Chip giant Advanced Micro Devices (AMD) has gained Tokyo-based Turing as a customer through AMD Ventures, the investment arm of AMD. The Japanese firm is building fully autonomous vehicles and has been sourcing chips from industry leader Nvidia (NVDA).

Now, AMD has a foothold in the company’s supply chain, as Turing started running roughly 10% of its AI training on AMD chips. Therefore, AMD now claims a share of the pie in the autonomous vehicle chip market as well. A share previously claimed by Nvidia.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Turing has been clear in its reasoning for adding more suppliers: lower costs and diversification benefits. It also might be added that Nvidia GPUs have been supply-constrained over the years. So, Turing, with a target of full self-driving software in consumer vehicles and driverless robotaxis as early as 2028, is burning through chips to train driving models, which explains the need to look for a new supplier.

This 10% share is important for AMD as well, since it indicates that its chips have come close enough to Nvidia’s so that a small company that cannot afford to have both GPU stacks at the same time, like a trillion-dollar tech giant, is also considering AMD’s ROCm software. It might also be mentioned that AMD was one of the chip giants that gained about $2 trillion in combined market cap in the second quarter, a list Nvidia was not a part of.

About AMD Stock

AMD, or Advanced Micro Devices, is a global semiconductor company that designs computing and graphics products for data centers, PCs, gaming, and embedded systems. Its operations center on creating high-performance, adaptive chips and on coordinating research, product development, supply chain partners, and global business functions to bring those products to market. The company is headquartered in Santa Clara, California and has a market capitalization of $900.17 billion.

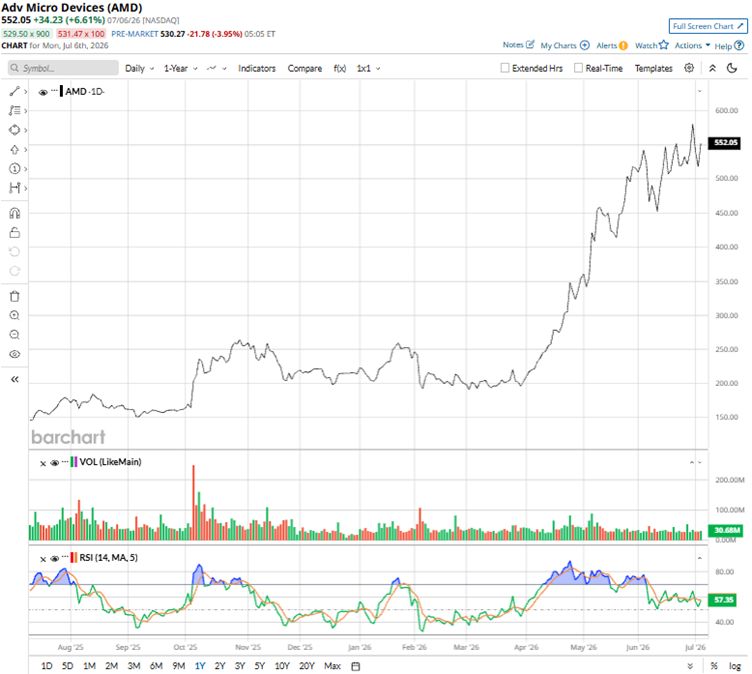

AMD’s stock has been up over the past year mainly because investors have re-rated chip makers higher on the AI boom, with the company benefiting from a broad semiconductor rally and renewed buying in the sector. Over the past 52 weeks, the stock has gained 286.9%, while it is up 143.56% year-to-date. The company’s shares reached a 52-week high of $584.73 on June 30, but are down 5.6% from that level.

www.barchart.com

www.barchart.com AMD has a 14-day relative strength index (RSI) of 57.35, which is closer to the overbought territory than the oversold territory. On a forward-adjusted basis, AMD’s price-to-earnings (non-GAAP) ratio of 70.12x is higher than the industry average of 24.61x.

AMD Q1 Earnings Topped Estimates on Data Center and AI Growth

AMD reported strong first-quarter results driven by demand for AI infrastructure, with data centers as the primary growth driver. The company’s revenue increased by 38% year-over-year (YOY) to $10.25 billion, exceeding the $9.85 billion expected by Wall Street analysts. Data Center segment revenue was $5.80 billion, up 57% YOY, driven by strong demand for AMD EPYC processors and the continued ramp of AMD Instinct GPU shipments.

On a non-GAAP basis, AMD’s gross margin climbed by one percentage point to 55%, while its operating income increased 43% YOY to $2.54 billion. The company’s non-GAAP EPS rose 43% from the prior-year period to $1.37, surpassing the $1.30 expected by Street analysts.

For the second quarter, AMD expects to report revenue of approximately $11.20 billion, plus or minus $300 million, representing about 46% YOY growth, with non-GAAP gross margin at approximately 56%.

Wall Street analysts are robustly optimistic about AMD’s future earnings. They expect the company’s EPS to climb by 400% YOY to $1.35 for Q2 2026. For fiscal 2026, EPS is projected to surge 88.1% annually to $6.15, followed by a 76.1% growth to $10.83 in fiscal 2027.

What Do Analysts Think About AMD’s Stock?

Recently, analysts at Goldman Sachs raised the price target on AMD’s stock from $450 to $640 while maintaining a positive stance. Despite volatility in semiconductor stocks and pressure on AMD as it comes down from its highs, this move suggests that Goldman Sachs analysts expect upside in AMD.

Wells Fargo analysts also maintained a bullish “Overweight” rating and raised the price target from $505 to $615. The firm said stronger demand for EPYC server CPUs, along with better pricing, is driving the increase. It also said it remains above consensus on data center GPU revenue estimates and lifted its 2027 and 2028 EPS forecasts to $13.40 and $18.75, respectively.

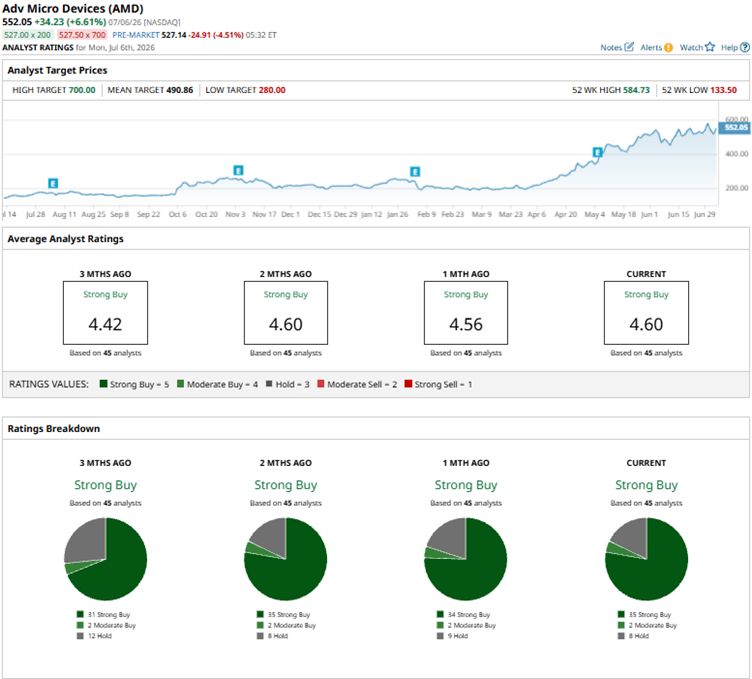

Chip giant AMD is an extremely popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 45 analysts rating the stock, a majority of 35 analysts have given it a “Strong Buy” rating, two analysts rated it “Moderate Buy,” while eight analysts are taking the middle-of-the-road approach with a “Hold” rating. The consensus price target of $490.86 represents 11.1% downside from current levels. However, the Street-high price target of $700 reflects 26.8% upside.

www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Michael Burry Is Shorting Caterpillar Stock for the First Time. Why You Shouldn’t Rush to Do the Same. Unusual Put Option Activity in Johnson & Johnson After JNJ Stock's Recent Runup A $2.2 Billion Reason to Buy Oracle Stock Here The Micron Stock Rally Is Far From Over. Here’s Why Bulls See $2,200 for MU Next.