Shares of Super Micro Computer (SMCI) have plunged about 35% over the past month, despite continued strength in artificial intelligence (AI) infrastructure demand. The sharp selloff followed the company's announcement of a massive $7 billion capital-raising plan, sparking concerns about dilution.

At first glance, the market's reaction appears justified. However, the financing announcement also reflects the scale of Super Micro's growth opportunity. The AI server manufacturer says it has secured roughly $39 billion in new AI server orders in recent weeks and needs additional capital to expand production and meet that surging demand.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

While dilution remains a legitimate risk, the company's robust order backlog suggests the capital raise is intended to support rapid growth. Meanwhile, the recent decline has pushed SMCI stock to a much more attractive valuation than it traded at just weeks ago.

www.barchart.com

www.barchart.com Super Micro's AI Tailwinds Could Fuel a Strong Comeback

Share dilution has weighed on investor sentiment, but Super Micro's latest results suggest the market may be overlooking the bigger picture. Beneath the headlines, AI demand remains robust, the customer base is becoming more diversified, and management is investing to drive higher profitability over time.

Fiscal third-quarter revenue jumped 123% year-over-year (YoY) to $10.2 billion, reflecting continued strength in AI infrastructure spending from hyperscale and enterprise customers. Although component shortages and deployment delays limited sequential growth, management indicated that much of the delayed demand has shifted into future quarters.

Supporting SMCI’s investment appeal is the company's expanding enterprise business. Enterprise revenue accounted for 28% of total sales, up from 15% a year earlier. Revenue in this segment increased 46% YoY and 45% sequentially, reducing reliance on just a few hyperscale customers and creating a more balanced revenue mix.

The company’s core OEM appliance and large data center segment generated $7.4 billion, growing 183% from the prior year. Despite deployment timing issues, demand for AI servers appears firmly intact.

Super Micro is also working to improve earnings quality. Through its Data Center Building Block Solutions (DCBBS) strategy, the company is expanding beyond standalone servers by offering integrated solutions that include liquid cooling, networking, software, and related services. This broader portfolio should deepen customer relationships while supporting higher-margin revenue over time.

In addition, SMCI continues to expand manufacturing capacity, automate production, improve efficiency, and strengthen supplier relationships to boost output and gradually expand margins as volumes increase.

Returning to the dilution issue, management says the additional capital will help secure critical components, expand production capacity, and meet growing demand for AI servers. Recent orders from more than 20 customers provide additional visibility into future revenue.

Overall, AI infrastructure spending continues to accelerate as cloud providers, enterprises, and governments invest heavily in next-generation computing. With strong revenue growth, expanding enterprise adoption, a growing backlog, and ongoing investments to scale production, Super Micro appears well-positioned to benefit from this multi-year AI investment cycle.

SMCI Stock Is Trading at a Valuation That’s Hard to Ignore

The sharp pullback in SMCI stock has significantly improved its valuation, making it attractive for long-term investors. The stock trades at a forward P/E multiple of 9.8, which is low for a company that analysts expect to deliver solid earnings growth over the next year.

Wall Street expects Super Micro to generate $2.13 in earnings per share in fiscal 2027, suggesting the stock is undervalued. At the same time, its price-to-sales (P/S) ratio of only 0.54 further strengthens its investment case.

The Bottom Line

SMCI stock could mark a solid comeback in 2026 and beyond. Solid AI infrastructure demand, a large order backlog, expanding enterprise exposure, and a compelling valuation make the stock attractive.

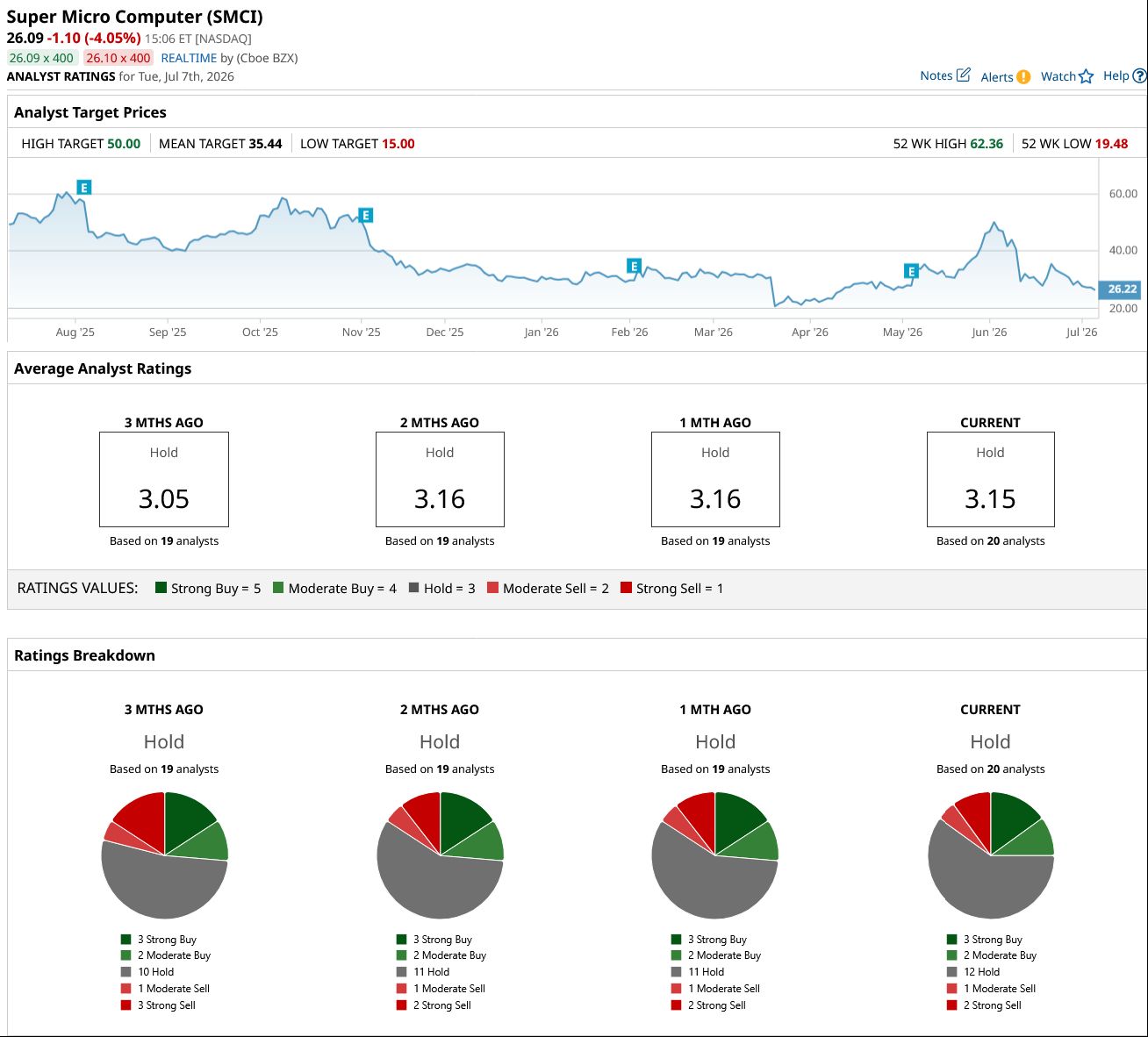

While analysts maintain a “Hold” consensus rating on SMCI stock, it offers an attractive risk-reward opportunity near the current levels.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Super Micro Drops 35% in a Month. What’s Next for SMCI Stock in 2026. 3 Calendar Spread Trade Ideas For This Wednesday Stock Index Futures Tumble as Oil Jumps After Trump Says U.S.-Iran Ceasefire Is Over, FOMC Minutes on Tap AbbVie vs Eli Lilly: 1 Is Clearly the Better Dividend Stock to Buy and Hold for the Next 10 Years