Every new wave of technology brings new opportunities and new risks along with it. As businesses race to adopt artificial intelligence (AI), protecting digital infrastructure has become more critical than ever. That’s where Palo Alto Networks (PANW) has carved out its leadership, offering cybersecurity solutions that help enterprises safeguard everything from cloud workloads to AI-powered operations. The company’s ability to stay ahead of evolving threats has kept it firmly on investors’ radar, and Wall Street appears to be growing even more optimistic.

Recently, Needham raised its price target on PANW stock by over 20%, increasing it to $425 from $350 while reiterating its “Buy” rating. The brokerage also lifted its long-term estimates for the company’s next-generation security (NGS) annual recurring revenue (ARR), reflecting growing confidence that Palo Alto can sustain strong organic growth while successfully integrating its recent acquisitions. The bullish outlook suggests Needham believes the company is well positioned to capitalize on the next phase of cybersecurity demand.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

So, what exactly convinced Needham to become even more optimistic about Palo Alto’s growth story? Let’s the reasons behind the firm's belief that PANW still has meaningful upside ahead.

About Palo Alto Networks Stock

Palo Alto Networks is one of the world’s leading cybersecurity companies, helping businesses protect their networks, cloud systems, applications, and data from constantly evolving cyber threats. Headquartered in Santa Clara, the company has grown into a cybersecurity giant with a market capitalization of $274.68 billion.

Its platform combines network, cloud, and AI-powered security solutions, enabling organizations to detect and respond to threats in real time. Palo Alto also leverages threat intelligence from its Unit 42 team to help customers stay ahead of increasingly sophisticated cyberattacks. By bringing multiple security tools together on a single platform, the company simplifies cybersecurity management while helping enterprises strengthen their digital defenses in an increasingly connected world.

That strong business foundation has also been reflected in the stock’s performance. PANW stock has turned a sharp setback into an even sharper comeback, with investors steadily warming back up to the cybersecurity giant. Earlier this year, the stock came under pressure as investor enthusiasm around AI-driven themes cooled, falling to a 52-week low of $139.57 in February.

However, the pullback proved short-lived. As confidence returned and analysts grew increasingly optimistic about the company’s long-term growth prospects, PANW staged a remarkable rebound. The stock has since surged 129.6% from its February low and recently climbed to a record high of $368.17 on July 6, helped by a string of recent bullish analyst calls.

The rally has translated into impressive returns across multiple time frames. Over the past 52 weeks, PANW stock has gained 55.9%. The momentum has been even stronger in 2026, with shares soaring 72.6% year-to-date (YTD). Over the past three months alone, the stock has nearly doubled, jumping 83%, while rising 19.4% over the last month.

Although the 14-day RSI recently entered overbought territory, it has since eased to 57.76, suggesting buying pressure has moderated without significantly weakening the uptrend. At the same time, the MACD oscillator signals bullish sentiments, with the MACD line above the signal line and the histogram printing positive bars. Together, these signals indicate that bullish momentum remains intact, suggesting PANW could have further upside if broader market conditions continue to support the rally.

www.barchart.com

www.barchart.com Of course, quality rarely comes cheap, and PANW stock carries a premium valuation. The stock trades at 89.33 times forward adjusted earnings and 24.05 times forward sales, well above sector averages and its own historical median. Investors are clearly willing to pay up for its consistent growth, expanding platform, and acquisition strategy. But a rich valuation is a double-edged sword. It leaves little room for missteps if growth or execution begins to lose steam.

A Snapshot of Palo Alto Networks’ Q3 Numbers

Palo Alto Networks’ third-quarter fiscal 2026 results, released on June 2, showed the company is riding a strong wave of demand as businesses ramp up investments in AI-powered cybersecurity. Revenue climbed 31% year-over-year (YOY) to $3 billion, comfortably beating Wall Street’s expectations, as more enterprises turned to Palo Alto’s platform to secure AI deployments at scale. Management said accelerating organic bookings momentum was a key driver behind the strong quarter, suggesting customer demand remains healthy despite an uncertain macroeconomic backdrop.

The company’s business model also continues to shift toward more predictable recurring revenue. Product revenue rose to $594 million, accounting for 19.8% of total revenue, while subscription and support revenue increased to $2.41 billion, making up the remaining 80.2%. That mix continues to work in Palo Alto’s favor, helping it maintain a healthy gross margin of 75.8% and a non-GAAP operating margin of 27.1%. Meanwhile, non-GAAP earnings improved 6.3% annually to $0.85 per share, also topping Street’s projections.

Growth was not limited to the income statement. Remaining performance obligations (RPO), a closely watched indicator of future revenue, jumped 36% YOY to $18.4 billion, aided by contributions from CyberArk and Chronosphere. At the same time, NGS ARR surged 60% to $8.1 billion, highlighting strong adoption of the company’s expanding AI-driven security platform.

Palo Alto continued to generate robust cash flows. As of April 30, it held $3.1 billion in cash, cash equivalents, and short-term investments. Net cash from operating activities increased to $871 million, while adjusted free cash flow reached $910 million. Its trailing 12-month adjusted free cash flow margin also improved 430 basis points YOY to 38.5%.

With momentum clearly on its side, management anticipates Q4 revenue to be between $3.345 billion and $3.355 billion, representing roughly 32% annual growth, along with non-GAAP EPS expected to be somewhere between $0.96 and $0.98. It also expects NGS ARR to reach $8.9 billion to $8.95 billion, implying 59% to 60% growth, while RPO is projected between $20.9 billion and $21 billion.

For the full fiscal year, the company now forecasts revenue of $11.415 billion to $11.425 billion and non-GAAP EPS of $3.77 to $3.79, reflecting management’s confidence that strong customer demand and platform adoption will continue through the remainder of the year.

Analysts tracking the company project its EPS to be around $2.03 in fiscal 2026, representing a growth of around 23.4% YOY, while revenue is expected to be $11.4 billion. For fiscal 2027, analysts expect EPS of $2.24, up 10.3% annually.

What Do Analysts Expect for Palo Alto Networks Stock?

Needham analyst Mike Cikos raised PANW’s price target to $425 from $350 after becoming more confident in the company’s ability to sustain long-term growth. The biggest reason behind the upgrade was his higher forecast for Palo Alto’s NGS ARR, which he now expects to reach $10.95 billion in fiscal 2027.

According to Cikos, that confidence is supported by the company’s strong core business, which is projected to generate roughly $1.5 billion in net-new NGS ARR during fiscal 2026, even before factoring in acquisitions. He also expects Palo Alto’s recently announced acquisition of CyberArk to contribute around $250 million in net-new ARR, while Chronosphere is expected to add a normalized $100 million. Although Chronosphere has enjoyed an unusual boost from a leading frontier AI lab customer in fiscal 2026, Cikos expects that migration to conclude by Q4, allowing growth to normalize in fiscal 2027 while still supporting a healthy long-term outlook.

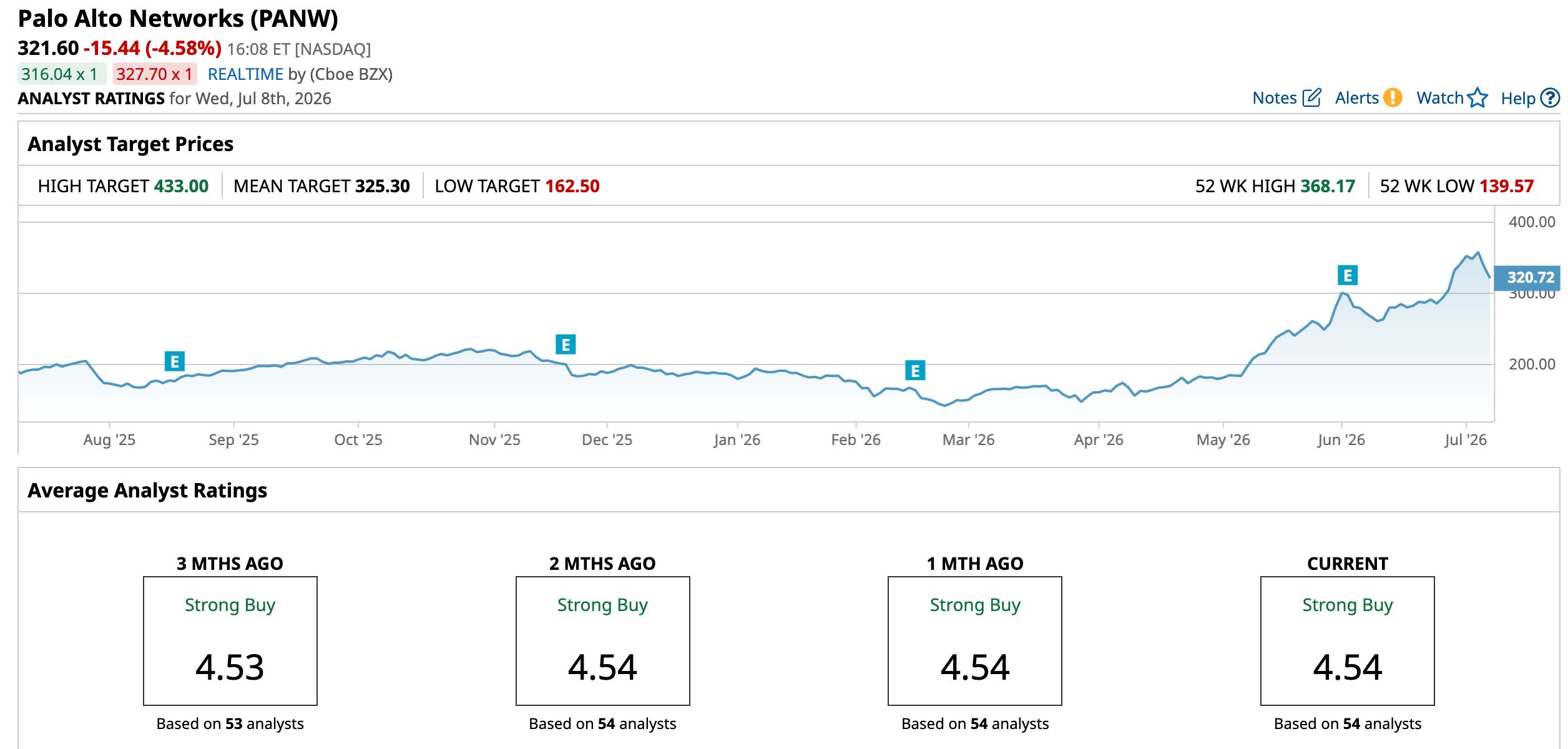

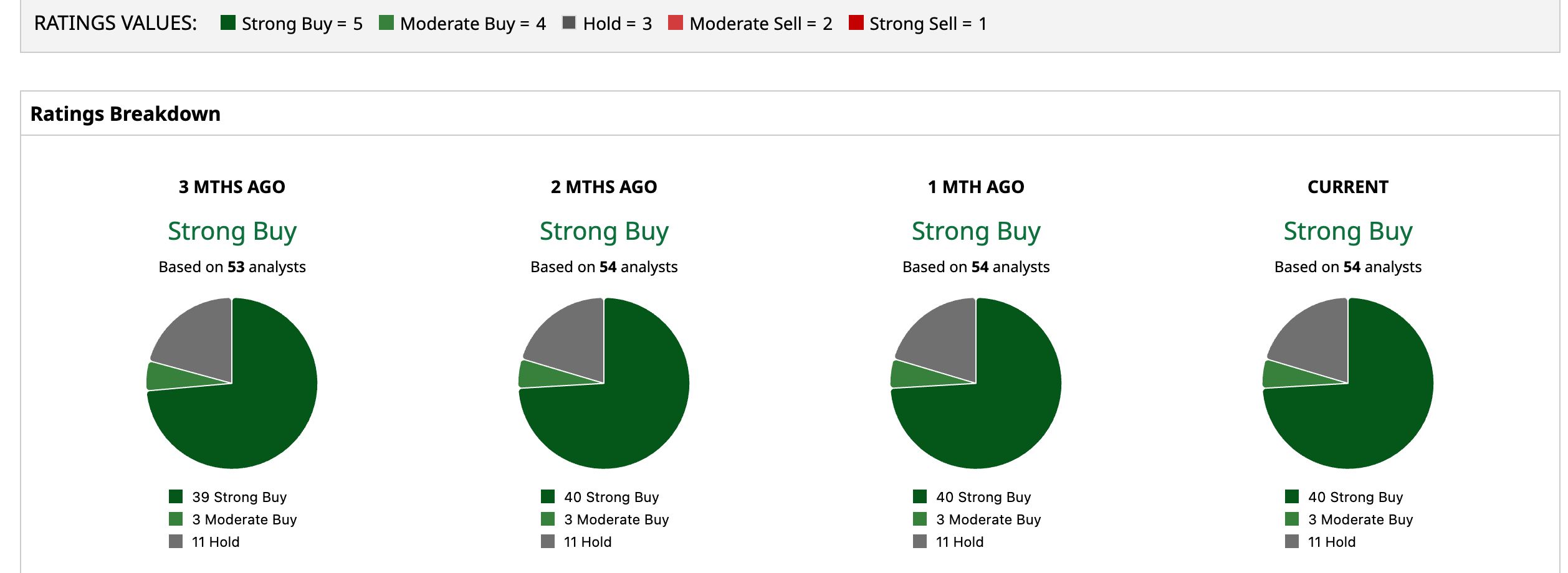

Overall, sentiment on PANW remains firmly bullish, with the stock’s consensus rating at “Strong Buy.” Out of 54 analysts, 40 recommend a “Strong Buy,” three have a “Moderate Buy,” and the remaining 11 are giving it a “Hold” rating.

The mean target price of $325.30 implies a marginal upside but the Street-high price target of $433 suggests the stock could rise as much as 34.6% from the current price levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Needham Just Raised Its Palo Alto Stock Price Target by More Than 20% This ETF Promises to Protect Your Portfolio with High-Quality Stocks, But Its Chart Is Waving a Yellow Flag Nvidia Says Kyber Is Still on Track. Why the Next-Gen Infrastructure Matters for NVDA Stock. Alibaba Shares Are Gaining on AI Optimism. Here's What to Know.