Spending on tools that help companies talk to customers is jumping fast, and that matters for any business selling digital experience software. Recent research shows the AI market for sales and marketing is expected to grow from $58.00 billion 2025 to about $240.59 billion by 2030, which works out to a strong 32.9% annual growth rate.

That kind of expansion should, on paper, be good news for platforms that power content creation and customer interactions. Yet Adobe (ADBE) is finding itself in a very different spotlight.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The stock is trading near multi‑year lows around $200 and is one of the big underperformers in the S&P 500 Index ($SPX) so far in 2026. That weak performance now comes with a fresh blow, as Bank of America has cut its rating on Adobe to "Underperform" and says new AI tools are starting to hurt its growth outlook instead of helping it.

So what does that really mean for ADBE’s prospects from here, and is the market overreacting or simply catching up to reality?

Adobe’s AI Numbers

Adobe develops Creative Cloud and Document Cloud software that people and businesses use to design, edit, and manage digital content, and the company is headquartered in San Jose, California, at the heart of the U.S. tech industry.

ADBE is down 36.9% year to date and 42.2% over the past 52 weeks.

www.barchart.com

www.barchart.comThe company’s market cap is $88.06 billion, and the shares trade at 9.70 times trailing price-to-earnings and 9.07 times forward price-to-earnings versus sector medians of 26.17 times and 24.77 times, showing a clear valuation discount.

Their quarter ending May 26 delivered earnings per share (EPS) of $4.58 versus a $4.74 estimate, a 3.38% negative surprise. The second‑quarter FY2026 update on June 13 reported record revenue of $6.62 billion, up 13% year-over-year (YOY), or 11% in constant currency.

It also showed GAAP diluted EPS of $4.25 and non‑GAAP EPS of $5.96, with GAAP including a $0.17 per‑share non‑cash goodwill impairment tied to the Publishing and Advertising unit. ADBE exited the quarter with $27.10 billion in total annualized recurring revenue, including about $480 million from Semrush.

The company posted GAAP operating income of $2.24 billion and non‑GAAP operating income of $2.95 billion, along with GAAP net income of $1.71 billion and non‑GAAP net income of $2.40 billion. This period also saw $2.17 billion in cash from operations, operating cash flow of $5.123 billion, up 73.19% YOY, and net cash flow of -$512 million with a -156.83% change, reflecting heavy capital deployment and roughly 8.5 million shares repurchased.

Adobe Hard AI Lean

Adobe is pushing deeper into AI in a very practical way. The company recently agreed to buy Topaz Labs, a firm known for image and video enhancement tools, with the deal announced in late June 2026. This acquisition brings in products like Astra, which helps upscale video, and Wonder, which focuses on cleaning up and retouching images.

It also adds Neurostream technology that can cut memory needs for large video models by up to 95% and make more processing happen directly on devices. These tools are expected to plug straight into Firefly and key Creative Cloud apps such as Photoshop, Lightroom, Premiere Pro, and Illustrator, boosting Adobe’s ability to sharpen, denoise, upscale, stabilize, and repair content without forcing users to leave its ecosystem.

The company is backing this up with new partnerships aimed at big creative and enterprise teams. Fresh deals with Accenture (ACN), Omnicom (OMC), WPP plc (WPP), Microsoft (MSFT), and Anthropic are meant to bake Firefly and related tools into marketing and tech stacks so creative and data teams can use software agents to plan, create, and fine‑tune campaigns at scale.

On the product front, Adobe has started rolling out a broad expansion of its Creative Agent across Firefly and Creative Cloud apps, adding more in‑app help and automation inside flagship tools like Photoshop and Premiere. The aim is to turn AI from a handful of separate buttons into something that is present throughout the workflow, from the first idea to the final export.

All of these details sit at the heart of the current debate around the stock because they show a company investing heavily in AI.

Analyst Lens on Adobe

Adobe’s next earnings report is marked on the calendar for September 10, and expectations are fairly straightforward. For the quarter ending in August 2026, the average EPS estimate sits at $4.86, up from $4.29 a year earlier, which works out to 13.29% growth.

Some investors think the market is already too pessimistic. Michael Burry has argued that ADBE is being mispriced and that management needs to show AI is driving real revenue, not just new features, to prove that view right.

Another camp is warming up to that idea, at least at the margin. HSBC recently moved Adobe from “Hold” to “Buy” and lifted its price target from $282 to $308, which works out to 39.4% upside from recent levels. Their case rests on the day‑to‑day reality of how people use Adobe’s software, pointing to deeply embedded workflows, a very large user base, and a fast‑growing set of new tools inside Creative Cloud.

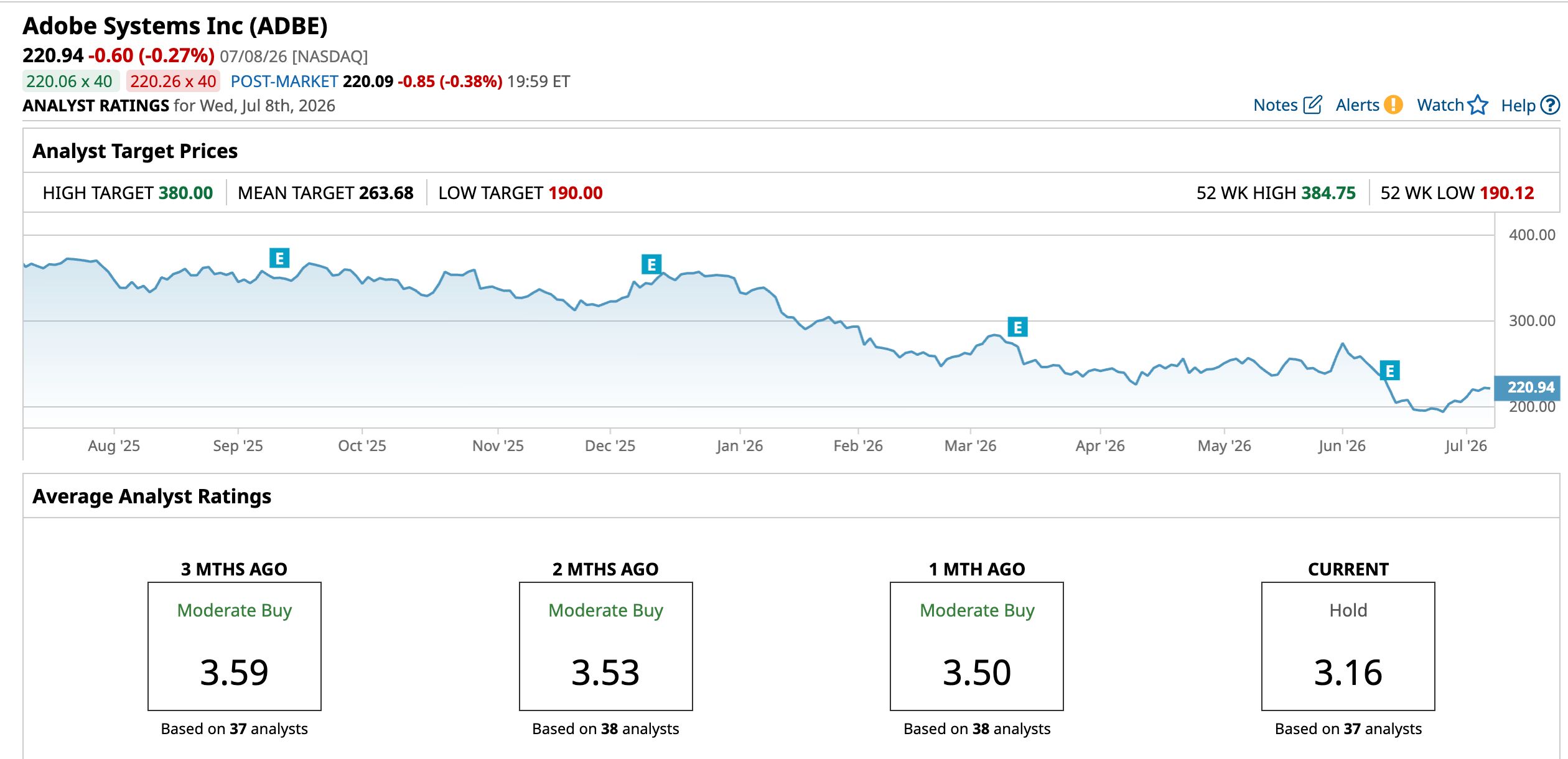

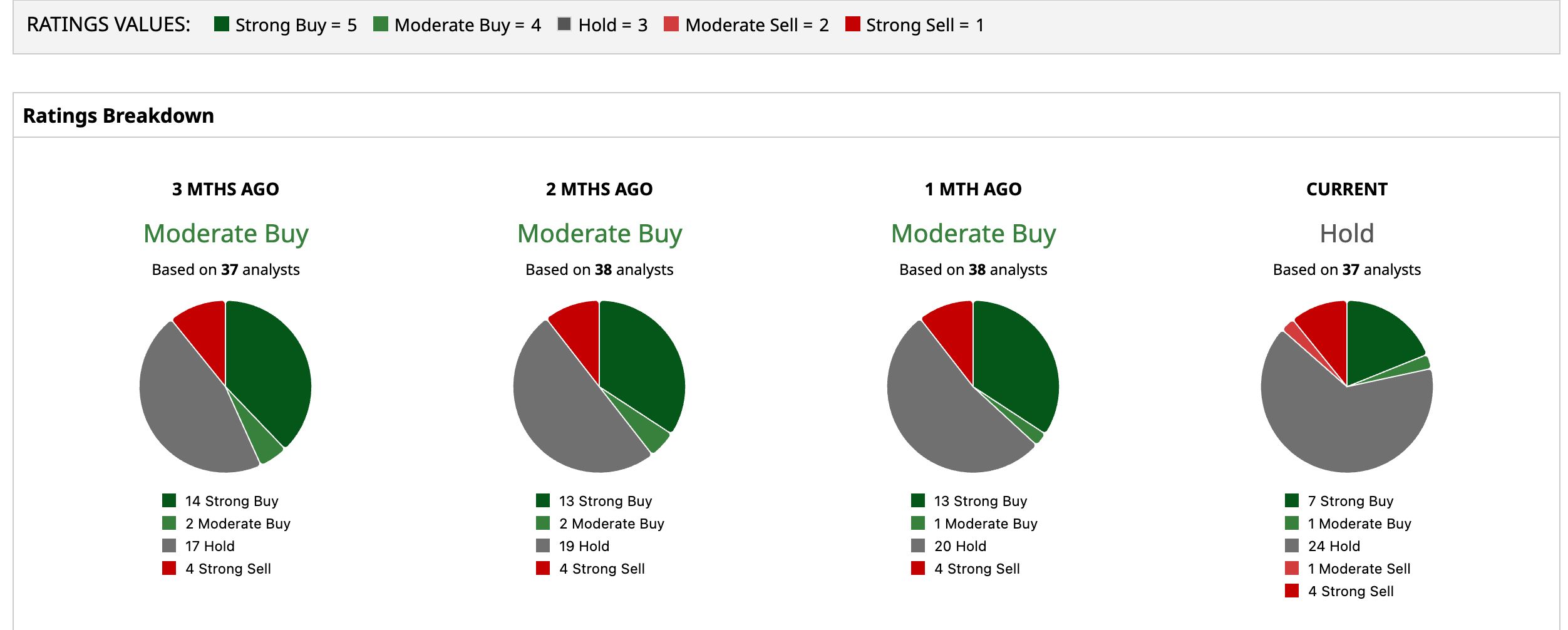

The wider Street view backs up that caution, with 37 analysts providing a consensus “Hold” rating on ADBE. It also has an average price target of $263.68, implying roughly 19.4% upside.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comConclusion

So what does Bank of America’s downgrade really mean for Adobe right now? It basically says the market is done paying a premium for Adobe’s AI story until the numbers clearly show faster and more durable growth again. Given double-digit EPS estimates but muted targets and a wall of “Hold” consensus calls, shares look more likely to drift sideways or slightly lower than rip higher near term. However, if management can show that AI is adding paying users and real pricing power instead of just new tools, then ADBE can gradually move back into a higher trading range over time.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Bank of America Says AI Will Drag Down Adobe Stock Why Chapter 11 Might Be the Best Move for JetBlue Stock in 2026 IBM’s Quantum Breakthrough Sends Massive Clean Energy Signal DeepSeek Just Dealt Nvidia Stock a Potentially Major Blow