Applied Materials (AMAT) stock has surged by nearly 190% in the last 52-weeks. The picks and shovels play in the AI revolution has continued to benefit and growth can potentially accelerate in the coming years.

According to Stifel, semiconductor equipment manufacturers like Applied Materials, KLA-Tenor (KLAC), and Lam Research (LRCX), are positioned to benefit from a “prolonged demand cycle in the industry.” Stifle has a “Buy” rating for AMAT stock with a price target of $650.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

This view does not come as a surprise. The global semiconductor market was valued at $796 billion in 2025. For the current year, the market size is expected to swell to $1.5 trillion. As industry tailwinds sustain, the market is expected to touch $1.9 trillion by 2027.

Earlier this month, Applied Materials CEO indicated that chipmakers are sharing their “equipment demand outlooks for two years or more to ensure their capacity expansions proceed smoothly.”

Given the demand outlook, Applied Materials is well positioned for sustained value creation. In June 2026, the company opened a $500 million manufacturing campus in Singapore to cater to the incremental demand. Overall, the company has nearly doubled manufacturing capacity considering U.S., Singapore, and Europe. The capacity expansion will support growth acceleration.

About Applied Materials Stock

Headquartered in Santa Clara, California, Applied Materials is a provider of materials engineering solutions used to produce virtually every semiconductor. The company’s expertise includes design, development, production, and servicing of the critical wafer fabrication tools for semiconductor manufacturing. Applied Materials has two business segments: Semiconductor Systems and Applied Global Services.

The Semiconductor Systems segment designs, develops, manufactures, and sells a wide range of equipment used to fabricate semiconductor chips. Further, the AGS segment provides services, spares and factory automation software to customer fabrication plants globally.

For the first half of FY26, Applied Materials reported revenue of $14.9 billion. For the same period, the company’s operating income and operating cash flow were $4.4 billion and $2.5 billion, respectively. From a geographic perspective, AMAT reported 74% of Q2 FY26 revenue from Korea, Taiwan, and China. Further, 12% of the revenue was from the United States.

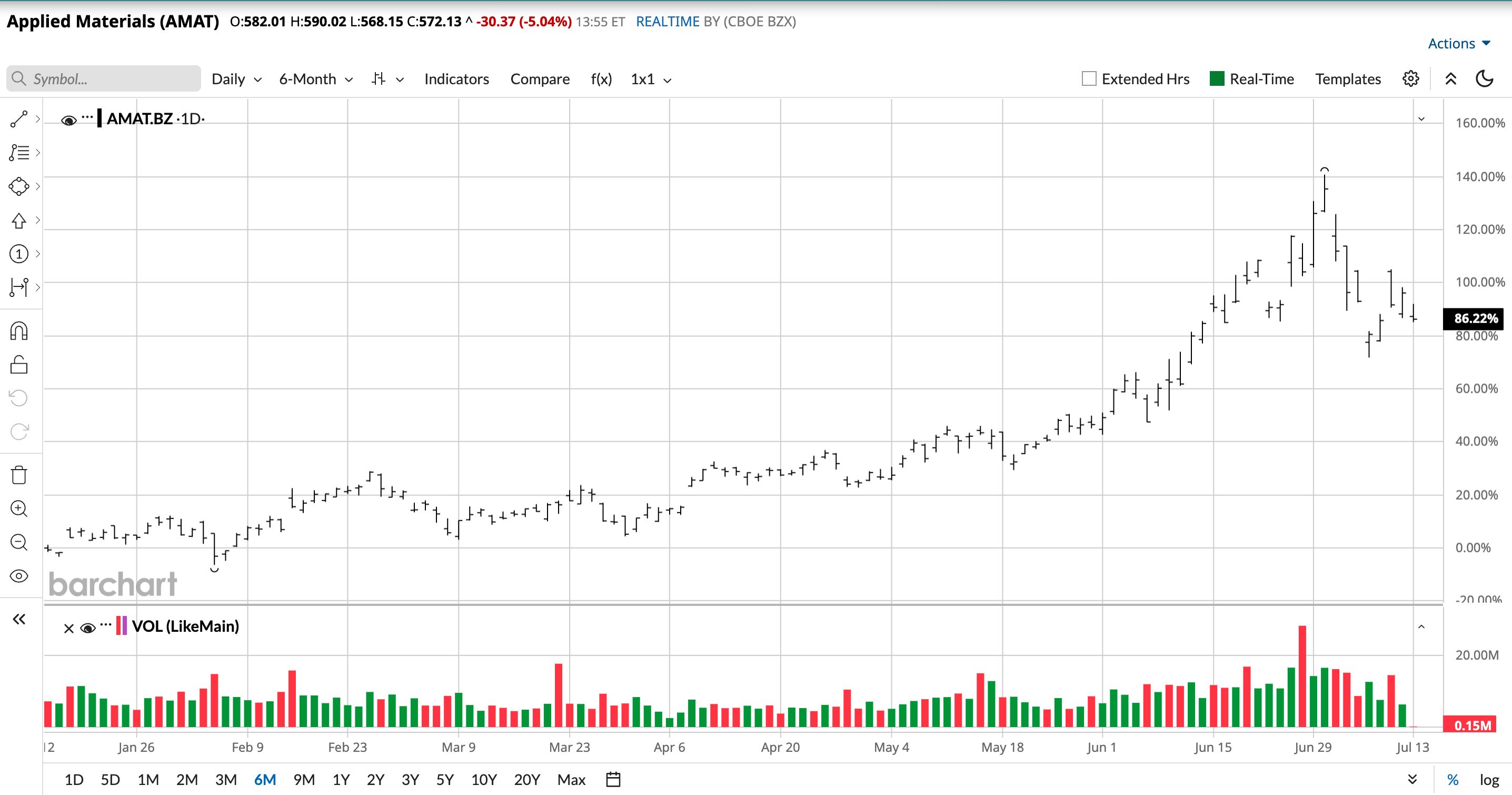

Considering the tailwinds for the semiconductor industry, the trend for AMAT stock is likely to remain positive even after an upside of 87.7% in the last six months.

www.barchart.com

www.barchart.com Margin Expansion Likely to Sustain

For Q2 FY26, Advanced Materials reported operating margin of 32.1%. Year-over-year (YOY), margin expanded by 140 basis points. Besides ongoing manufacturing cost improvement, value-based pricing on differentiated products is likely to ensure sustained margin expansion. Further, there is clear demand visibility over the next 24 to 36 months. Therefore, Applied Materials is positioned for upside in free cash flows. This will support dividend growth and aggressive share repurchases.

Notably, Applied Materials reported total cash and investments of $13.4 billion as of Q2 FY26. Even with debt of $6.5 billion, the company has high financial flexibility and an investment-grade credit rating. The company is positioned for continued investment in research and development coupled with infrastructure development.

What Do Analysts Say About AMAT Stock?

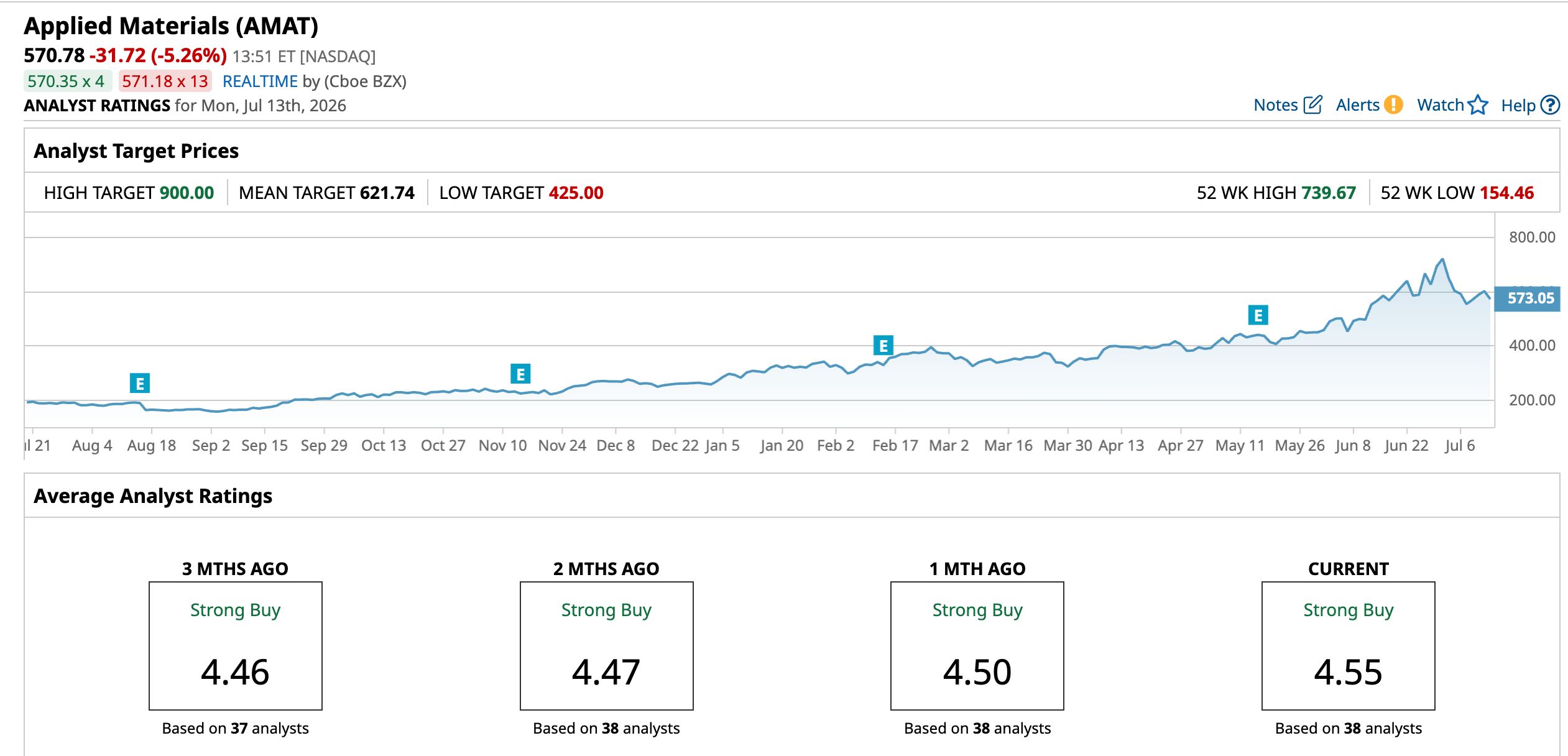

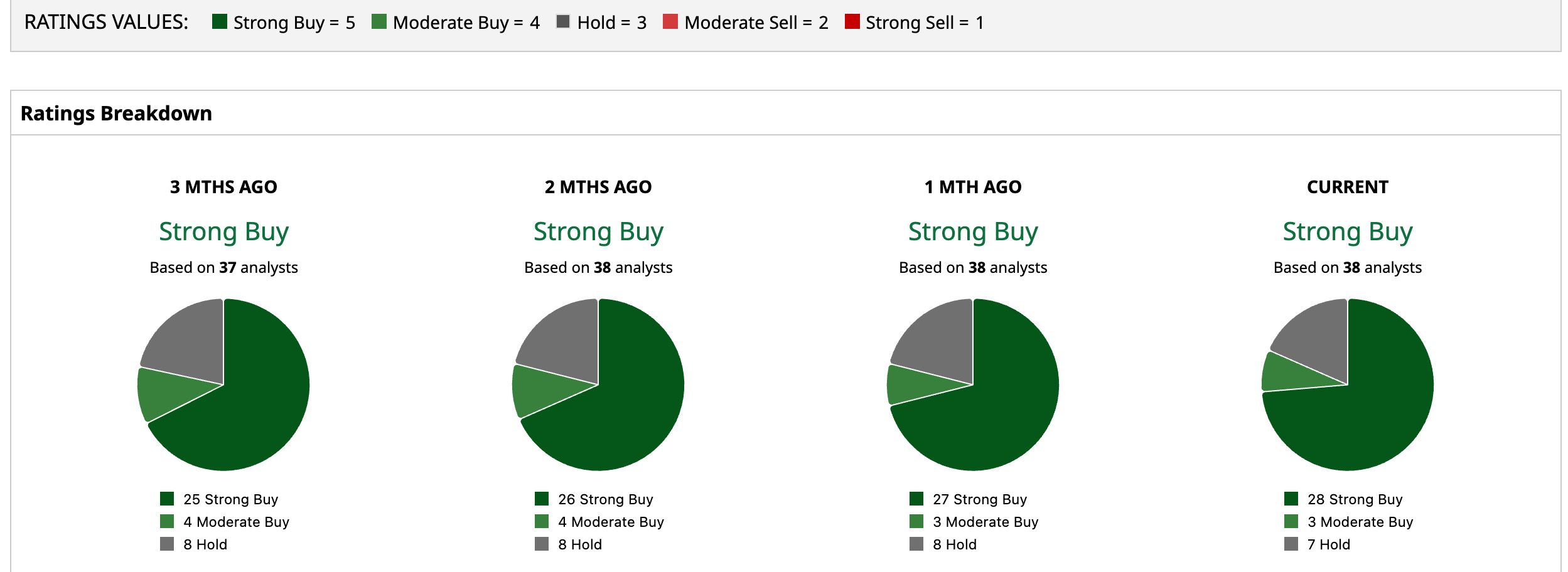

Based on 38 analysts with coverage, AMAT stock has a consensus “Strong Buy” rating. While 28 analysts have a “Strong Buy” rating for the stock, three have a “Moderate Buy,” and seven analysts have a “Hold” rating.

The mean price target of $621.74 represents an upside potential of 9% from current levels. Furthermore, the most bullish price target of $900 suggests that AMAT stock could climb as much as 57.7% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Concluding Views

AMAT stock has witnessed a strong rally that’s backed by fundamental factors. With the company having a strong position in leading edge logic, DRAM, and advanced packaging, the outlook is bullish.

According to analyst estimates, earnings growth for FY26 and FY27 is expected at 28.77% and 33.47%, respectively. Considering the industry factors and capacity expansion, it’s likely that robust growth will sustain beyond FY27. This makes AMAT stock worth considering on corrections.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

CF Industries Just Raised Its Dividend by 20% While Its Stock Has Surged 55% in 2026 PC Shipments Fell in Q2, but AI Optimism Is Set to Keep Growing and Push DELL Stock Higher Applied Materials: The Picks-and-Shovels Play in an AI Era Will Continue to Trend Higher Circle Just Won a Major Banking Approval. This Could Be a Game Changer for CRCL Stock.