While artificial intelligence (AI) stocks have taken center stage now, retail stocks have been the reliable ones in times of economic uncertainty. Costco Wholesale (COST) and Walmart (WMT) are two of the world's largest retailers, both generating billions in annual sales while rewarding shareholders with consistent dividends. But only one company stands out as the stronger long-term investment.

The Case for Costco

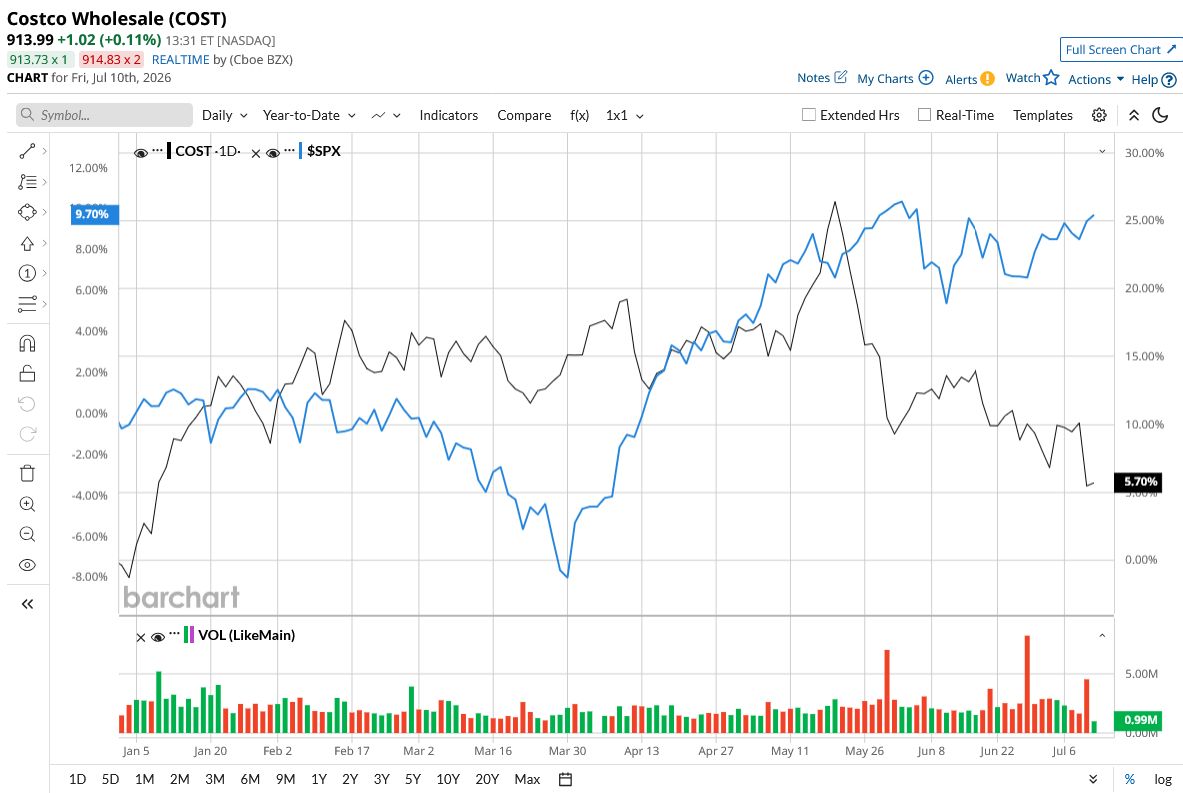

Costco Wholesale is a warehouse club retailer that provides members access to a wide range of products at low prices by selling in bulk through large warehouse locations. COST stock has climbed 6% year-to-date (YTD), underperforming the S&P 500 Index ($SPX) gain of 11%.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

www.barchart.com

www.barchart.com Globally, Costco now operates close to 928 warehouses. The company even has plans of opening 30 net new warehouses annually over the coming years. Unlike other retailers, Costco’s business model is unique. It offers its members a selection of high-quality products at low prices by charging a membership fee. Its membership fee income rose 11% in the third quarter of fiscal 2026 to $1.37 billion. This led to a 12% increase in net sales to $69.2 billion, while diluted earnings per share (EPS) jumped 15% to $4.93.

Furthermore, this year higher oil prices and supply disruptions in the Middle East fueled strong consumer demand for lower-priced fuel options. Costco took advantage of this by maintaining inventory and offering competitive pricing, which boosted its gas business. Excluding gasoline sales, comparable sales also increased 6.6% in the quarter, reflecting the strength of its core merchandise business.

Its membership-based model creates an unusually loyal customer base, with renewal rates remaining above 90% in the U.S. and Canada for years. This competitive advantage has translated into strong comparable sales growth. Recently, the company reported a 10.6% increase in June comparable sales to $29.2 billion.

Costco offers a low forward dividend yield of 0.62% and also pays out just 27% of its profits as dividends. However, the company is on the verge of becoming a Dividend Aristocrat by increasing its dividends for the past 23 years. It recently hiked its quarterly dividend by 13% to $1.47 per share. Occasionally, the company also pays a special dividend to its shareholders, besides its regular dividends. The company paid out $1.1 billion in dividends in the third quarter.

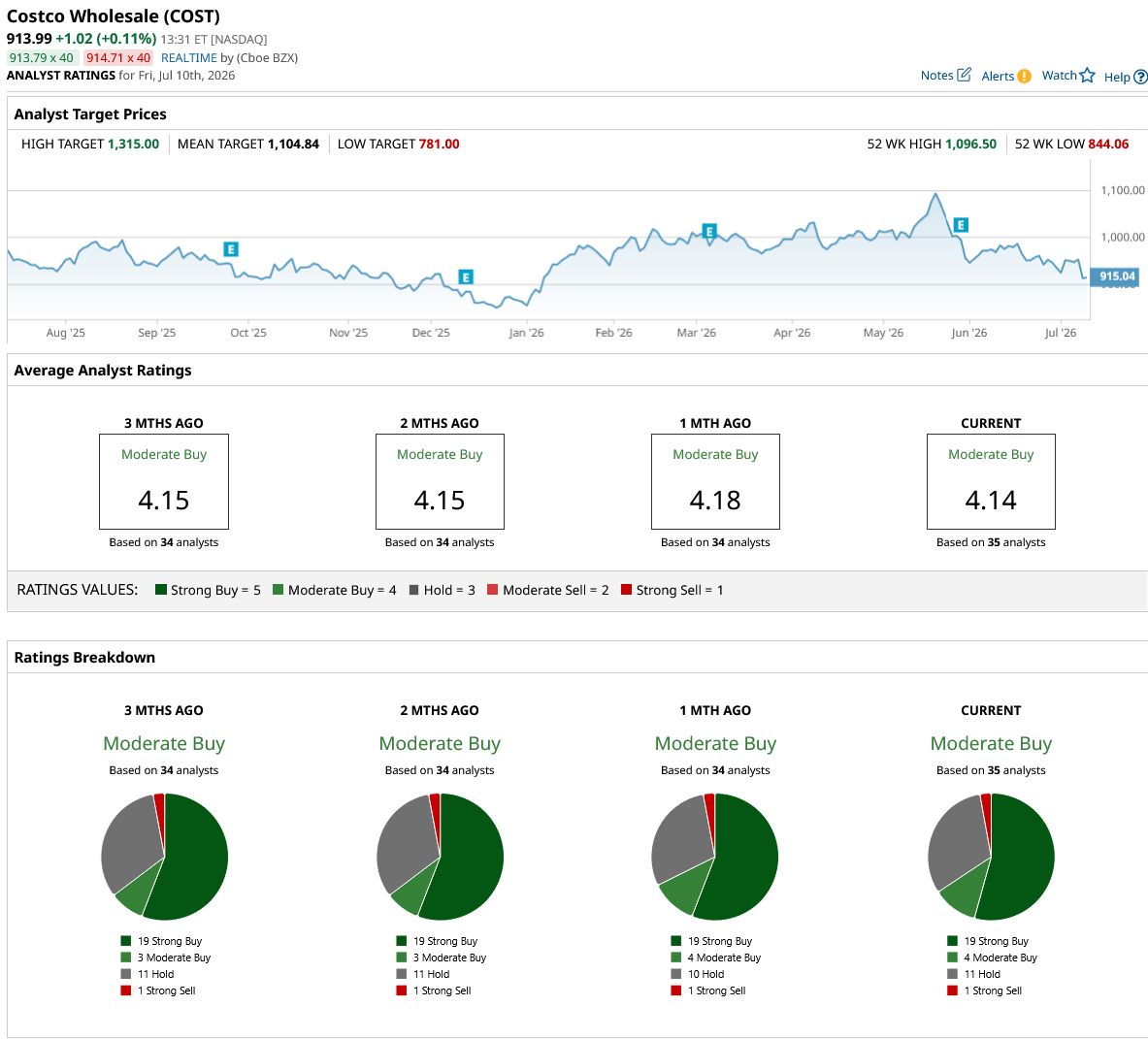

On Wall Street, COST stock is a consensus "Moderate Buy." Of the 35 analysts covering the stock, 19 rate it a "Strong Buy," four say it is a "Moderate Buy," 11 rate it a "Hold," and one analyst says it is a "Strong Sell." The average target price of $1,104.84 suggests COST can climb by 20% from current levels. Plus, the high price estimate of $1,315 suggests an upside potential of 43% over the next 12 months.

www.barchart.com

www.barchart.com The Case for Walmart

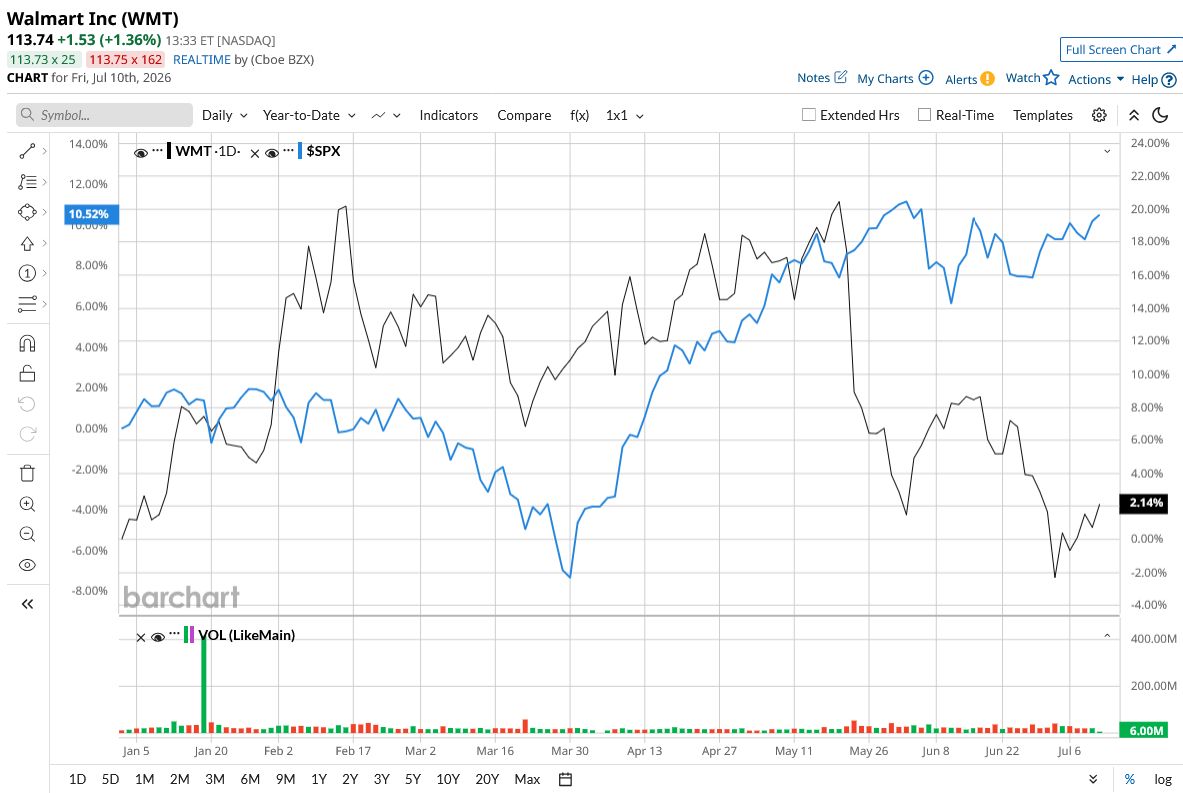

Walmart is the world’s largest retailer that operates a network of discount stores, supercenters, neighborhood markets, warehouse clubs, and a rapidly growing e-commerce platform. Unlike Costco, Walmart is open to everyone and not just select members. WMT stock has climbed 2% YTD, underperforming the broader market.

www.barchart.com

www.barchart.com Walmart now operates a network of more than 10,900 stores, which remains its significant competitive advantage. During the latest first quarter of fiscal 2027, consolidated revenue increased 7.3% to $177.8 billion, with a 4.1% increase in comparable sales. Additionally, its digital ecosystem is becoming another powerful profit engine. Enterprise e-commerce revenue increased 26% in the quarter. Walmart’s advertising business grew by more than 30% across every operating segment. Membership fee revenue climbed 17%, with Walmart+ recording its highest-ever first-quarter net member additions.

Walmart is also using AI and automation to improve efficiency. Thanks to its AI shopping assistant, Sparky, weekly active users increased by more than 100% during the quarter. The company expects full sales growth of 3.5% to 4.5%, with EPS landing between $2.75 and $2.85. For dividend investors, Walmart's financial strength makes the investment case even more compelling. While Walmart’s yield of 0.62% and payout ratio of 27% are low, its Dividend King status makes it more appealing to income investors. The company has not only paid but also increased dividends for 53 years.

An unmatched global scale, expanding ecosystem of higher-margin businesses, AI-driven operational improvements, resilient omnichannel retail model, and its Dividend King status make Walmart stand out as the better choice for the long term.

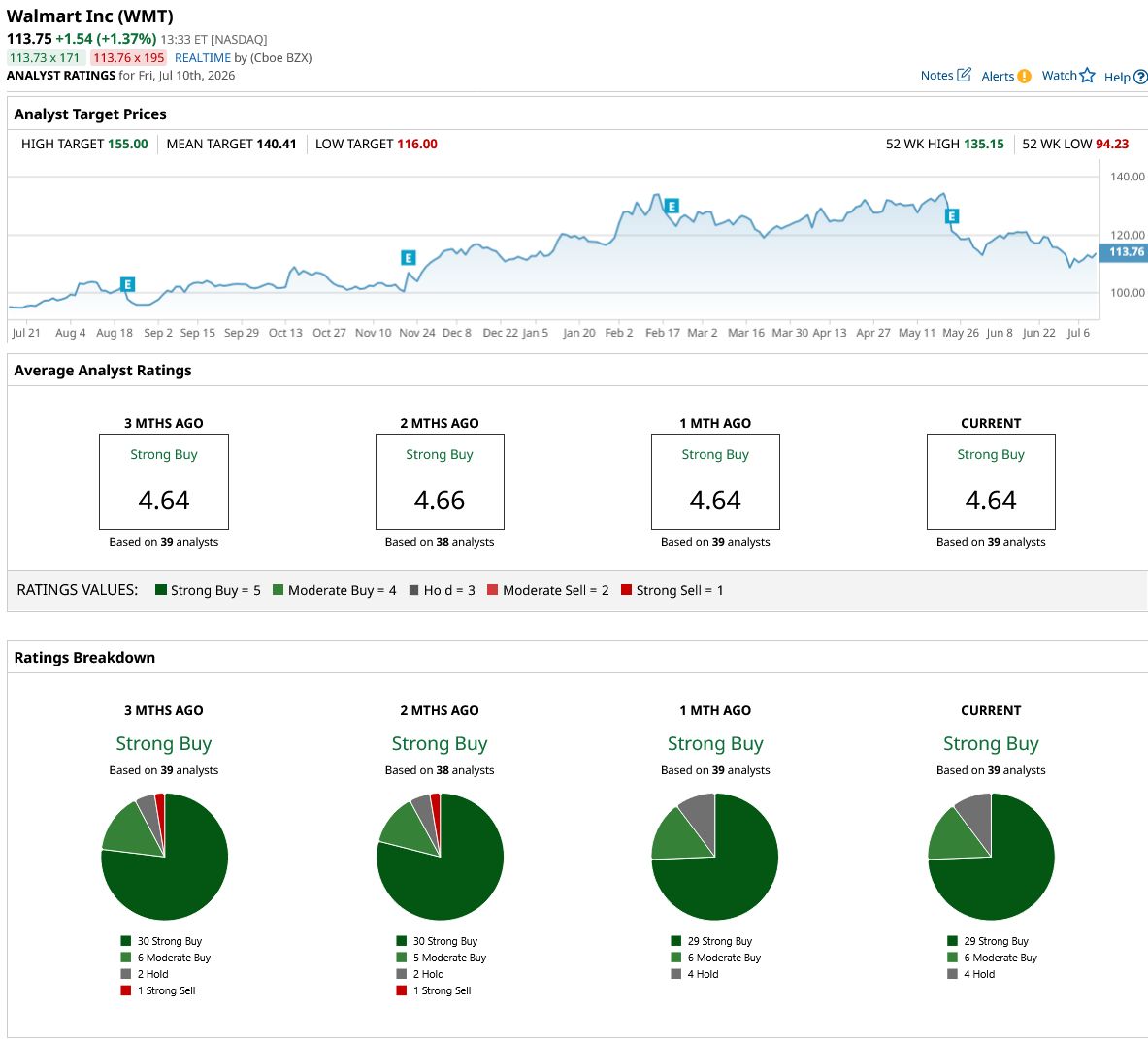

On Wall Street, WMT stock holds a consensus “Strong Buy” rating. Of the 39 analysts covering the stock, 29 rate it a “Strong Buy,” six say it is a “Moderate Buy,” and four rate it a “Hold.” The average target price of $140.41 suggests WMT can climb by 23% from current levels. Plus, the high price estimate of $155 suggests an upside potential of 36% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Costco vs. Walmart: 1 Dividend-Paying Retail Giant Stands Above the Other CF Industries Just Raised Its Dividend by 20% While Its Stock Has Surged 55% in 2026 Taiwan Just Waved a Red Flag for Nvidia Stock Apple vs. Nvidia: One Is Growing 10x Faster and Trades Cheaper. The Better AI Dividend Stock Is Clear.