Privately held Stripe has decided to swing for the fences with its boldest play yet in digital payments. Reuters reported that the fintech heavyweight joined forces with private equity firm Advent International to submit an offer worth more than $53 billion to acquire PayPal Holdings (PYPL).

The proposal values PayPal at $60.50 per share, placing the offer roughly 28% above Tuesday, July 14's closing price. Stripe and Advent plan to jointly own PayPal under the proposal, with each taking an equal stake rather than carving up the business. People familiar with the matter also cautioned that nothing guarantees the discussions will lead to a completed deal.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Reuters reported that banks have committed nearly $50 billion in financing to support the transaction. A successful acquisition would bring together two giants of digital payments under one roof, creating a business capable of processing nearly $3.7 trillion in annual payment volume.

The offer arrives at a pivotal moment for PayPal, which has struggled to maintain its competitive edge in an increasingly crowded digital payments market, a challenge reflected in its latest earnings report. The company also overhauled its leadership this year after replacing former CEO Alex Chriss, who had been brought in to revive its slowing business.

Investors wasted no time cheering the acquisition news, sending PayPal shares up 17.2% after the report emerged on Wednesday, July 15.

William Blair analyst Andrew Jeffrey believes the current proposal simply opens the door to a longer round of negotiations. He expects PayPal's new leadership to reject what could be viewed as a low initial bid and believes Stripe and Advent could ultimately raise their offer to as much as $70 per share.

With PYPL stock already staging a sharp rally, let us see whether it still offers meaningful upside.

About PayPal Stock

Headquartered in San Jose, California, PayPal is a global digital payments platform that serves consumers and businesses through brands such as PayPal, Venmo, Braintree, Xoom, and Honey.

Once among Silicon Valley's biggest success stories, PayPal reached a market value of roughly $360 billion in 2021 during the pandemic-fueled digital payments boom.

Since then, slowing growth, rising competition from Apple's (AAPL) Apple Pay and Alphabet's (GOOGL) Google Pay, and the growing adoption of alternative payment methods have weighed on its business, reducing its market cap to approximately $49 billion.

The stock reflects that difficult journey. PayPal’s shares have fallen 22.3% over the past 52 weeks and slipped 2.9% year-to-date (YTD). However, recent trading tells a different story. The shares have rallied 29.9% over the past month and gained 25.1% during the last five trading sessions, largely fueled by an intraday jump following news of Stripe's takeover proposal.

www.barchart.com

www.barchart.com Even after the recent rally, PayPal still trades at an attractive valuation. The stock currently trades at 8.91 times forward adjusted price-to-earnings and 1.43 times sales. Both multiples remain below the broader industry averages as well as the company's own five-year historical averages, suggesting the valuation still leaves room for opportunity.

In addition, PayPal returns capital to shareholders through dividends. It pays an annual dividend of $0.56 per share, which translates to a dividend yield of 1.18%. Its most recent quarterly dividend of $0.14 per share was paid on June 25 to shareholders of record as of June 4.

PayPal Surpasses Q1 Earnings

Although PayPal delivered stronger-than-expected first-quarter results on Tuesday, May 5, investors still headed for the exits. The fintech reported revenue growth of 7.2% year-over-year (YOY) to $8.35 billion, ahead of analysts' estimate of $8.05 billion. Adjusted EPS also marginally increased from the prior year to $1.34, beating Wall Street's expectation of $1.27.

Even so, the stock slipped 7.7% during intraday trading. The market's reaction centered on PayPal's core business. Branded checkout remains the company's largest and most profitable segment. But total payment volume for online branded checkout increased by only 2% on a currency-neutral basis during Q1 due to sluggish growth in Europe and weakness across the travel sector.

Newer payment products continue to outperform the legacy business, yet that trend has done little to calm investor concerns. Many worry PayPal's traditional checkout leadership could gradually weaken as digital wallets, alternative payment methods, and emerging fintech platforms continue capturing market share.

Overall payment activity remained healthy, with total payment volume rising 11% to $464 billion during the quarter. Management, however, acknowledged that current trends point toward full-year payment volume landing near the lower end of its guidance range, reinforcing concerns about the company's core operations.

Additionally, PayPal is investing aggressively to stabilize growth. The company increased spending across technology, marketing, artificial intelligence (AI) infrastructure, product development, loyalty programs, and organizational restructuring. As a result, operating income declined 5% YOY to $1.5 billion.

Management expects additional pressure during Q2 FY2026, forecasting adjusted EPS to decline by around 9% YOY due to higher investment costs and restructuring expenses, while maintaining that these investments will strengthen long-term growth.

Despite those challenges, PayPal is benefiting from its global scale, recognized brand, and valuable assets such as Venmo and Braintree. The company generated $1.7 billion in adjusted free cash flow during Q1 and repurchased $1.5 billion of shares.

Looking ahead, analysts expect Q2 FY2026 EPS to decline 8.6% YOY to $1.28. Full-year FY2026 earnings are projected to edge up to $5.32 before rising another 8.3% to $5.76 in FY2027.

What Do Analysts Expect for PayPal Stock?

Analyst sentiment on PayPal remains mixed despite the recent rally. Mizuho analyst Dan Dolev downgraded PYPL stock to “Neutral” from “Outperform” and lowered his price target to $50 from $60.

Meanwhile, Clear Street analyst Owen Lau maintained a “Hold” rating and set a $61 price target. Lau believes PayPal stands at a strategic crossroads as investors await clearer evidence that the company's latest reorganization will deliver meaningful results. He also argues that PayPal still possesses significant hidden value that remains masked by its complex organizational structure.

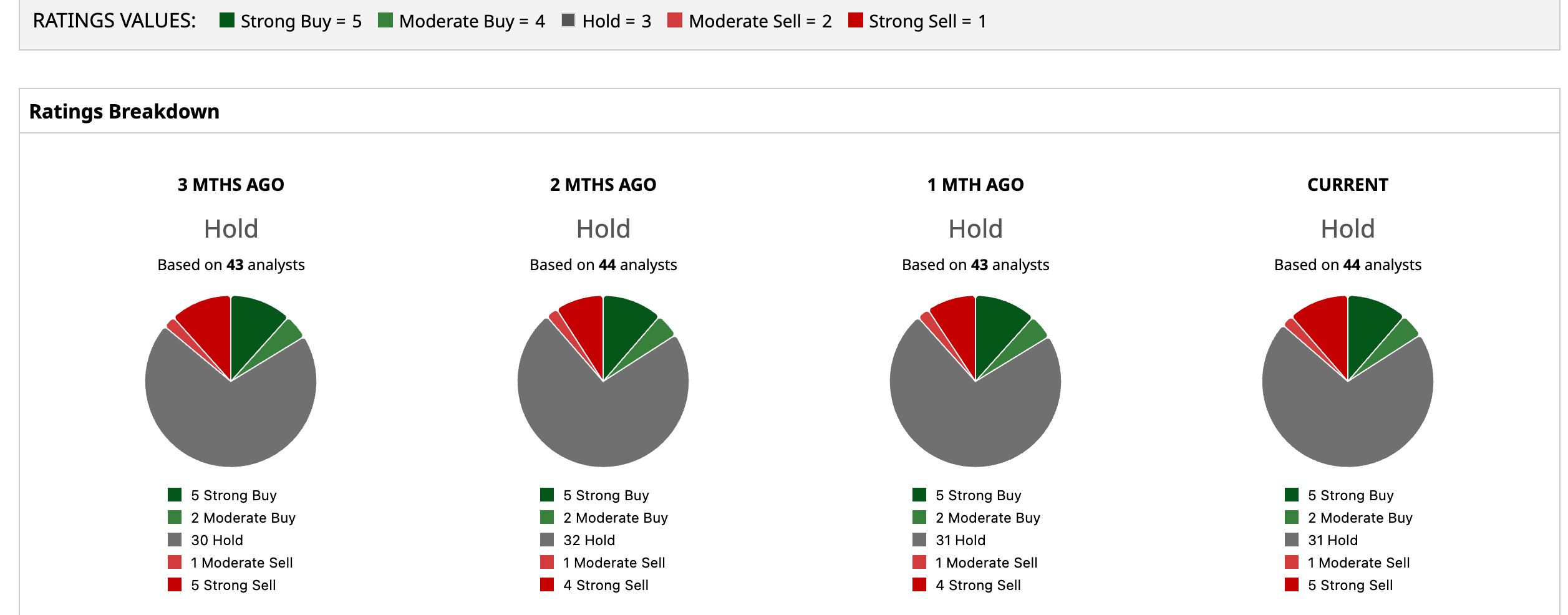

Wall Street remains cautious on PayPal, assigning the stock an overall “Hold” rating. Among 44 analysts covering PYPL, five recommend “Strong Buy,” two rate it “Moderate Buy,” 31 maintain “Hold” ratings, one recommends “Moderate Sell,” and five assign “Strong Sell” ratings.

Although PYPL stock already trades above the average price target of $48.29, the Street-High target of $65 still implies potential upside of 14.6% from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Stripe Wants to Buy PayPal. How You Should Play PYPL Stock Right Now. Quantinuum Just Struck a New Deal with Rolls-Royce. What That Means for QNT Stock Here. Why Jim Cramer Is Telling Retail Investors to Stay Far Away from the IBM Stock Dip Reddit Just Scored a New 'Outperform' Rating. What Comes Next for RDDT Stock.