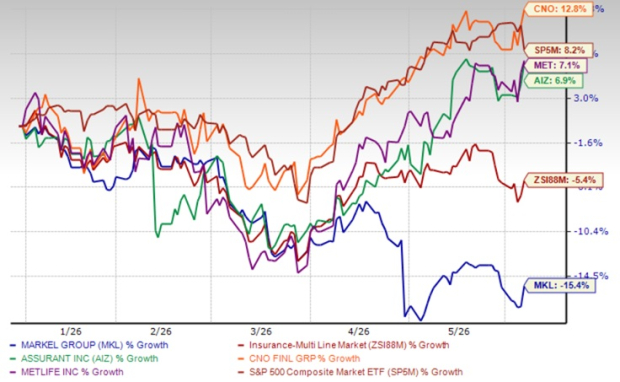

Shares of Markel Group Inc. MKL have declined 15.4% year-to-date compared with the industry’s fall of 5.4%.

Investment portfolio losses, lower premium volume and earnings estimate cuts are pushing the stock down. Markel’s first-quarter 2026 earnings missed expectations, which has weighed on the insurer. However, strong underwriting discipline, strategic acquisitions, international diversification and its niche insurance expertise position the company for sustainable growth ahead.

Some other insurers, like Assurant, Inc. AIZ, CNO Financial Group, Inc. CNO and MetLife, Inc. MET, have risen 6.9%, 12.8% and 7.1%, respectively, in the said time frame.

YTD Price Performance – MKL, AIZ, CNO, MET, Industry & S&P 500

Image Source: Zacks Investment Research

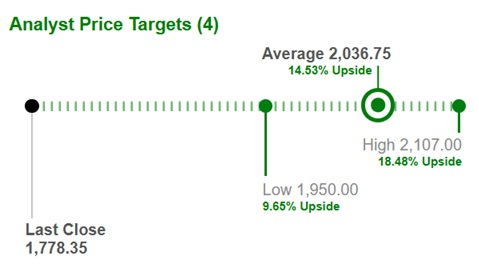

Average Target Price for MKL Suggests Upside

Based on short-term price targets offered by four analysts, the Zacks average price target is $2,036.75 per share. The average suggests a potential 14.5% upside from the last closing price.

Image Source: Zacks Investment Research

MKL’s Valuation

MKL shares are trading at a discount to the industry. Its price-to-book value of 1.26X is lower than the industry average of 2.51X.

Image Source: Zacks Investment Research

MKL’s Favorable ROIC

Return on invested capital (ROIC) in the trailing-12 months was 5.8%, better than the industry average of 2.2%, reflecting MKL’s efficiency in utilizing funds to generate income.

What Aids MKL's Performance?

Markel’s operational results are primarily driven by better performance at its Insurance, Industrial, Financial, Consumer and Other segments. The performance can be attributed to its niche focus, improved pricing and effective risk management. The company expects its specialty insurance operations to remain the primary source of capital generation, supporting expansion and future investments.

MKL looks to double the size of its insurance operations and targets $10 billion of annual insurance premiums in five years. This should lead to $1 billion of annual underwriting profit. The company expects to achieve this goal primarily through organic growth of its existing profitable operations. Investment income should continue to benefit from fixed maturity securities, higher yield and higher average holdings.

Markel strives to grow via acquisitions and organic initiatives to diversify its portfolio and expand its international footprint. Acquisitions have helped the company enhance its surety capabilities. Acquisitions like Valor Environmental and EPI continue to contribute significantly to its top line, highlighting the company's ability to drive growth through this strategy. Markel's acquisition of MECO expands its marine insurance capabilities and strengthens its presence in key international markets such as London, Dubai, Shanghai and Hamburg.

Markel has partnered with hyperexponential to modernize rating, underwriting workflows and integration architecture across its Canadian business. This partnership highlights management's focus on AI-powered underwriting, which could improve risk selection, operational efficiency and long-term profitability.

Markel boasts strong liquidity levels. We expect to see an improvement moving ahead, owing to a robust capital position. MKL exited the first quarter with investments, cash and cash equivalents of $36 billion as of March 31, 2026. The company engages in share buybacks, a prudent way to distribute wealth to its shareholders.

Estimates for MKL

The Zacks Consensus Estimate for Markel’s 2026 earnings per share (EPS) is pegged at $113.55, indicating a year-over-year increase of 17.4%. However, it has witnessed three downward movements and one upward revision over the past 60 days. During this time, the earnings estimate declined 3.4%.

The estimate for 2026 revenues is pegged at $16.88 billion, implying a year-over-year improvement of 10.3%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 8.4% and 2.9%, respectively, from the corresponding 2026 estimates.

Earnings have grown 18.3% in the past five years, better than the industry average of 10.4%.

Risks for MKL

Markel is exposed to catastrophe losses, inducing volatility in underwriting results. Exposure to catastrophe losses always remains a concern, given its unprecedented nature.

Markel has been experiencing an increase in operating expenses due to higher losses and loss adjustment expenses, underwriting, acquisition and insurance expenses.

Markel’s debt levels have increased over the past few years. Senior long-term debt and other debt balance increased 1.8% to $4.4 billion, as of March 31, 2026.

Conclusion

Markel's niche focus, improved pricing, effective management of insurance risk, and focus on developing and maintaining underwriting as well as pricing guidelines should drive growth. However, exposure to catastrophic losses, a rise in debt levels and an increase in operating expenses are concerns.

Coupled with the favourable ROIC, strategic acquisitions and impressive wealth distribution, but recent earnings estimate cuts, it is wise to retain this Zacks Rank #3 (Hold) insurer. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CNO Financial Group, Inc. (CNO): Free Stock Analysis Report

MetLife, Inc. (MET): Free Stock Analysis Report

Assurant, Inc. (AIZ): Free Stock Analysis Report

Markel Group Inc. (MKL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).