Resmed RMD benefits from the acquisition-led expansion of its Residential Care Software segment, which is poised to continue supporting its growth in the coming quarters. The company continues to expand its mask portfolio through product innovation and targeted initiatives that support resupply. Solid financial health further adds to the stock’s appeal. Yet, headwinds from macroeconomic pressures and intense competition may present operational risks for Resmed.

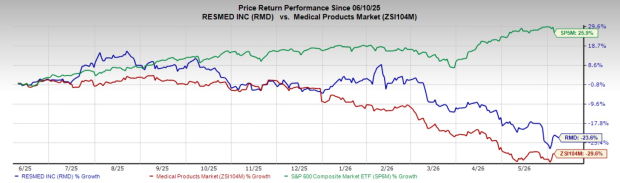

Over the past year, this Zacks Rank #3 (Hold) stock has dropped 23.6% compared with the 29.6% decline of the industry and the S&P 500 Composite’s 25.9% growth.

The renowned medical device company has a market capitalization of $28.44 billion. RMD has an earnings yield of 5.7% compared with the industry’s yield of 3.2%. RMD’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 3.26%.

Let’s delve deeper.

Upsides for RMD Stock

Strategic Pacts to Boost Residential Care Software Business: The Residential Care Software business remains a key synergistic enabler of Resmed’s Sleep and Breathing Health franchise. The company has historically used strategic buyouts to expand its SaaS footprint, including MEDIFOX DAN in 2022 to enter Germany. In 2018, RMD acquired HEALTHCAREfirst, while the addition of MatrixCare broadened its exposure to skilled nursing and senior living.

Image Source: Zacks Investment Research

In 2016, Resmed acquired Brightree to strengthen its connected healthcare software capabilities. The segment continues to show steady underlying demand in select verticals. In the third quarter of fiscal 2026, Residential Care Software revenues increased 4% on a constant-currency basis, driven by growth in the MEDIFOX DAN, Home and Hospice, and HME verticals, partially offset by weaker performance in Senior Living and Long-Term Care.

Mask Innovation and Resupply: Resmed has been a consistent innovator in small nasal, nasal pillows and full-face masks, improving patient comfort while reducing size and weight. The company continues to broaden its AirFit and AirTouch platforms and launch new designs that address fit, leak and adherence — all critical to long-term therapy usage.

Resmed also remains focused on expanding the mask portfolio with new platforms and driving mask resupply through education, awareness and execution across provider and direct-to-consumer channels. This resupply focus supports recurring revenues and helps the company retain patients as they move through the care pathway. In the third quarter of fiscal 2026, Americas masks and other sales increased 14%, reflecting continued growth in both the mask portfolio and resupply and incremental revenues from VirtuOx, which ResMed acquired in the fourth quarter of fiscal 2025.

Financial Flexibility: Resmed exited the third quarter of fiscal 2026 with $1.66 billion in cash and cash equivalents while maintaining a modest leverage profile. Short-term debt was $260 million, and long-term debt was $404 million at quarter-end. The company’s debt-to-capital ratio improved 0.1% sequentially to 5.9%, reflecting relatively contained balance sheet risk compared with many med-tech peers.

What Ails Resmed?

Macroeconomic Sensitivity: Resmed remains exposed to macroeconomic conditions, geopolitical instability, and the impact of tariffs and trade actions on its suppliers and input costs. These factors can weigh on demand, influence pricing and raise operating costs through higher freight, labor or component expenses, while currency volatility can also affect reported results.

Competitive Landscape: The market for sleep-disordered breathing (SDB) is highly competitive on product price, features, reliability and supply performance. The disparity between Resmed’s resources and those of some competitors can widen as the healthcare industry consolidates, and large providers and payers increase purchasing leverage. Certain competitors are affiliated with customers, which can make it harder for Resmed to defend its share in specific channels. Competition can intensify as supply availability improves and providers reassess purchasing decisions, which can lead to pricing pressure in devices, masks and accessories, and can increase the cost of retaining accounts.

RMD Stock’s Estimate Trend

The Zacks Consensus Estimate for RMD’s fiscal 2026 earnings per share (EPS) has improved 0.4% to $11.13 in the past 60 days.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $5.65 billion, up 9.8% from the year-ago reported figure.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Align Technology ALGN and Integra LifeSciences IART.

Globus Medical has an earnings yield of 5.9% compared to the industry’s negative 3.2% yield. Its earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 26.3%. GMED shares have rallied 27.4% against the industry’s 6% fall over the past year.

GMED sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Align Technology, sporting a Zacks Rank #1, has an estimated long-term earnings growth rate of 10.3% compared with the industry’s 9.6% growth. Shares of the company have dropped 8.5% against the industry’s 6.4% rise. ALGN’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 7.8%.

Integra LifeSciences, carrying a Zacks Rank #2 (Buy), has an earnings yield of 14.2% against the industry’s negative 3.2% yield. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 16.7%. IART shares have rallied 21.2% against the industry’s 5.9% decline over the past year.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Align Technology, Inc. (ALGN): Free Stock Analysis Report

ResMed Inc. (RMD): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).