Crescent Energy Company CRGY is drawing attention as its oil-weighted portfolio, tighter execution and integration progress improve the visibility of its 2026 cash flow profile.

The setup is not without risk, but the company’s Permian progress, minerals exposure and capital-return flexibility give investors a clearer framework for evaluating the stock.

Crescent’s Oil Mix Supports Margins

Crescent’s production base is tilted toward oil and liquids, which generally carry better economics than dry gas. That mix helps support margins when commodity markets are uneven.

The company also uses marketing and hedging to reduce exposure to regional price swings, particularly in natural gas. That does not eliminate commodity risk, but it can make cash flows more predictable across cycles.

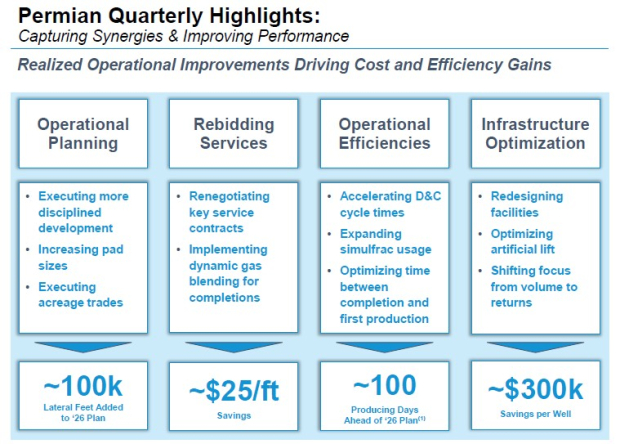

CRGY’s Permian Deal Is Paying Off

The Vital Energy integration is the central near-term catalyst for CRGY. By the first quarter of 2026, Crescent had already captured about $120 million of synergies, above its initial target.

Operational gains are also showing up in the development plan. Crescent added roughly 100,000 lateral feet to its 2026 program, accelerated production by about 100 producing days and reduced well costs by more than $500,000 per well versus the prior operator.

Crescent’s Cash Flow Case for 2026

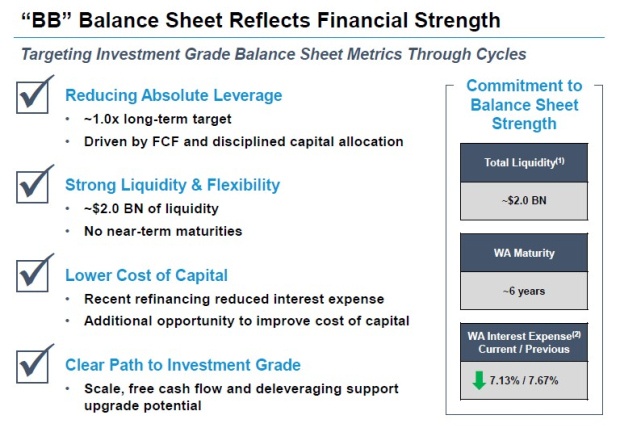

The financial case rests on free cash flow. Management expects roughly $1 billion of 2026 levered free cash flow at current commodity prices, helped by a lower-capital-intensity asset base.

That matters because liquidity and maturity timing shape capital flexibility. Crescent has about $2 billion of liquidity and no significant near-term debt maturities, giving it room to fund development, pay dividends, repurchase shares and pursue selective deals.

Diamondback Energy FANG offers a useful comparison because it is a Permian-focused oil and gas producer. For investors watching Crescent’s Permian integration, FANG remains a relevant benchmark for basin execution and capital discipline.

CRGY’s Minerals Unit Adds Stability

Crescent’s Minerals & Royalties business adds another layer to the cash flow story. The segment is expected to generate about $200 million of EBITDA in 2026.

The appeal is its low-capital structure. With minimal capital requirements and diversified exposure across key U.S. basins, the business can provide steadier cash generation alongside Crescent’s working-interest portfolio.

EOG Resources EOG is another relevant name in the U.S. exploration and production space. Its scale and onshore resource base make it a useful peer when investors compare asset quality, execution and commodity exposure.

Crescent’s Key Risks Still Matter

Commodity prices remain the largest swing factor. Weaker oil, natural gas or NGL prices could pressure cash flow, slow drilling activity or limit shareholder returns.

Debt is another constraint. Crescent carries $5.2 billion of long-term debt, and debt-to-capitalization is above 50%, leaving less margin for error if prices weaken or acquisition benefits take longer to materialize.

CRGY’s Ratings Reinforce the Bull Case

The bottom line is that Crescent’s 2026 outlook looks more constructive as Permian synergies build, minerals cash flow expands and free cash flow supports capital flexibility. The stock still requires tolerance for commodity and balance-sheet risk.

CRGY currently carries a Zacks Rank #1 (Strong Buy). It also has a VGM Score of A, Value Score of A, Growth Score of D and Momentum Score of B.

You can see the complete list of today’s Zacks #1 Rank stocks here.

That combination points to a favorable near-term setup for investors looking for value and momentum exposure. Growth is not the main appeal, but the Rank and Style Scores support a constructive view for investors comfortable with energy-sector cyclicality.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EOG Resources, Inc. (EOG): Free Stock Analysis Report

Diamondback Energy, Inc. (FANG): Free Stock Analysis Report

Crescent Energy Company (CRGY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).