Salesforce, Inc. CRM has become one of the strongest cash-generating companies in the software industry, giving it significant flexibility to reward shareholders while continuing to invest in growth initiatives. The company’s robust cash flow performance is increasingly becoming a key part of the investment story.

In the first quarter of fiscal 2027, Salesforce generated a record $6.7 billion in operating cash flow and $6.6 billion in free cash flow. This strong cash generation was supported by healthy demand for its cloud applications, expanding adoption of AI offerings such as Agentforce and continued focus on operational efficiency. Revenues increased 13% year over year to $11.13 billion during the quarter, demonstrating that the company is still growing while generating substantial cash.

Salesforce has been using this financial strength to aggressively return capital. During the first quarter, the company launched a massive $25 billion accelerated share repurchase program, representing half of its authorized $50 billion buyback plan. The repurchase reduced diluted share count by 10% year over year, helping boost earnings per share and increasing the ownership stake of existing investors.

Salesforce’s balance sheet also remains healthy. The company ended the quarter with nearly $11.8 billion in cash and marketable securities, providing ample liquidity to fund strategic investments, acquisitions and shareholder returns simultaneously. The company’s growing profitability further supports this strategy. First-quarter GAAP operating margin expanded 130 basis points to 21.1%, while non-GAAP operating margin improved 250 basis points to 34.8%. These improvements indicate that Salesforce is converting a larger portion of revenues into earnings and cash.

With strong cash flow, rising margins and a large buyback authorization in place, Salesforce appears well-positioned to continue delivering meaningful shareholder returns while pursuing long-term growth opportunities. The Zacks Consensus Estimate for CRM’s fiscal 2027 revenues is pegged at $46.09 billion, indicating a year-over-year increase of 11%.

How Do Salesforce’s Peers Compare on Shareholder Returns?

Two major Salesforce competitors that also generate strong cash flows and return capital to shareholders are Microsoft Corporation MSFT and Oracle Corporation ORCL.

Microsoft remains one of the strongest cash generators in the technology sector. In the first nine months of fiscal 2026, the company produced more than $127 billion in operating cash flow and $47 billion in free cash flow. This financial strength allows Microsoft to maintain a balanced capital return strategy through both dividends and share repurchases. During the first three quarters of fiscal 2026, the company returned more than $37 billion to shareholders through buybacks and dividends. Its expanding cloud business, led by Azure’s 40% revenue growth in the latest reported quarter, continues to support rising cash generation and shareholder-friendly actions.

Oracle is also increasing shareholder returns as its cloud business scales. In fiscal 2026, Oracle generated approximately $32 billion in operating cash flow. The company has consistently repurchased shares while maintaining a quarterly dividend. In fiscal 2026, it returned $5.3 billion to shareholders. Oracle’s cloud infrastructure revenues surged nearly 77% year over year in fiscal 2026, helping improve cash flow generation. The company has increasingly used this cash to support both growth investments and shareholder rewards.

While Microsoft and Oracle have impressive capital return programs, Salesforce’s recent $50 billion buyback authorization highlights its growing confidence in future cash generation and commitment to enhancing shareholder value.

Salesforce’s Price Performance, Valuation and Estimates

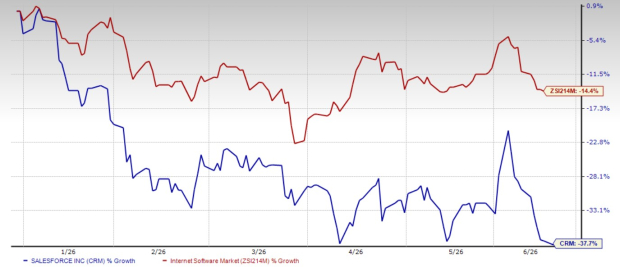

Shares of Salesforce have plunged 37.7% year to date, while the Zacks Internet – Software industry has fallen 14.4%.

Salesforce YTD Price Return Performance

Image Source: Zacks Investment Research

From a valuation standpoint, CRM trades at a forward price-to-earnings ratio of 11.25, significantly below the industry’s average of 25.65.

Salesforce Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Salesforce’s fiscal 2027 and 2028 earnings implies a year-over-year increase of approximately 12.8% and 9.7%, respectively. Estimates for fiscal 2027 and 2028 have remained unchanged over the past 30 days.

Image Source: Zacks Investment Research

Salesforce currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Oracle Corporation (ORCL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).