Stitch Fix, Inc. SFIX is rebuilding its investment case around steadier revenue trends, higher client spending and better engagement. The turnaround is still developing, but recent results show more traction than the stock’s uneven performance suggests.

The key question for investors is whether these gains can become durable growth while the company maintains discipline on profitability and acquisition costs.

SFIX Revenue Growth Is Gaining Traction

Stitch Fix reported fiscal third-quarter revenues of $340.3 million, up 4.7% year over year. The quarter marked its fifth consecutive period of year-over-year revenue growth on an adjusted basis, helped by average order value gains, stronger client spending and assortment improvements. The company posted an adjusted loss of 1 cent per share, which was narrower than the expected loss of 6 cents.

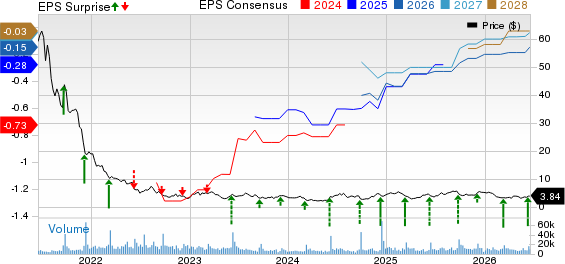

Stitch Fix, Inc. Price, Consensus and EPS Surprise

Stitch Fix, Inc. price-consensus-eps-surprise-chart | Stitch Fix, Inc. Quote

Management also raised its fiscal 2026 revenue outlook to $1.346-$1.351 billion, indicating 6.2-6.6% growth. That higher guide strengthens the recovery narrative because SFIX is gaining ground even as the apparel backdrop remains uneven.

The company also said its revenue growth rate was more than four times the total U.S. apparel, footwear and accessories market in the most recent quarter. The Gap Inc. GAP and Abercrombie & Fitch Co. ANF are relevant comparison points for investors tracking discretionary apparel demand, although Stitch Fix’s curated model makes its operating signals different.

Stitch Fix Is Winning More From Each Client

Revenue per active client reached $578 in the fiscal third quarter, up 6.6% year over year and the highest level reported by the company. That marked the ninth straight quarter of year-over-year growth in the metric.

The improvement matters because active clients were still down 1.9% year over year, even after rising 0.9% sequentially to 2.309 million. Stitch Fix is producing more from each client before the client base has fully stabilized.

Average order value increased year over year for the 11th consecutive quarter. Higher items per Fix, broader adoption of larger Fixes, higher average unit retail and a better assortment mix helped lift order size.

SFIX Category Expansion Is Opening New Paths

Category expansion is giving Stitch Fix more ways to capture wardrobe spending. In women’s, activewear and athleisure grew about 50% year over year, while sandals, skirts and sneakers also posted gains.

Men’s remained a bright spot, delivering double-digit growth for the fourth straight quarter. Shorts, casual shoes and short-sleeve woven tops each increased more than 30%, showing that the business is gaining traction beyond its core women’s offering.

The company sees activewear, athleisure, footwear and accessories as meaningful long-term opportunities. By adding brands and supporting head-to-toe outfitting, Stitch Fix can pursue larger baskets and deeper wardrobe relevance with existing clients.

Stitch Fix Uses AI to Deepen Engagement

Stitch Fix’s personalization model combines stylists, client data and artificial intelligence. Stitch Fix Vision, its AI-powered style visualization platform, gives clients personalized, shoppable outfit imagery tied to their style profiles and current trends.

Clients using Vision have generated more than a 100% lift in Freestyle spending over 90 days. That signal is important because better discovery can support conversion, repeat engagement and higher spend.

AI is also being used outside the customer interface. Stitch Fix is applying these tools to inventory management, intelligent pricing, marketing execution and private-brand product development, including a faster design process for private-brand assortments.

How SFIX Signals Shape the Investor View

The bottom line is that SFIX’s turnaround has become more credible, but not risk-free. Revenue is growing again, spending per active client is at a record level and category expansion is adding new growth paths, while client growth and margin pressure still require monitoring.

Valuation also adds context. SFIX trades at 0.37X forward 12-month sales, below the Zacks sub-industry at 1.85X and close to its five-year median of 0.36X. That discount may draw interest, but execution will likely decide whether investors become more constructive.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #3 (Hold), which supports a balanced stance. This rank can be appropriate for investors who want to watch continued execution rather than assume the recovery is complete. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF): Free Stock Analysis Report

The Gap, Inc. (GAP): Free Stock Analysis Report

Stitch Fix, Inc. (SFIX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).