Johnson & Johnson’s JNJ stock has declined 3% in the past three months despite robust first-quarter 2026 results announced in January and fundamentally positive developments in the period. J&J’s stock has significantly outperformed the broader industry over the past year. However, after the stock rose significantly, many investors seem to have locked in gains. Investors also seem to have shifted investments away from defensive healthcare stocks toward faster-growing sectors, especially technology and artificial intelligence (AI) companies, which have been performing strongly.

As a result of profit-taking and this shift toward technology and AI stocks, J&J's shares faced some short-term weakness and have declined recently, even though the company's underlying business remains relatively stable. So, does this short-term weakness indicate a buying opportunity for J&J stock?

Let’s understand the company’s strengths and weaknesses to better analyze how to play J&J stock amid the recent price suppression.

JNJ’s Innovative Medicine Showing Consistent Growth

J&J’s Innovative Medicine unit is showing a growth trend, despite the loss of exclusivity (LOE) of the blockbuster drug, Stelara. Growth is being driven by J&J’s key drugs like Darzalex, Erleada and Tremfya. New drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato are also contributing significantly to growth.

The segment has recorded four consecutive quarters of sales of more than $15 billion despite the LOE of Stelara.

In 2026, J&J expects accelerated growth in the Innovative Medicine segment despite Stelara LOE. The growth is expected to be driven by its key products such as Darzalex, Tremfya, Spravato, Carvykti and Erleada, as well as increased contribution from new launches like Icotyde, Rybrevant and Inlexzo.

J&J’s Recent Significant Pipeline Progress

In 2025, J&J invested more than $32 billion in R&D and M&A, including the acquisitions of Intra-Cellular Therapies and Halda Therapeutics.

J&J also rapidly advanced its pipeline in the past year, attaining significant clinical and regulatory milestones that will help drive growth through the back half of the decade. In the past year, it has gained approval for new products like Inlexzoh/TAR-200, a first-of-its-kind drug-releasing system, for treating high-risk non-muscle invasive bladder cancer, Imaavy (nipocalimab) for treating generalized myasthenia gravis and Icotyde (icotrokinra), an oral targeted peptide inhibitor of the IL-23 receptor, for treating moderate-to-severe plaque psoriasis (PsO). J&J markets Icotyde in partnership with Protagonist Therapeutics PTGX.

J&J believes that nipocalimab has a pipeline-in-a-product potential and Protagonist Therapeutics-partnered Icotyde has the potential to revolutionize the treatment of plaque psoriasis with a once-a-day pill. It has the potential to be J&J’s largest product ever, with $10 billion in sales potential.

J&J’s new cancer drugs, Carvykti, Tecvayli, Talvey and Rybrevant/Lazcluze are contributing significantly to top-line growth driven by market share gains. J&J’s acquisition of Intra-Cellular Therapies added antidepressant drug, Caplyta, to its neuroscience portfolio, which is approved for the treatment of schizophrenia, depression in both bipolar 1 and 2, and major depressive disorder.

The company expects a more pronounced impact from new products in 2026 than in 2025. J&J expects that contributions from its new product launches across oncology, immunology and neuroscience will increase as the year progresses.

J&J believes 10 of its new products/pipeline candidates in the Innovative Medicine segment have the potential to deliver peak sales of $5 billion, including Talvey, Tecvayli, Imaavy, Caplyta, Inlexzo, Rybrevant plus Lazcluze and Icotyde.

J&J’s MedTech Segment Sales Improving

J&J’s MedTech business has improved in the last four quarters, driven by the acquired cardiovascular businesses, Abiomed and Shockwave, as well as Surgical Vision and wound closure in Surgery. Improvements in J&J’s electrophysiology business are also driving growth.

Moreover, the potential separation of its Orthopaedics franchise into a standalone orthopedics-focused company, called DePuy Synthes, should improve its MedTech unit’s growth and margins. The Orthopaedics franchise has been a slow-growth business for J&J.

In 2026, J&J expects better growth in the MedTech business than 2025 levels, driven by increased adoption of newly launched products across Cardiovascular, Surgery and Vision portfolios.

However, the company continues to face headwinds in China. Sales in China are being hurt by the impact of the volume-based procurement (VBP) program, which is a government-driven cost containment effort in China. J&J expects continued impacts from VBP issues in China in 2026, mainly in the second half.

Patent Expiration of J&J’s Drug Stelara & Other Headwinds

J&J lost U.S. patent exclusivity of Stelara in 2025. Stelara was a key top-line driver for J&J, accounting for around 18% of J&J’s Innovative Medicine unit’s sales in 2024, before it lost patent exclusivity in 2025.

Several biosimilar versions of Stelara were launched in the United States in 2025 as the drug lost patent exclusivity.

According to patent settlements and license agreements, Amgen AMGN, Teva Pharmaceutical Industries TEVA, Samsung Bioepis/Sandoz and some other companies launched Stelara biosimilars in 2025. Stelara’s LOE negatively impacted the Innovative Medicines segment’s growth by 920 basis points and total revenues by 540 basis points in the first quarter. Stelara’s sales declined 62% in the first quarter, which was steeper than expected. J&J expects generic impact for both Simponi and Opsumit to begin in 2026 as the drugs lose patent protection.

J&J faces more than 74,000 lawsuits for its talc-based products, primarily baby powders. The lawsuits allege that its talc products contain asbestos, which caused many women to develop ovarian cancer. While the company has taken steps to resolve many of these matters, litigation remains an overhang that can lead to high costs, create negative headlines and weigh on investor sentiment.

J&J Stock Price, Valuation and Estimates

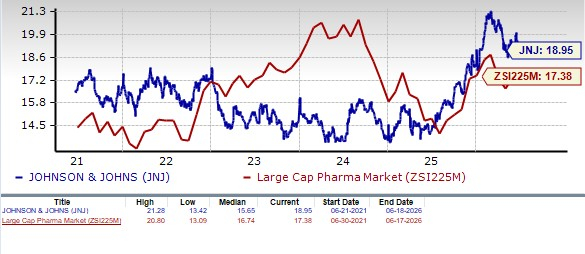

J&J’s shares have outperformed the industry over the past year. The stock has risen 52.5% in the past year compared with 25.5% appreciation of the industry. The stock has also outperformed the sector and the S&P 500 Index, as seen in the chart below.

JNJ Stock Outperforms Industry, Sector & S&P 500

From a valuation standpoint, J&J is slightly expensive. Going by the price/earnings ratio, the company’s shares currently trade at 18.95 forward earnings, higher than 17.38 for the industry. The stock is also trading above its five-year mean of 15.65.

JNJ Stock Valuation

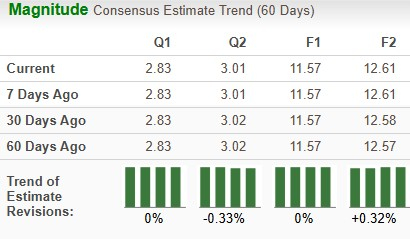

The Zacks Consensus Estimate for 2026 earnings has been stable at $11.57 per share over the past 60 days, while that for 2027 earnings has gone up from $12.57 per share to $12.61 per share over the same time frame.

JNJ Estimate Movement

Stay Invested in J&J’s Stock

J&J’s biggest strength is its diversified business model, as it operates through pharmaceuticals and medical devices divisions, which reduces dependence on any single product or market. It has more than 275 subsidiaries and boasts 28 platforms or products with more than $1 billion in annual sales, with the aim of adding even more. Its diversification helps it to withstand economic cycles more effectively. It also boasts strong cash flows and has increased its dividends for 64 consecutive years. J&J believes that the depth of its portfolio and pipeline is stronger than ever.

The company expects 2026 to be a year of accelerated growth. The company expects both its Innovative Medicines and MedTech segments to deliver stronger growth this year. The company is confident that it can achieve its target of generating around $100 billion in revenues in 2026. It expects sales to continue to improve in 2027, with a “line of sight” to double-digit growth by the end of the decade. J&J believes that it is already achieving this growth. Though J&J’s total revenues are currently rising in a mid-single-digit range, excluding Stelara, J&J’s top line grew in a double-digit range in the first quarter.

Despite headwinds like the legal battle surrounding its talc lawsuits, the Stelara patent cliff, the upcoming LOE of key drugs Opsumit and Simponi and softness in MedTech China, J&J looks quite confident that it will be able to navigate these challenges.

J&J’s price appreciation, rising estimates, consistent earnings and sales growth, important new launches and pipeline depth suggest that one should stay invested in this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Investors with a long-term horizon can use the recent dip as a buying opportunity.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Amgen Inc. (AMGN): Free Stock Analysis Report

Teva Pharmaceutical Industries Ltd. (TEVA): Free Stock Analysis Report

Protagonist Therapeutics, Inc. (PTGX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).