Pembina Pipeline Corporation PBA is one of Canada’s premier energy infrastructure companies, operating a vast network of pipelines, gas gathering and processing facilities, liquids infrastructure, storage assets and export terminals. Its integrated business model provides end-to-end services that connect production sites with key markets across North America and beyond. Backed largely by long-term, fee-based agreements, Pembina Pipeline generates stable and predictable cash flows while maintaining a strong focus on operational safety, reliability and disciplined capital allocation. The company continues to invest in strategic infrastructure projects aimed at supporting resource development, improving market connectivity and reinforcing its competitive position in a changing global energy environment.

For investors, the central question is whether the stock’s recent strong performance justifies maintaining a position for additional upside or warrants a reassessment of valuation levels. Evaluating Pembina Pipeline’s financial strength, favorable industry dynamics and long-term growth opportunities can provide valuable insight into whether the stock remains an attractive holding.

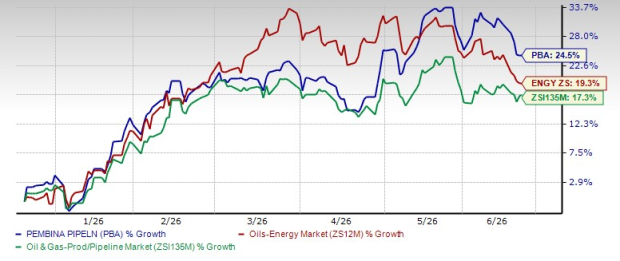

PBA’s Price Performance

In the past six months, PBA’s shares have gained 24.5%, outperforming the broader oil and energy sector's rise of 19.3% and the Oil & Gas Production and Pipelines sub-industry’s growth of 17.3%.

PBA’s Six-Month Stock Performance

Image Source: Zacks Investment Research

Core Strengths of Pembina Pipeline

Strong Fee-Based Business Model Provides Stable Cash Flows: Pembina Pipeline's business remains heavily supported by long-term, fee-based contracts, insulating earnings from commodity price volatility. Management highlighted that the fee-based business is performing ahead of plan and continues to support the company's target of approximately 5% annual adjusted EBITDA-per-share growth through 2026. This predictable cash flow profile allows Pembina Pipeline to fund growth projects, maintain balance sheet strength and support shareholder returns even during periods of energy market uncertainty. The stability of its pipeline and midstream infrastructure network makes the company particularly attractive for income-oriented and risk-conscious investors.

Upward Revision to 2026 EBITDA Guidance Signals Momentum: Following a strong first quarter, management increased its 2026 adjusted EBITDA guidance range to C$4.35-C$4.55 billion, representing a midpoint increase of approximately C$175 million from prior expectations. The upgrade reflects stronger marketing performance, improved commodity-related opportunities and favorable market conditions. Raising guidance early in the year demonstrates confidence in operating performance and suggests earnings momentum is stronger than originally anticipated. Companies that consistently outperform and raise forecasts often command higher valuation multiples over time.

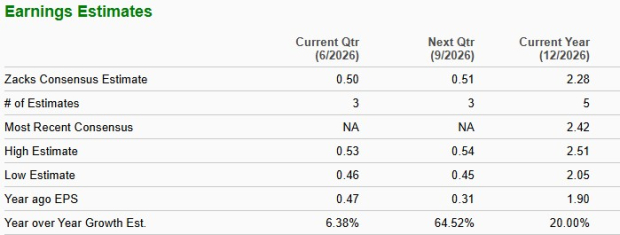

A Positive 2026 Earnings Estimate: The Zacks Consensus Estimate for PBA’s 2026 earnings is pegged at $2.28 per share, indicating 20% year-over-year growth. The positive earnings estimate outlook makes the stock attractive for investors.

PBA’s Earnings Estimate Overview

Image Source: Zacks Investment Research

Significant Growth Project Portfolio Creates Long-Term Upside: The company continues to advance a substantial portfolio of projects, including Cedar LNG, the RFS IV fractionator, Alliance Pipeline expansion and the Greenlight Electricity Center. Several projects are progressing on time and under budget, while others are approaching final investment decisions. These developments should contribute incremental earnings over the next several years and expand Pembina Pipeline's integrated value chain. Importantly, many of these projects are backed by customer demand and long-term contracts, increasing the likelihood that future capital investments will generate attractive returns.

Risks That Could Hinder PBA's Growth

Declining EBITDA in the First Quarter of 2026: Despite a solid quarter overall, first-quarter adjusted EBITDA fell approximately 3% from the prior year. Management attributed the decline partly to the new Alliance Pipeline toll structure and revenue-sharing mechanisms, as well as weaker NGL marketing economics earlier in the quarter. While the company expects improvement going forward, the decline highlights that regulatory changes, contract renegotiations and market conditions can offset volume growth and operational improvements, creating headwinds for earnings expansion.

Earnings Remain Exposed to Commodity-Related Marketing Activities: Although Pembina Pipeline's core business is fee-based, a meaningful portion of earnings still comes from marketing operations that are influenced by commodity prices, frac spreads and market conditions. Management acknowledged that guidance improvements were driven largely by stronger marketing expectations. If propane prices weaken, frac spreads narrow, or global energy markets soften, marketing profits could decline materially. This introduces earnings variability and can make financial results less predictable than those of a purely regulated pipeline operator.

Elevated Leverage Due to Growth Investments: Pembina Pipeline expects its debt-to-adjusted EBITDA ratio to range between approximately 3.5x and 3.7x in 2026. While manageable for a midstream company, leverage remains elevated due to ongoing capital spending and investments such as Cedar LNG. Rising interest rates, weaker earnings, or unexpected project expenditures could place additional pressure on the balance sheet. Investors seeking highly conservative financial profiles may view this leverage level as a potential concern.

Dependence on Producer Activity Levels: The company’s infrastructure volumes depend heavily on drilling activity and production levels from upstream energy companies. While management expects long-term production growth in Western Canada, short-term activity can fluctuate due to commodity price swings, mergers among producers, or changes in drilling plans. If upstream operators reduce capital spending, throughput volumes on Pembina Pipeline’s pipelines and facilities could decline, affecting revenues.

Final Thoughts on PBA Stock

Pembina Pipeline appears well-positioned with its stable fee-based contract structure and upward 2026 EBITDA revision that supports predictable cash flows. Ongoing expansion projects and LNG export opportunities also provide visible long-term growth potential, while positive earnings expectations reinforce confidence in its operational outlook.

However, recent EBITDA pressure, exposure to commodity market fluctuations and the company’s heavy capital spending phase introduce near-term financial risks and potential earnings volatility. Given the balance between solid long-term fundamentals and short-term uncertainties, a wait-and-see approach appears prudent for this company, allowing investors to participate in structural upside while waiting for clearer earnings traction.

Key Picks

Currently, PBA has a Zacks Rank #3 (Hold).

Investors interested in the energy sector may consider some top-ranked stocks like Global Partners LP GLP, Crescent Energy Company CRGY and CrossAmerica Partners LP CAPL, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Global Partners is a Delaware limited partnership formed by affiliates of the Slifka family. It owns, controls or has access to one of the largest terminal networks of refined petroleum products in New England. The Zacks Consensus Estimate for GLP’s 2026 earnings indicates 113.1% year-over-year growth.

Crescent Energy is a U.S. onshore oil and gas producer focused on three major basins: the Eagle Ford in Texas, the Permian in Texas and New Mexico and the Uinta in Utah. The Zacks Consensus Estimate for CRGY’s 2026 earnings indicates 39.4% year-over-year growth.

CrossAmerica Partners engages in the wholesale distribution of motor fuels, consisting of gasoline and diesel fuel, and owns and leases real estate used in the retail distribution of motor fuels. The Zacks Consensus Estimate for CAPL’s 2026 earnings indicates 4% year-over-year growth.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Global Partners LP (GLP): Free Stock Analysis Report

Pembina Pipeline Corp. (PBA): Free Stock Analysis Report

CrossAmerica Partners LP (CAPL): Free Stock Analysis Report

Crescent Energy Company (CRGY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).