Encore Capital Group ECPG has rallied sharply, with shares up 58.1% year to date. The move reflects stronger collections, favorable U.S. purchasing conditions and improving earnings expectations.

Image Source: Zacks Investment Research

The question is whether those drivers can keep working after the rebound. For now, ECPG’s outlook rests on supply, execution and funding discipline.

Why ECPG Benefits From U.S. Debt Supply

Encore is benefiting from a steady flow of receivable portfolios in the United States, its largest revenue contributor. Elevated lending activity, near-peak charge-offs and stable delinquency trends continue to support supply.

Scale matters in this environment. Smaller buyers remain pressured by regulatory challenges and limited funding access, while Encore’s balance sheet and funding flexibility help it compete for larger portfolios at attractive returns.

PRA Group, Inc. PRAA is a relevant peer because it also acquires and collects nonperforming loan portfolios. Its presence keeps investor attention on portfolio supply, pricing and collections efficiency across the debt-purchasing industry.

How Encore Capital Is Turning Supply Into Growth

Encore converted favorable supply into record first-quarter 2026 collections of $718.4 million, up 19% year over year. MCM, its U.S. business, generated $556 million of collections, up 23%.

Management raised its 2026 global collections outlook to nearly $2.8 billion, representing 8% growth, while keeping global portfolio purchase guidance at $1.4-$1.5 billion. Higher forward flows should improve revenue visibility as the recently purchased portfolios season.

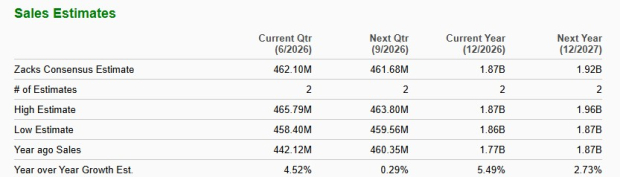

The Zacks Consensus Estimate for ECPG’s sales suggests growth of 5.5% for 2026 and 2.7% for 2027.

Image Source: Zacks Investment Research

What is ECPG’s Technological Drive Changing

Technology is becoming a bigger part of the ECPG story. New tools, enhanced digital capabilities and operating innovation have helped the company reach more consumers, generate more payments and expand its payer book.

Collections exceeded forecasts by $46 million in the first quarter, and expected future recoveries increased by $16.7 million. Management expects future cash overperformance to shift gradually into portfolio revenues as collection forecasts adjust upward.

Where Encore Capital Still Looks Vulnerable

ECPG’s U.S. strength also creates concentration risk. Cabot continues to face subdued consumer lending, low delinquencies and strong competition in Europe, limiting purchases and ERC growth.

Costs and leverage remain watch items. Rising legal collection activity could pressure margins if collections slow, while borrowings of $4.03 billion leave earnings sensitive to higher funding costs.

FirstCash Holdings, Inc. FCFS offers a different consumer-finance comparison point, with pawn operations accounting for more than 90% of net revenues. Its model is less tied to charged-off receivable purchases, giving investors another way to view consumer-credit exposure.

How ECPG’s Ratings Fit the Bull Case

The bottom line is balanced but constructive. Encore Capital’s U.S. purchasing strength, record collections and improving portfolio revenue setup support near-term investor interest, while Cabot softness, legal costs and debt funding keep the risk profile from looking one-sided.

ECPG currently sports a Zacks Rank #1 (Strong Buy). On the other hand, PRA Group and FirstCash Holdings carry a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank stocks here.

ECPG also has a Value Score of B, VGM Score of C, Growth Score of D and Momentum Score of F.

The Rank supports a favorable near-term earnings-revision backdrop. The Style Scores are mixed: value is the clearest positive, while weaker growth and momentum scores suggest the stock does not screen strongly across every factor.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PRA Group, Inc. (PRAA): Free Stock Analysis Report

FirstCash Holdings, Inc. (FCFS): Free Stock Analysis Report

Encore Capital Group Inc (ECPG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).