Mission Produce, Inc. AVO is trying to turn a larger avocado platform into steadier earnings power. Its vertically integrated model gives it control across sourcing, farming, packing, distribution and ripening.

The challenge is that avocados remain a price-sensitive category. Volume growth can help, but second-quarter fiscal 2026 showed that low prices and fruit-size imbalances can quickly pressure margins.

How AVO Built a Global Avocado Platform

Mission Produce sources, grows, packs, distributes and ripens avocados for retail, wholesale and foodservice customers. That structure helps the company manage supply, quality and logistics across a market where timing and source region matter.

Marketing and Distribution remains the core business, accounting for 92% of fiscal 2025 revenues. International Farming adds upstream exposure through orchards, while Blueberries provides diversification. Multi-region sourcing, led by Mexico and Peru, supports year-round supply and strengthens customer relationships.

Mission Produce, Inc. Price, Consensus and EPS Surprise

Mission Produce, Inc. price-consensus-eps-surprise-chart | Mission Produce, Inc. Quote

Why Mission Produce Bought Calavo

The Calavo acquisition expands Mission Produce’s North American avocado scale and adds packing capacity. That matters because high-volume Mexican supply environments can stretch internal capacity and force greater reliance on third-party packing.

Calavo also broadens the product portfolio into tomatoes, papayas and prepared foods, including guacamole and salsas. This gives Mission Produce exposure beyond fresh avocados and creates a path to operational synergies. Dole plc DOLE and Del Monte Corporation FDP offer useful context as broader fresh produce companies with diversified platforms. Mission Produce remains more avocado-centered, making Calavo’s prepared foods exposure strategically meaningful.

Where AVO Still Faces Margin Pressure

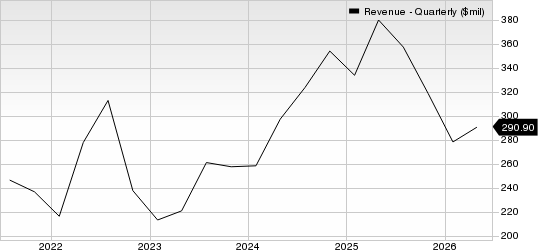

Second-quarter fiscal 2026 revenue fell 24% year over year to $290.9 million even though avocado volumes rose 15%. The offset was a 36% decline in per-unit avocado sales prices, driven by abundant Mexican supply.

Mission Produce, Inc. Revenue (Quarterly)

Mission Produce, Inc. revenue-quarterly | Mission Produce, Inc. Quote

Margins also faced a temporary mismatch between supply and demand for core fruit sizes. Mission Produce had to pay higher spot-market prices for high-demand sizes while discounting lower-demand sizes. Adjusted EBITDA fell to $7.1 million from $19.1 million a year earlier, showing how fast earnings can swing when oversupply meets weaker pricing.

How Mission Produce Plans to Recover

Management expects supply conditions, pricing and sizing curves to normalize through the back half of fiscal 2026. The company also expects its multi-region sourcing network to become more useful as supply shifts from Mexico toward California and Peru.

Mission Produce expects exportable avocado production from owned Peru farms to reach 120-130 million pounds in fiscal 2026, up from 105 million pounds in the 2025 harvest season. Consolidated second-half adjusted EBITDA is expected in the range of $84-$88 million, supported by better avocado margins, higher blueberry yields, a full fiscal fourth-quarter Calavo contribution and early synergy benefits.

What AVO’s Ratings Say About the Setup

The bottom line is that Mission Produce has a larger platform and clear category advantages, but the stock still needs evidence of steadier earnings execution. Scale, sourcing reach and prepared foods exposure improve the long-term setup. Pricing volatility, integration work and seasonal cash flow remain near-term checks on the story.

AVO currently carries a Zacks Rank #3 (Hold). It has a Value Score of B, Growth Score of C, Momentum Score of F and VGM Score of C. The Value Score points to a relatively better valuation profile, while the Growth and VGM Scores suggest a more balanced setup. The Momentum Score of F signals weak near-term price momentum.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That combination fits a measured view of the stock. Mission Produce’s strategic position has improved, but the Rank and Style Scores do not point to an aggressive near-term stance. Investors may want to see Calavo synergies, Peru volumes and per-unit margins translate into more consistent earnings before treating the stock as more than a wait-and-watch idea.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mission Produce, Inc. (AVO): Free Stock Analysis Report

Dole PLC (DOLE): Free Stock Analysis Report

Del Monte Corporation (FDP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).