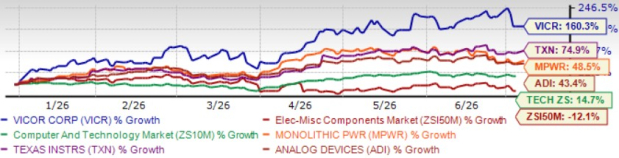

Vicor Corporation VICR shares have surged 160.3% year to date, outperforming the Zacks Electronic Miscellaneous Components industry's return of 74.9% and the broader Computer and Technology sector's appreciation of 14.7%. The rally has outpaced peers, such as Monolithic Power Systems MPWR, Analog Devices ADI and Texas Instruments TXN, shares of which have returned 48.5%, 43.4% and 74.9%, respectively, over the same period.

VICR shares are benefiting from a positive outlook as the company expects second-quarter revenues of $142 million, raised from a prior estimate of $126 million, on the back of rising product revenues and an additional licensee to its patented power system technology. Strong bookings across high-performance computing, industrial and aerospace and defense markets have driven backlog sharply higher, reinforcing confidence in the growth trajectory. Let us find out whether investors should buy VICR stock right now.

VICR Price Performance

Image Source: Zacks Investment Research

VICR Benefits From the AI Power Delivery Ramp

VICR designs and manufactures modular power components and complete power systems, with vertical power delivery increasingly central to its growth. Vicor's lead high-performance computing customer is in the midst of a steep production ramp for its wafer-scale engine, and a generational transition is expected in the second half of 2026. The company's second-generation Vertical Power Delivery (VPD) solution combines a thin package format with high current density and current multiplication, attributes that competing approaches have struggled to match.

Chipmakers and hyperscalers are pushing toward wafer-scale and multi-die chiplet packaging, increasing the need for pure vertical power delivery at the point of load. VICR's positioning at the center of this shift, combined with capacity earmarked for existing strategic customers, supports continued above-industry growth as engagement with additional high-performance computing customers follows the lead customer's generational transition.

VICR Ramps Up Capacity and Licensing to Expand Share

VICR is strengthening its position through capacity expansion and a significant licensing program. The company has identified opportunities to raise capacity at its Andover facility toward a $1.5 billion annual revenue run rate, up from a prior $1 billion target, aided by reduced cycle times and the ability to redeploy certain process steps to a nearby facility as a bridge to a second fab. This contrasts with the more measured capacity additions typical of Texas Instruments, whose scale is already largely built out.

VICR's licensing business is also emerging as a durable growth driver. The company has signed an all-inclusive licensing agreement with an additional original equipment manufacturer covering its full patent portfolio, including Factorized Power and Vertical Power Delivery architectures. Licensing carries near-full-margin economics, and management continues to expect licensing income could eventually reach as much as 50% of product revenues, a structural advantage that Analog Devices does not share to the same degree.

VICR's broad industrial base is also a source of strength, particularly among semiconductor test equipment customers, while aerospace and defense spending are rising amid geopolitical developments and higher defense budgets. These end markets diversify VICR's revenue base beyond any single compute customer, distinguishing it from Monolithic Power Systems, whose exposure remains concentrated primarily in AI server and data center applications.

The Zacks Consensus Estimate for 2026 EPS is pegged at $2.94 per share, up by 23 cents over the past 30 days, indicating year-over-year growth of 12.64%.

Vicor Corporation Price and Consensus

Vicor Corporation price-consensus-chart | Vicor Corporation Quote

VICR's Valuation is Backed by Fundamentals

VICR currently trades at a forward 12-month price-to-sales multiple of 16.26X, well above the industry average of 4.08X and the broader sector average of 6.88X. The premium also exceeds peers Texas Instruments and Analog Devices, which trade at 12.66X and 11.96X, respectively, though it is roughly in line with Monolithic Power Systems at 16.16X.

The premium looks justified given VICR's differentiated position in VPD, its expanding high-margin licensing business and a current backlog of $300.6 million that provides revenue visibility well beyond the current quarter. Gross margin reached 55.2% in the first quarter of fiscal 2026, up 800 basis points year over year, underscoring the strength of VICR's growth trajectory relative to more diversified analog peers.

VICR's P/S F12M Ratio

Image Source: Zacks Investment Research

Conclusion

Despite VICR's remarkable rally year to date, its long-term growth story remains intact. Rising demand for vertical power delivery across AI compute, along with steady strength in industrial and aerospace and defense markets, continues to support favorable demand conditions. Capacity expansion and an expanding licensing program position it for continued above-industry growth as second-generation VPD adoption broadens beyond its lead customer. With backlog building and margins expanding, VICR's premium valuation appears reasonably supported, making the stock a compelling buy for investors seeking exposure to the AI power delivery supply chain.

Vicor carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vicor Corporation (VICR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).