Monolithic Power Systems Inc. MPWR shares have risen 40.4% in the past six months compared with the industry’s growth of 31.9%. The stock has outperformed the Zacks Computer & Technology sector and the S&P 500 during the same time frame.

Image Source: Zacks Investment Research

The company has outperformed its peers like Analog Devices, Inc. ADI and Microchip Technology MCHP. Shares of Analog Devices have jumped 30%, and shares of Microchip have risen 19.1%.

MPWR Benefits From Strong Demand Across Multiple Verticals

Monolithic is witnessing solid traction across multiple end markets. Strong demand for AI accelerators, CPUs and server power management solutions is driving demand in the Enterprise Data segment. The company’s robust capability in high-power-density solutions, monolithic integration and advanced module designs is boosting its competitive edge in the AI infrastructure vertical. MPS differentiates itself by offering single-piece silicon-based power solutions, unlike competitors that rely on multiple silicon components. This facilitates greater efficiency, compact designs and better thermal performance. These factors are becoming critical in next-generation AI servers and GPUs that are moving toward higher power requirements.

Strong demand for optical modules and Ethernet switches used in AI data centers is propelling growth in the Communications segment. Automotive remains a long-term growth driver as semiconductor content rises across ADAS, infotainment and connectivity applications. Management indicated that the pipeline across Automotive and Enterprise Data continues to expand through new project wins across regions and customers.

Robotics and physical AI are an emerging long-term growth driver. AI adoption in robotics has already started to create commercial opportunities. Recognizing this trend, Monolithic is broadening its exposure to robotics, building automation and portable AI devices. sampled its first DDR5 high-speed interface products, expanding beyond power management into higher-value semiconductor content. The company’s growing emphasis on innovation, diversifying its portfolio offering to different emerging opportunities, bodes well for sustainable growth.

It is to be noted that MPWR is steadily increasing its manufacturing capacity. It has raised its manufacturing capacity target from $4 billion to $6 billion to support the growing demand. It is also actively diversifying its production geographically. This will boost supply chain resilience and allow the company to capture opportunities in unexplored markets.

Major Challenges

MPWR continues to face weakness in the consumer notebook market. Memory shortages, higher memory prices and weaker consumer demand will likely continue to impact demand in the near term.

The company is venturing into several new growth areas to diversify its revenue stream. It is investing in DDR5 interfaces, robotics, 800V power architectures and silicon carbide technologies. Despite the significant upside in these markets in the long term, commercial deployments are still in early stages. The timing of revenue generation from these verticals remains uncertain.

Monolithic operates in a highly competitive analog semiconductor market populated by larger companies with broader product portfolios and deeper financial resources. It faces intense competition across analog and power management semiconductors from larger peers, such as Analog Devices, Microchip, Texas Instruments and others. The company must continue investing heavily in research and development, manufacturing capacity and new technologies to maintain its competitive position. Any slowdown in product innovation or execution could affect future socket wins and profitability.

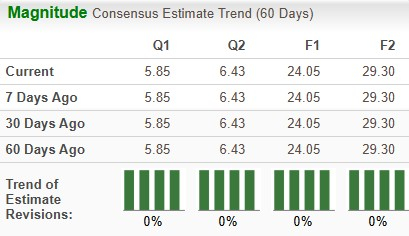

Estimate Revision Trend

Earnings estimates for MPWR for 2026 and 2027 have remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

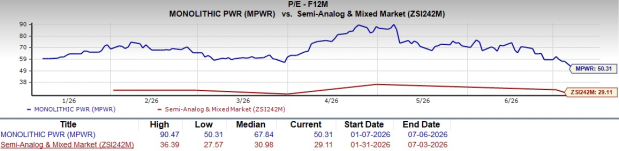

Key Valuation Metric of MPWR

From a valuation standpoint, MPWR is currently trading at a premium compared to the industry. Going by the price/earnings ratio, the company’s shares currently trade at 50.31 forward 12-month earnings, higher than 29.11 for the industry.

Image Source: Zacks Investment Research

End Note

Solid momentum across multiple verticals, such as AI servers and optical networking, is a major growth catalyst. Design wins across the automotive and enterprise markets are a positive. Focus on manufacturing capacity expansion and supply chain diversification will likely bring long-term benefits. Portfolio expansion beyond core power management markets is a tailwind. However, demand softness in the consumer notebook market due to memory shortages and rising prices remains a concern. Geopolitical volatility and macro headwinds can impact its supply chain operations and hinder customer spending. Competition from other major players in the industry is weighing on margins. With a Zacks Rank #3 (Hold), MPWR appears to be treading in the middle of the road, and new investors could be better off if they trade with caution. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Microchip Technology Incorporated (MCHP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).