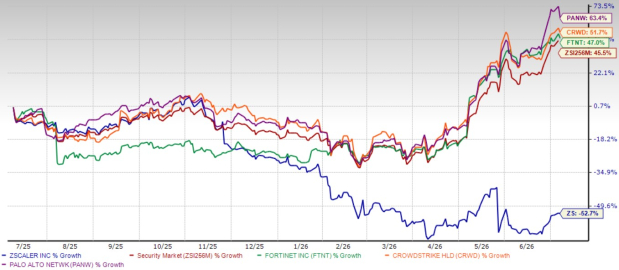

Zscaler, Inc. ZS stock has been one of the biggest disappointments in the cybersecurity space over the past year. The stock has plunged 52.7%, while the broader Zacks Security industry has gained 45.5%.

That gap becomes even more striking when compared with peers. Fortinet, Inc. FTNT, CrowdStrike Holdings, Inc. CRWD and Palo Alto Networks, Inc. PANW have delivered strong gains over the same period. Over the past year, shares of Fortinet, CrowdStrike Holdings and Palo Alto Networks have rallied 47%, 51.7% and 63.4%, respectively.

A decline of this size naturally raises an important question: Is Zscaler losing its edge, or has the market become too pessimistic?

Zscaler One-Year Price Return Performance

Image Source: Zacks Investment Research

Why Investors Have Turned Cautious About ZS Stock

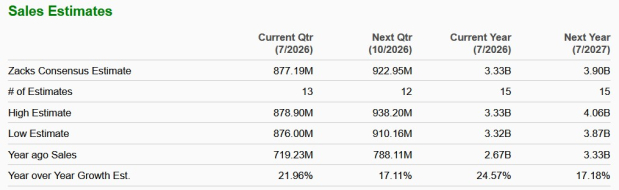

The biggest concern is not that Zscaler is shrinking. The company is no longer growing at the pace investors had become accustomed to. For years, Zscaler consistently delivered revenue growth above 40%. Today, that growth has settled into the mid-20% range, and management expects another slowdown in fiscal 2027. The company projects revenue growth of roughly 16% and annual recurring revenue (ARR) growth of about 17% in fiscal 2027.

That marks a meaningful slowdown from recent years. Management attributes the softer outlook to several factors, including changes in sales leadership, more conservative assumptions for acquiring new customers and a slower-than-expected contribution from the Red Canary acquisition.

Image Source: Zacks Investment Research

Another issue weighing on sentiment is higher spending. Artificial intelligence (AI) is creating new cybersecurity opportunities, but it is also making infrastructure more expensive. Memory, processors, storage and networking equipment are becoming costlier, forcing Zscaler to increase capital spending.

Management expects capital expenditures to reach the high single digits as a percentage of revenues in fiscal 2026 compared with its earlier expectation of the mid-single digits. It also expects fiscal 2027 capital expenditures as a percentage of revenues to rise by as much as 200 basis points from the 2026 level because of higher hardware costs.

Macroeconomic uncertainty, tariffs and geopolitical risks have only added to investor caution. Taken together, these issues have kept the stock highly volatile over the past year. However, these negative factors do not necessarily suggest that Zscaler’s business itself is weakening.

Zscaler’s Business Is Still Delivering

Despite the sharp decline in the share price, Zscaler continues to post strong operating results. In the third quarter of fiscal 2026, revenues increased 25% year over year to $850 million. ARR also grew 25% to $3.53 billion, while remaining performance obligations climbed about 30% to $6.5 billion.

Customer engagement remains healthy as well. The company now has 748 customers generating more than $1 million in ARR and more than 4,000 customers contributing above $100,000 annually.

Profitability is moving in the right direction, too. Non-GAAP gross margin expanded 40 basis points to 80.7%, operating margin improved 140 basis points to 23%, and adjusted earnings per share jumped nearly 29% year over year to $1.08. Free cash flow remains impressive, with a margin of 29% year to date. Management also highlighted that it continues to meet the "Rule of 55," balancing healthy growth with strong cash generation.

These numbers suggest that Zscaler's business is not facing a demand collapse. Instead, investors are reacting to a moderation in growth expectations after years of exceptionally rapid expansion.

AI Security Could Be the Next Growth Engine for ZS

The long-term opportunity may be larger than the current market reaction suggests.

As enterprises deploy AI applications and autonomous AI agents, securing those systems is becoming increasingly important. That plays directly into Zscaler's Zero Trust platform, which is designed to prevent unauthorized access and limit the movement of attackers across corporate networks.

Early signs are encouraging. Bookings for AI Protect have exceeded $100 million over the past year, showing that customers are already investing in AI-specific security solutions.

The company is also expanding its AI ecosystem through partnerships with OpenAI and Anthropic, while the planned acquisition of Symmetry Systems should strengthen its ability to protect enterprise data and AI workloads.

Enterprise AI adoption is still in its early stages. If that trend accelerates over the next several years, Zscaler could be well-positioned to benefit.

Zscaler’s Platform Expansion Is Becoming an Advantage

Another upside is that Zscaler is selling more products to existing customers instead of relying solely on new customer wins.

Its Data Security business has surpassed $500 million in ARR and continues to grow more than 30% annually. Zero Trust Branch ARR has nearly tripled over the past year, reflecting broader adoption of the company's platform.

Perhaps the strongest indicator is the rapid growth in "Zero Trust Everywhere" customers —organizations using Zscaler across users, cloud workloads and branch environments. Their number increased from more than 550 in the second quarter to above 700 in the third quarter.

The company's Z-Flex program is also gaining traction by encouraging larger, multi-year customer commitments. During the third quarter, Z-Flex generated more than $480 million in contract value, up more than 60% sequentially. Over the past year, it has produced more than $1 billion in total contract value.

These metrics suggest customers are expanding their relationships with Zscaler rather than reducing spending.

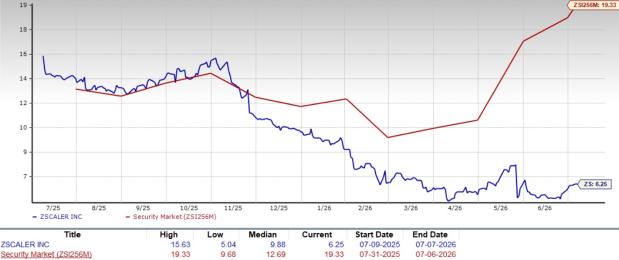

ZS Stock’s Valuation Finally Looks Reasonable

After losing more than half its value, Zscaler is no longer priced like a high-flying growth stock. Its shares currently trade at a forward price-to-sales ratio of 6.25, well below the security software industry average of 19.33.

Zscaler Forward 12-Month Price-To-Sales Ratio

Image Source: Zacks Investment Research

The discount is even more noticeable when compared with peers, such as Fortinet, Palo Alto Networks and CrowdStrike. Fortinet trades at 14.16 times forward sales, Palo Alto Networks at 20.25 times and CrowdStrike at 30.52 times.

Some of that valuation gap is justified because Zscaler's growth is slowing. Considering that the company is still growing revenues around 25%, expanding margins, generating strong free cash flow and building new AI-driven businesses, the discount appears larger than fundamentals alone would suggest.

Final Thoughts: Hold Zscaler Stock for Now

The market has clearly shifted its view of Zscaler. Investors are no longer willing to pay premium valuations for slowing growth, even if the business remains fundamentally healthy. That does not mean the investment case is broken.

Fiscal 2027 is likely to bring slower revenue growth and higher infrastructure spending. Those headwinds could keep the stock volatile over the near term.

However, the bigger picture remains intact. Zscaler continues to lead in Zero Trust security, customer adoption is expanding, profitability is improving, and AI security is opening another potential growth avenue.

For investors with a long-term horizon, this looks more like a period of resetting expectations than a deterioration in the underlying business. The stock may not rebound overnight, but its combination of solid execution, expanding platform adoption and a much more reasonable valuation supports a hold stance rather than an exit.

Zscaler currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zscaler, Inc. (ZS): Free Stock Analysis Report

Fortinet, Inc. (FTNT): Free Stock Analysis Report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).