The global semiconductor foundry market is attracting growing investor interest, driven by advancements in artificial intelligence (AI), machine learning, 5G and the Internet of Things (IoT). Foundries continue to heavily invest in research and development to offer advanced process nodes, helping meet demand for these high-tech applications. According to Fortune Business Insights, the market is projected to witness a CAGR of 3.4% through 2026-2034, expanding from $175.1 billion in 2025. Taiwan Semiconductor Manufacturing Company TSM, or TSMC, dominates this space with more than 70% market share.

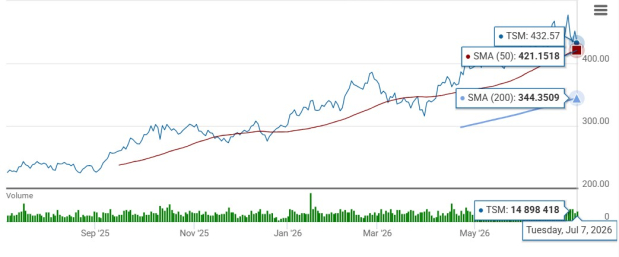

Over the past year, the stock has surged 90.4%, outperforming the Zacks Computer and Technology sector’s 37.2% gain and the S&P 500 composite’s 24.9% return. TSMC also outpaced peers GlobalFoundries GFS and ON Semiconductor ON, or onsemi, both of which gained 58.9% over the same period.

TSM Stock’s 12-month Performance

Image Source: Zacks Investment Research

Based on its last closing price, TSM stock is trading above its 50-day and 200-day simple moving averages (SMAs), signaling sustained bullish momentum.

TSM Technical Indicator

Image Source: Zacks Investment Research

Tailwinds Supporting TSMC

TSMC reported May 2026 consolidated net revenues of NT$416.98 billion (New Taiwan Dollars), up 1.5% from April 2026 and 30.1% from May 2025. For the first five months of 2026, consolidated revenues totaled NT$1.96 trillion, marking a 30% increase compared with the same period last year.

Robust AI-related demand underpins the company’s growth outlook. Management stated that the shift from generative AI and the query mode to agentic AI and command and action mode is driving higher token consumption and increasing the need for computation, supporting demand for leading-edge silicon. TSMC continues to see a strong signal and positive outlook from its customers as well as cloud service providers, maintaining a high level of conviction in the multiyear AI megatrend.

Performance-wise, first-quarter 2026 revenues increased 6.4% sequentially to $35.9 billion, slightly ahead of the company’s guidance. Gross margin expanded by 390 basis points (bps) sequentially to 66.2%, driven by cost improvement efforts, a higher overall capacity utilization rate and a more favorable foreign exchange rate. Operating margin improved 410 bps sequentially to 58.1% due to operating leverage.

TSMC’s 2-nanometer (N2) and A16 technologies continue to lead the industry in addressing the demand for energy-efficient computing, with almost all the innovators working with TSMC. N2 is ramping up successfully in multiple phases at both the company’s Hsinchu and Kaohsiung sites, led by strong demand from both smartphone and High-Performance Computing (“HPC”) AI applications.

At the same time, the company is stepping up its capital expenditure to expand its global 3-nanometer capacity. The expansion spans Taiwan, Arizona and Japan, alongside 5-nanometer tool conversions and capacity optimization across N7, N5 and N3 nodes. TSMC’s A14 technology development is also on track, for which it is seeing a high level of customer interest and engagement from both smartphone and HPC applications.

TSMC’s Near-Term Financial Outlook

TSMC remains confident that full-year 2026 revenues will grow by more than 30% in U.S. dollar terms, reflecting the strength of its differentiated technology and broad customer base.

For the second quarter, the company expects revenues between $39 billion and $40.2 billion, representing 10% sequential growth and 32% year-over-year growth at the midpoint. Based on an exchange rate assumption of $1 to 31.7 New Taiwan Dollars, the second-quarter gross margin is projected at 65.5%-67.5% and operating margin at 56.5%-58.5%. Management noted that the initial ramp-up of its 2-nanometer technology will dilute gross margin by 2%-3% for the year.

TSMC also expects capital expenditures to trend toward the high end of its previously announced $52-$56 billion range as it expands capacity to support customer demand. Despite the elevated spending, management reiterated its focus on delivering profitable growth for shareholders.

TSM Stock’s Estimate Trend

At present, the Zacks Consensus Estimate expects TSMC’s earnings per share (EPS) to grow 44.1% to $15.35 in 2026, followed by another 27% increase to $19.50 in 2027. Analyst estimates for both years have moved higher over the past three months. The company’s revenues are expected to grow 32.3% in 2026 and another 26.6% in 2027.

Image Source: Zacks Investment Research

How Valuation Metrics Look for TSMC

Based on the forward 12-month Price/Earnings (P/E), TSM trades at 25.84X, slightly above its median of 24.33X and the 24.98X sector average. In contrast, GFS trades at a P/E of 38.63X, while ON sits with 24.35X.

TSM’s One-Year P/E

Image Source: Zacks Investment Research

Conclusion

TSMC benefits from strong demand for its leading-edge process technologies. The performance of its key profitability metrics is supported by cost improvement efforts and a high-capacity utilization rate. The higher level of capital spending reflects management’s confidence in delivering profitable growth to shareholders and also capturing long-term growth opportunities. At the same time, TSMC remains well-positioned to continue capitalizing on the strong industry tailwinds.

The stock has significantly outperformed the sector and other peers over the past 12 months. From a valuation standpoint, TSM is trading close to both its historical median and sector average. Backed by positive earnings estimate revisions, the stock appears to be an attractive investment opportunity.

TSM carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Taiwan Semiconductor Manufacturing Company Ltd. (TSM): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

GlobalFoundries Inc. (GFS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).