Uranium Energy Corp. UEC offers a split case for investors. It has no debt, nearly $794 million in liquid assets, growing U.S. in-situ recovery production capacity and physical uranium inventory.

The offset is harder to ignore. Losses widened in the latest quarter, sales timing remains inconsistent and the stock still carries a premium valuation despite recent estimate cuts.

Why UEC Bulls Point to Balance Sheet Strength

UEC ended the third quarter of fiscal 2026 with $794 million of liquid assets, including $488 million of cash. That balance sheet gives the company room to keep building wellfields, advance development assets and fund fuel-cycle initiatives without leaning on debt.

The company also held 1.456 million pounds of purchased uranium inventory, with an indicated market value of about $127 million. Management made no sales in the quarter, preserving inventory so it can execute sales when pricing is attractive.

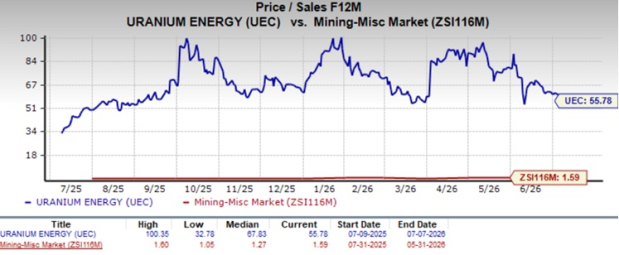

Why Uranium Energy Still Looks Expensive

The valuation case is less forgiving. UEC trades at 55.78X forward 12-month sales compared with 1.59X for the Zacks sub-industry, 2.66X for the broader sector and 5.07X for the S&P 500.

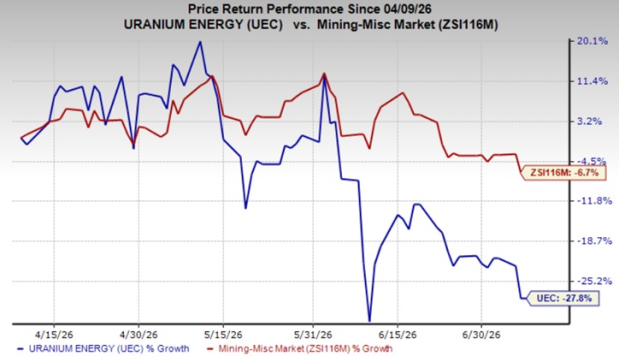

The $11 price target also leaves a narrower near-term case with the stock at $9.90 as of July 7, 2026. Operational progress still matters, but investors are being asked to pay a premium while production, costs and sales remain uneven. Also. shares of UEC have declined 27.8% in the past three months against the industry’s 6.7% fall.

Cameco Corporation CCJ is a larger uranium peer in the same industry comparison set, which gives investors another way to assess uranium exposure. Energy Fuels Inc. UUUU also sits in the peer group, making it a relevant comparison for investors weighing U.S.-linked uranium themes.

UEC Earnings Trend Still Sends a Cautious Signal

UEC reported an adjusted loss of seven cents per share in the third quarter of fiscal 2026. That was wider than the Zacks Consensus Estimate of a loss of five cents and worse than the year-ago loss of six cents.

The company reported no sales in the quarter. Total operating costs rose 73.8% year over year to $40.8 million, while the current fiscal-year earnings estimate fell 30.4% over the past four weeks, showing that the market is still absorbing the cost of the ramp.

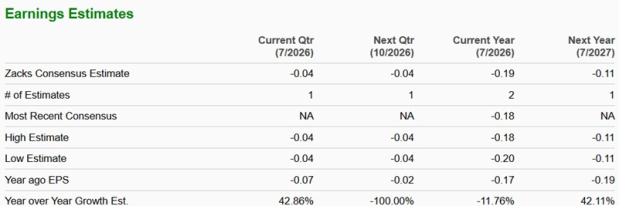

The Zacks Consensus Estimate for UEC for fiscal 2026 is currently pegged at a loss of 19 cents per share, wider than the loss of 17 cents reported in fiscal 2025. The consensus for fiscal 2027 also suggests a loss of 11 cents per share, as shown in the chart below.

Image Source: Zacks Investment Research

What Could Change the UEC Investment Case

A more compelling setup would require steadier production from Christensen Ranch and Burke Hollow. At Christensen Ranch, three new header houses began production late in the third quarter after state approval, while one more was complete and awaiting approval.

Burke Hollow started production on April 8, 2026, and is expected to contribute for a full fourth fiscal quarter. Investors should watch whether higher volumes lower unit costs, whether approvals arrive on schedule and whether preserved inventory begins turning into revenues.

How UEC’s Signals Support a Wait-and-See View

The bottom line is that UEC has strategic assets and meaningful liquidity, but the stock has not yet shown a clean earnings or sales pattern. Its operating base is expanding, yet unit costs, approval timing and unhedged sales decisions can still make quarterly results choppy.

The stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Its Style Scores are also weak, with a VGM Score of F, Value Score of F, Growth Score of F and Momentum Score of D.

Zacks Style Scores are designed to complement the Zacks Rank by evaluating value, growth and momentum traits. For UEC, the weak scores and unfavorable Rank support a wait-and-see posture rather than a clear buy-now case.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Uranium Energy Corp. (UEC): Free Stock Analysis Report

Cameco Corporation (CCJ): Free Stock Analysis Report

Energy Fuels Inc (UUUU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).