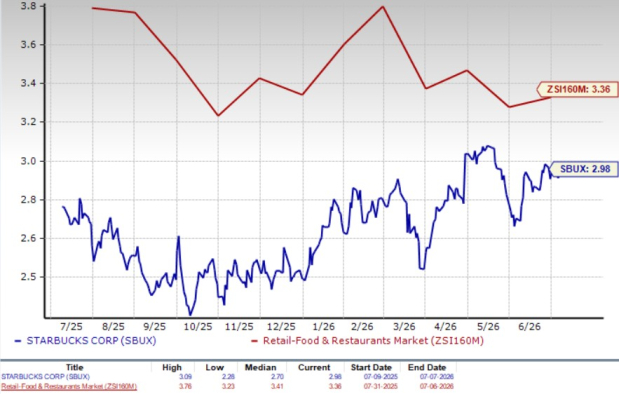

Starbucks Corporation’s SBUX shares have rallied 23.1% year to date, significantly outperforming the industry’s 1.9% growth. The strong momentum has pushed the stock close to its 52-week high of $108.88. Yesterday, Starbucks closed at $103.61, just 4.8% below that peak, reflecting growing investor confidence in its turnaround strategy.

Starbucks' recent rally reflects growing confidence in its turnaround strategy. The company posted its first year-over-year revenue and earnings growth in more than two years, raised the fiscal 2026 outlook and benefited from strong comparable sales, improving customer traffic, successful menu innovation and a stronger Starbucks Rewards program, reinforcing investor optimism.

Even among the top industry players, SBUX stands tall, outperforming McDonald's Corporation MCD, Chipotle Mexican Grill, Inc. CMG and Yum! Brands, Inc. YUM.

Price Performance

Image Source: Zacks Investment Research

Turnaround Strategy Is Delivering Results

One of the biggest catalysts behind Starbucks stock rally has been its return to revenue and earnings growth. During the second quarter of fiscal 2026, Starbucks reported year-over-year growth in both metrics for the first time in more than two years. Global comparable-store sales rose 6%, driven by more than 7% comparable sales growth in North America and strong transaction gains across all dayparts. Importantly, management noted that customer traffic reached its strongest level in three years, indicating that the company's operational improvements are encouraging consumers to visit more frequently.

The turnaround has been supported by the rollout of the Green Apron Service model, which focuses on better staffing, faster service and improved customer experience. Starbucks reported rising customer satisfaction scores while maintaining service speed despite handling higher transaction volumes. The company is also introducing scheduled mobile order pickup, which should improve convenience and throughput. These initiatives are helping restore Starbucks' premium customer experience while increasing store productivity.

Innovation and Loyalty Are Driving Demand

Starbucks continues to strengthen customer engagement through product innovation and an upgraded loyalty ecosystem. New beverage launches, including premium Matcha drinks, energy refreshers and seasonal offerings, have generated strong demand and expanded afternoon sales opportunities. The company also highlighted rapid growth in its Cold Foam platform and refreshers business, which continues to attract younger consumers.

At the same time, Starbucks Rewards has become a key growth engine. Active U.S. Rewards membership reached a record 35.6 million, while the redesigned program has increased customer engagement and visit frequency. Management noted that the new 60-star redemption option has quickly become the most popular reward, supporting repeat visits and reinforcing customer loyalty. These initiatives, combined with targeted marketing, have helped improve brand affinity to its highest level in five years.

International Momentum Adds Another Growth Avenue

The recovery is no longer limited to North America. Starbucks reported positive comparable sales across all 10 of its largest international markets for the first time in nine quarters. China recorded another quarter of transaction-led growth, while Japan and South Korea delivered particularly strong performances.

The recently completed partnership with Boyu Capital also positions Starbucks China for long-term expansion while reducing capital intensity. Management expects the new licensing structure to improve profitability and support faster expansion across more than 1,500 Chinese county-level cities over the next three years. The company also reaffirmed plans to open 600-650 net new stores globally in fiscal 2026, providing another growth catalyst.

What Could Slow the Rally?

Despite the encouraging progress, several risks could temper Starbucks stock’s momentum.

Management acknowledged that the macroeconomic environment remains uncertain. Although customer demand has remained resilient, executives cautioned that higher fuel prices and broader economic pressures could eventually weigh on consumer spending. Starbucks incorporated this uncertainty into its updated fiscal 2026 guidance, suggesting management remains cautious despite recent strength.

Margin pressures have not disappeared. Product and distribution costs remain elevated due to coffee inflation, tariffs and innovation-related expenses. While Starbucks expects these headwinds to ease in the second half of fiscal 2026, any rebound in commodity prices or prolonged tariff impacts could pressure profitability.

Sustaining the rally will require continued flawless execution of the "Back to Starbucks" strategy. The company is making significant investments in labor, technology and store upgrades, and investors will expect these investments to continue generating stronger traffic, higher comparable sales and expanding margins. Any slowdown in execution or a weakening of consumer demand could reduce enthusiasm for the turnaround.

SBUX’s Estimate Revision Trend

The Zacks Consensus Estimate for SBUX's fiscal 2026 and 2027 EPS moved up in the last 60 days, indicating positive sentiment among analysts for its earnings.

Image Source: Zacks Investment Research

Taking a Look at Starbucks’ Valuation

SBUX stock is trading below the industry. With a forward 12-month price/sales ratio of 2.98X, below its industry average. Meanwhile, other industry players like McDonald's, Chipotle Mexican Grill and Yum! Brands are trading at 6.85X, 3.23X and 4.96X, respectively.

P/S (F12M)

Image Source: Zacks Investment Research

End Notes

Starbucks is making meaningful progress in its turnaround, supported by improving operations, stronger customer engagement, successful product innovation and growing momentum across international markets. These factors, along with improving earnings expectations and a reasonable valuation, support a Hold stance for existing investors. However, with the stock trading close to its 52-week high after a strong rally, much of the near-term optimism appears to be reflected in the share price.

In addition, macroeconomic uncertainty, lingering cost pressures and the need for continued flawless execution of the "Back to Starbucks" strategy could limit further upside. As a result, existing investors may consider holding the stock to benefit from the ongoing turnaround, while new investors may be better served waiting for a more attractive entry point.

Starbucks currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Starbucks Corporation (SBUX): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Yum! Brands, Inc. (YUM): Free Stock Analysis Report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).