EZCORP, Inc.'s EZPW strong operating performance has driven a sharp rally in its shares, bringing both its earnings outlook and valuation into focus. Over the past six months, EZPW shares have gained 65.8% against the industry’s 11.4% decline.

Price Performance

Image Source: Zacks Investment Research

The key question for investors now is whether the company’s improving fundamentals can continue to support further upside after much of the recent optimism has already been reflected in the stock price.

The outlook remains balanced. Strong earnings growth, rising pawn loan balances and solid liquidity support the bull case, while a higher valuation and ongoing cost pressures suggest that EZPW may no longer be an obvious bargain.

EZPW Has Built a Bullish Operating Case

EZCORP’s recent performance highlights improving operational execution. The company’s earnings topped estimates in each of the trailing four quarters, reflecting its sustained business momentum.

In the second quarter of fiscal 2026, revenues surged 46% year over year to $446.9 million, while gross profit also grew 46%. Pawn loans outstanding increased 33% to $349.4 million, driven by higher average loan sizes, sustained pawn demand and store expansion.

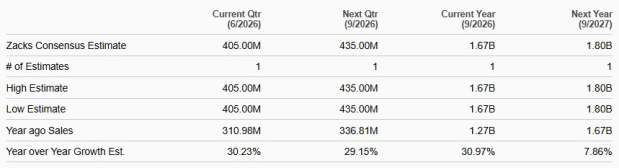

The revenue outlook further strengthens the growth narrative. The Zacks Consensus Estimate for sales is pegged at $1.67 billion for fiscal 2026 and $1.80 billion for fiscal 2027, indicating year-over-year growth of 31% and 8%, respectively.

Revenue Estimates

Image Source: Zacks Investment Research

Margins also improved year over year in the second quarter of fiscal 2026, with merchandise sales gross margin expanding to 36% from 34% and jewelry scrap sales gross margin increasing significantly to 38% from 22%.

Adding to the positive outlook, earnings estimates have remained stable. The Zacks Consensus Estimate for fiscal 2026 and 2027 earnings has been unchanged over the past 30 days, indicating year-over-year growth of 40% and 10%, respectively.

Estimates Revision Trend

Image Source: Zacks Investment Research

EZCORP Valuation Looks More Demanding

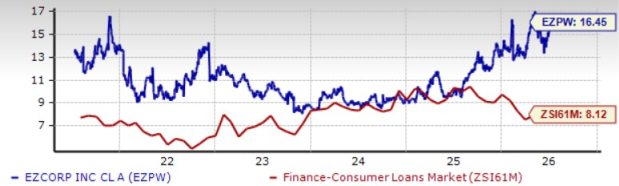

The recent rally has made EZPW's valuation look more demanding. EZPW is trading at 16.45X forward 12-month earnings, above the Zacks sub-industry average of 8.12X.

The multiple is broadly in line with the Zacks sector average of 16.59X and below the S&P 500 average of 21.24X. It also remains above the stock's five-year median of 10.67X, suggesting the shares have become more expensive relative to their historical valuation.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

Enova International, Inc. ENVA and Encore Capital Group, Inc. ECPG are part of the broader alternative finance peer group, offering investors additional names for comparison. At present, ECPG holds a forward 12-month P/E ratio of 6.71X, while ENVA's forward 12-month P/E ratio stands at 13.68X.

EZPW Liquidity Supports the Investment Story

EZCORP’s strong liquidity position continues to support its investment case. As of March 31, 2026, cash and cash equivalents totaled $354.2 million, providing the company with the flexibility to integrate acquisitions, expand its store network and pursue future growth opportunities.

The company’s pawn loans of $349.4 million and long-term debt of $519 million reflect continued investment in its core lending business while maintaining a balanced approach toward funding growth. Additionally, a current ratio of 4.71 highlights EZCORP’s strong short-term liquidity and ability to comfortably meet its near-term obligations.

With a healthy liquidity position, EZCORP remains well-positioned to execute its expansion strategy, including store openings and acquisitions such as Simple Management Group, while maintaining disciplined capital allocation.

EZCORP Risks Limit a Clear-Cut Buy Case

The key risk factor remains elevated costs. In the second quarter of fiscal 2026, store expenses increased 33%, while general and administrative expenses rose 37%. Higher labor costs, incentive compensation and Simple Management Group-related expenses were the primary drivers. If these cost pressures persist, they could make future earnings growth more difficult to achieve.

EZCORP’s revenue mix also creates sensitivity to changing market conditions. Merchandise sales accounted for 47.9% of revenues as of March 31, 2026, making weaker retail demand a potential risk to sales performance.

Gold prices represent another variable for the company. Jewelry scrapping activities contributed 18.2% of revenues in the second quarter of fiscal 2026, and recent scrap profitability benefited from favorable gold prices. Any normalization in gold-driven scrap profits could introduce volatility into future results.

How EZPW’s Ratings Shape the Stock Outlook

The bottom line is that EZPW continues to offer attractive growth prospects, but the recent rally has reduced the margin of safety for investors. While strong execution and an improving earnings outlook support the investment case, elevated valuation and expense pressures warrant a more cautious approach.

EZPW currently carries a Zacks Rank #3 (Hold). That supports a hold-or-watch stance rather than an aggressive buy call, especially with the shares already rerated. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are more constructive. EZPW has a Value Score of B, a Growth Score of B and a VGM Score of B, suggesting solid core characteristics across valuation and growth measures.

The weaker Momentum Score of D keeps the signal mixed. For investors, the stock looks worth monitoring, but new money may need a more favorable entry point or more proof that earnings growth can keep outpacing rising costs.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EZCORP, Inc. (EZPW): Free Stock Analysis Report

Encore Capital Group Inc (ECPG): Free Stock Analysis Report

Enova International, Inc. (ENVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).