Zeta Global Holdings Corp. ZETA gives investors a difficult setup. The business is growing quickly, AI adoption is building and management has continued to raise its outlook.

The stock case is less straightforward. Estimate pressure, margin timing and a sharp share-price recovery leave investors weighing operating momentum against a weaker near-term setup.

Why ZETA Bulls See More Upside

The bullish argument starts with execution. The first quarter of 2026 marked Zeta’s 19th consecutive beat-and-raise quarter, with management lifting 2026 guidance for revenues, adjusted EBITDA and free cash flow.

Visibility also improved. Remaining performance obligations increased $66 million sequentially from the fourth quarter of 2025 to the first quarter of 2026, helped by enterprise and agency wins with long-term commitments.

Management reiterated expectations for positive GAAP net income in 2026 and said earnings per share were pacing toward the high end of the 2-4 cents range. First-quarter revenues rose 50% year over year to $396.3 million, and the sales pipeline expanded roughly 40%.

Where Zeta’s Stock Case Gets Harder

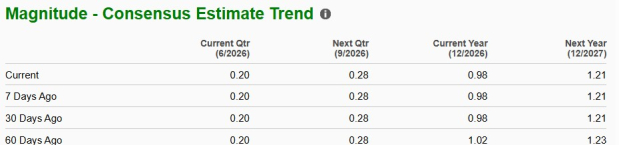

The caution starts with estimates. The 2026 earnings-per-share consensus has been trimmed to 98 cents from $1.02 over the past 60 days, with two downward revisions in the last four weeks.

Shares have already gained 39.5% in the past three months and 40% over the past year. That recovery can make the stock more sensitive to even modest revisions if investors question the timing of margin expansion or AI monetization.

The debate is not unique to Zeta. The Trade Desk TTD, an advertising technology platform for advertisers, offers another way to gauge demand for data-driven marketing workflows. LiveRamp Holdings RAMP, which focuses on data collaboration for marketing, is relevant as enterprises evaluate identity, measurement and interoperability tools.

How ZETA Valuation Looks Today

ZETA trades at 19.93X forward 12-month earnings, below the Zacks sub-industry average of 21.79X and the S&P 500’s 21.14X multiple. It is slightly above the Zacks sector average of 17.64X.

That valuation does not settle the buy question. The discount to the sub-industry may cushion some execution risk, but the premium to the sector means investors still need confidence that growth can convert into durable earnings expansion.

The current $23 price target is based on 19X trailing 12-month earnings. With the stock recently at $21.87, the target suggests limited near-term upside unless estimates stabilize or investors assign a higher multiple to Zeta’s AI-enabled platform strategy.

What Could Change the Zeta Debate?

Athena is a key swing factor. The product reached general availability for all enterprise customers in the first quarter of 2026, and agentic interactions increased more than sevenfold in the first week.

Guidance assumes minimal Athena revenue contribution in 2026, which leaves room for upside if usage converts into monetization faster than modeled. Better-than-expected Marigold cross-sell could also support operating leverage if integration synergies build as expected.

The risks remain clear. Agency-led social ramps lifted GAAP cost of revenue to 41% in the first quarter and contributed to an adjusted EBITDA margin of 16.7%, down 100 basis points year over year. Discretionary spending exposure, longer agency payment cycles and delayed synergy capture could keep the stock in wait-and-see mode.

How ZETA Signals Shape the Call

The bottom line is mixed. Zeta’s operating story has real momentum, but the stock does not offer a clean buy signal while estimate pressure and margin execution remain active concerns.

ZETA currently carries a Zacks Rank #4 (Sell), which points to unfavorable earnings estimate revision trends over the next one to three months. That argues for caution, even with strong revenue growth and repeated guidance raises.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are more balanced. ZETA has a Growth Score of A and a VGM Score of B, showing attractive growth characteristics and a solid combined profile. Its Momentum Score of F and Value Score of D are weaker, reinforcing that investors may need more evidence of estimate stability before treating the stock’s growth story as enough to offset near-term risk.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Zeta Global Holdings Corp. (ZETA): Free Stock Analysis Report

The Trade Desk (TTD): Free Stock Analysis Report

LiveRamp Holdings, Inc. (RAMP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).