Levi Strauss & Co. LEVI reported strong second-quarter fiscal 2026 results, with earnings and revenues surpassing the Zacks Consensus Estimate. The denim apparel maker continued to benefit from healthy consumer demand, robust Direct-to-Consumer (DTC) momentum, broad-based international growth and improving profitability. Management raised its fiscal 2026 revenue and earnings outlook.

The global denim leader reported adjusted earnings of 28 cents per share, which beat the Zacks Consensus Estimate of 24 cents by 16.7%. The bottom line also increased 27.3% from the 22 cents reported in the year-ago quarter.

Quarterly net revenues increased 8% year over year to $1.56 billion, surpassing the Zacks Consensus Estimate of $1.52 billion by 2.5%. Organic revenues advanced 5.7%, reflecting balanced growth across regions, channels and product categories.

Despite the earnings beat and higher full-year guidance, LEVI shares declined 5.5% following the earnings release. While management reaffirmed confidence in the business and highlighted broad-based growth, the company also noted that tariff and foreign exchange pressures remained headwinds and were embedded in its updated fiscal 2026 outlook.

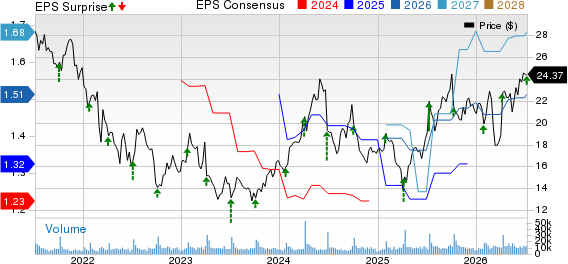

Levi Strauss & Co. Price, Consensus and EPS Surprise

Levi Strauss & Co. price-consensus-eps-surprise-chart | Levi Strauss & Co. Quote

LEVI's Quarterly Performance: Key Metrics & Insights

Levi Strauss' DTC business remained the primary growth engine during the quarter. DTC revenues increased 10.8% on a reported basis and 8.4% organically, benefiting from higher store productivity and strong digital momentum. E-commerce revenues climbed 19% on a reported basis and 17% organically, while DTC comparable sales advanced 6%. The DTC channel accounted for 51% of total company revenues during the second quarter.

Wholesale revenues grew 5.3% on a reported basis and 3.1% organically, reflecting healthy demand across retail partners. Beyond Yoga also performed strongly, with revenues increasing 15.8% year over year.

The Zacks Consensus Estimate for the DTC and wholesale channels was pegged at $805 million and $734 million, respectively, for the fiscal second quarter.

Management emphasized that the company's balanced growth strategy continued to generate momentum across wholesale and DTC, U.S. and international markets, women's and men's businesses, as well as tops and bottoms. Categories beyond denim bottoms contributed roughly one-third of quarterly revenue growth, highlighting Levi Strauss' transformation into a broader denim lifestyle company.

LEVI’s Regional Performance Stays Broad

The Americas generated revenues of $815.5 million, increasing 9% on a reported basis and 6.8% organically. Within the region, the U.S. business grew 5%, supported by continued strength across both DTC and wholesale channels.

Europe reported revenues of $420.2 million, up 4.2% on a reported basis but down 0.8% organically due to the timing impact of last year's distribution center transition. Excluding this temporary disruption, underlying demand remained healthy, supported by strong DTC performance across key markets.

Asia continued to outperform, with revenues increasing 10.1% on a reported basis and 11.9% organically to $283.7 million, reflecting double-digit growth across both DTC and wholesale channels. Management also highlighted strong performances across Turkey, Japan and India, while noting early signs of improvement in China. Mexico remained another standout market with 15% growth and Latin America also delivered double-digit gains across Brazil, Colombia and the Andes region.

Levi Strauss’ Brand & Category Momentum

The Levi's brand generated $1.46 billion in revenues during the quarter, increasing 8.1% on a reported basis and 5.6% organically. Total Levi's Brands revenues rose 7.8% on a reported basis and 5.5% organically, while Levi Strauss Signature posted modest growth.

Women's revenues advanced 11%, supported by continued demand across seasonal assortments and an expanding lifestyle offering. Bottoms revenues increased 6%, driven by core fits and looser silhouettes, while shorts grew 11%. Tops revenues increased 5%, or 7% excluding the European distribution center transition, benefiting from strength in blouses, wovens, sweaters and polos. Per management, encouraging traction in its premium Blue Tab collection as Levi Strauss expanded beyond its traditional denim franchise.

The company added nearly 3 million new loyalty members during the quarter, bringing total global membership to almost 50 million. Meanwhile, e-commerce represents about 12% of company revenues despite growing nearly 60% over the past three years, highlighting a significant long-term growth opportunity.

LEVI's Margins & Expenses

Gross profit increased to $979.1 million from $905.8 million in the year-ago quarter. Gross margin expanded 10 basis points to 62.7%, backed by the lower product costs and pricing actions, partly offset by tariffs and foreign exchange headwinds.

Selling, general and administrative expenses were $843.4 million compared with $791 million in the prior-year quarter. Adjusted SG&A increased 6.5% to $837.9 million, mainly due to higher selling expenses and unfavorable foreign exchange impacts. The adjusted SG&A margin declined 80 basis points year over year to 53.6% in the second quarter. Disciplined cost management helped adjusted EBIT margin expand 70 basis points to 9%.

Levi Strauss' Financial Snapshots

LEVI ended the second quarter with $849.3 million in cash and cash equivalents and total liquidity of approximately $1.8 billion, providing ample financial flexibility. Total inventories declined 7% year over year, reflecting disciplined inventory management.

Levi Strauss returned $53.9 million to shareholders through dividends during the quarter and continues to have $240 million available under its share repurchase authorization. Adjusted free cash flow increased nearly 60% year over year to $230.9 million. The company announced a quarterly dividend of 16 cents per share, representing a 14% increase from the prior year.

LEVI’s Q3 Guidance

The company expects continued business momentum in the third quarter, with reported and organic net revenues projected to increase 4%-5% year over year, despite no anticipated benefit from foreign exchange.

Gross margin is expected to expand by approximately 10 basis points to 61.8%, even with an estimated 70-basis-point foreign exchange headwind. Adjusted EBIT margin is projected to improve to 11.9%, reflecting continued operating leverage and disciplined cost management.

Adjusted EPS is expected to be in the range of 34-36 cents, including a 2-3 cents per share headwind from a higher tax rate and the impact of foreign exchange on gross margin. Management expects margin expansion to continue through the second half, with a more meaningful improvement anticipated in the fourth quarter.

What to Expect From LEVI in FY’26?

Following its strong first-half performance, Levi Strauss raised its fiscal 2026 outlook. Management said the company is taking into account the entire second-quarter beat into its updated guidance, reflecting confidence in continued business momentum.

The company now expects reported revenue growth of 7%-7.5%, up from the previous 5.5%-6.5% forecast. Organic revenue growth is projected at 5.5%-6%, compared with the earlier 4.5%-5.5% range.

Gross margin is expected to expand by approximately 10 basis points, supported by a favorable sales mix, including higher DTC sales, continued growth in the women's category, stronger international performance, lower promotional activity and ongoing cost-efficiency initiatives. The company expects an adjusted EBIT margin of 12% for the full year.

Adjusted EPS guidance was raised to $1.46-$1.52 from the previous $1.42-$1.48 range, despite incorporating an estimated 4-cent-per-share headwind from a higher tax rate. The outlook assumes current tariff levels remain in place and does not anticipate any significant deterioration in macroeconomic conditions, inflation, supply-chain disruptions or currency movements.

The company continues to expect 50-60 net new store openings during fiscal 2026, with most openings planned for the second half. Management reaffirmed confidence in achieving its long-term objectives of $10 billion in annual revenues and a 15% operating margin, supported by profitable growth and disciplined execution.

LEVI Stock Past Three-Month Performance

Image Source: Zacks Investment Research

Shares of this Zacks Rank #2 (Buy) company have risen 7.8% over the past three months against the industry’s 1.2% decline.

Other Solid Picks in Retail

Genesco Inc. GCO is a Nashville-based specialty retail and branded company. It sells footwear and accessories in retail stores. The company flaunts a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Genesco’s current fiscal-year earnings indicates growth of 55.2% from the year-ago actuals. GCO delivered a trailing four-quarter average earnings surprise of 3.8%.

Designer Brands Inc. DBI designs, produces and retails footwear and accessories. It offers shoes, boots, sandals, sneakers, socks, handbags and accessories. It currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Designer Brands’ current fiscal-year earnings and sales suggests growth of 137.5% and 0.5%, respectively, from the year-ago actuals. DBI delivered a trailing four-quarter average earnings surprise of 112.8%.

Tapestry, Inc. TPR is the designer and marketer of fine accessories and gifts for women and men in the United States and internationally. The company carries a Zacks Rank #2 at present.

The Zacks Consensus Estimate for Tapestry’s current fiscal-year earnings and sales indicates growth of 36.5% and 13.9%, respectively, from the year-ago actuals. TPR delivered a trailing four-quarter average earnings surprise of 15.6%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Levi Strauss & Co. (LEVI): Free Stock Analysis Report

Genesco Inc. (GCO): Free Stock Analysis Report

Tapestry, Inc. (TPR): Free Stock Analysis Report

Designer Brands Inc. (DBI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).