Vishay Intertechnology, Inc.'s VSH Vishay 3.0 strategy is designed to improve profitability by expanding manufacturing capacity, strengthening customer relationships and increasing exposure to faster-growing markets. While the company is still investing heavily, early results suggest that the strategy is beginning to support sustainable margin expansion.

Financial results for the first quarter of 2026 reflected encouraging progress. Revenues increased 17.3% year over year to $839.2 million, beating management's guidance. Gross margin improved to 21%, up from 19.6% in the previous quarter and 19% in the year-ago quarter. Operating margin also expanded to 2.6% from 1.8% in the fourth quarter of 2025, supported by stronger shipment volumes and improved factory utilization.

Demand has strengthened across industrial, automotive, aerospace and AI-related applications. Vishay Intertechnology reported a healthy book-to-bill ratio of 1.34, including an impressive 1.47 for semiconductors. Backlog increased 21% to $1.6 billion, providing strong revenue visibility and supporting higher capacity utilization in the coming quarters.

Vishay Intertechnology expects additional margin improvement in the second quarter. Revenues are projected between $875 million and $905 million, while gross margin is expected to reach roughly 22% despite higher metals and material costs. Recently implemented price increases should also contribute more meaningfully during the second and third quarters.

Although elevated capital spending on its new German 12-inch fab and other expansion projects may pressure free cash flow in the near term, these investments position Vishay Intertechnology to benefit from future demand growth. As capacity utilization rises and pricing actions take hold, Vishay 3.0 appears well-positioned to deliver sustainable margin expansion over the long run.

How Vishay Intertechnology Compares With Key Industry Rivals

Vishay Intertechnology's closest competitors, ON Semiconductor ON and Diodes Incorporated DIOD, are also working to improve margins through a richer product mix and manufacturing efficiency.

ON Semiconductor continues shifting its portfolio toward higher-margin silicon carbide (SiC), intelligent power and automotive solutions. In the first quarter of 2026, the company’s non-GAAP gross margin expanded by 30 basis points sequentially to 38.5%. This was primarily driven by increased manufacturing facility utilization (reaching 77% in the first quarter), enhanced operational efficiencies under its "Fab Right" strategy, and a richer product mix favoring higher-margin intelligent power products for AI data centers and automotive applications.

Diodes is also expanding its presence in automotive, industrial and AI power management applications. The company posted first-quarter 2026 revenues of $405.5 million, up 22.1% year over year, while its gross margin improved 30 basis points to 31.8%. Sequentially, Diodes’ gross margin expanded by 70 basis points, primarily driven by increased revenue contribution from higher-margin automotive and industrial segments and improved manufacturing facility utilization rates.

VSH’s Price Performance, Valuation and Estimates

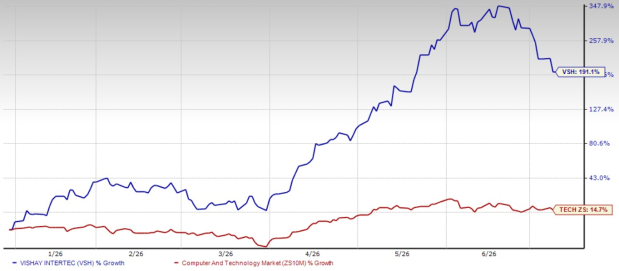

Shares of Vishay Intertechnology have skyrocketed 191.1% so far this year compared with the Zacks Computer and Technology sector’s 14.7% gain.

Vishay Intertechnology YTD Price Return Performance

Image Source: Zacks Investment Research

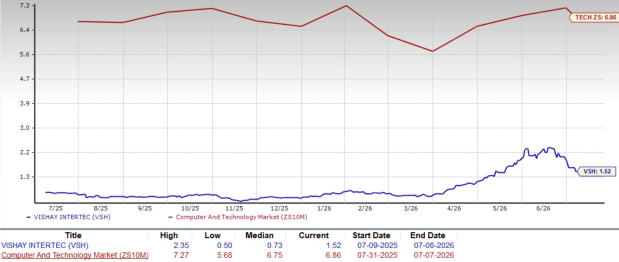

From a valuation standpoint, VSH trades at a forward 12-month price-to-sales ratio of 1.52, significantly below the sector average of 6.86. Vishay carries a Value Score of C.

Vishay Intertechnology Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Vishay Intertechnology’s 2026 earnings is pegged at 75 cents per share, implying a robust improvement from the loss of 5 cents in 2025. The consensus mark of $1.54 per share for 2027 earnings calls for a 105% year-over-year surge. Estimates for 2026 and 2027 have been revised upward over the past 60 days.

Image Source: Zacks Investment Research

Vishay Intertechnology currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vishay Intertechnology, Inc. (VSH): Free Stock Analysis Report

Diodes Incorporated (DIOD): Free Stock Analysis Report

ON Semiconductor Corporation (ON): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).