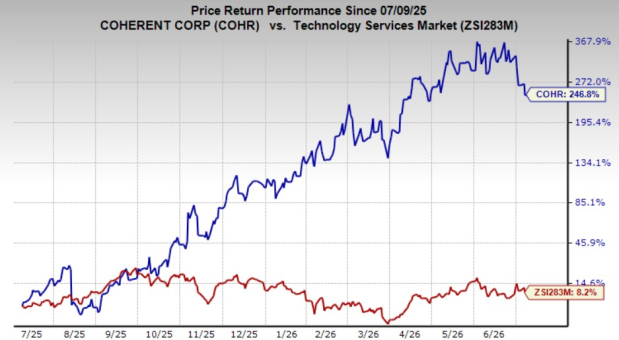

Coherent Corp. COHR has been one of the standout performers in the technology hardware space over the past year. The stock has surged an impressive 247%, significantly outperforming the industry's 8% growth and the Zacks S&P 500 Composite's 24% advance. More recently, however, COHR has pulled back 11% over the past month, suggesting the stock may be entering a healthy correction after its remarkable run.

The recent weakness raises an important question for investors: Is this a buying opportunity, a signal to hold existing positions, or a reason to stay on the sidelines? While the valuation remains elevated, Coherent's strengthening fundamentals indicate that the company's long-term growth story remains intact.

AI Infrastructure Demand Is Reshaping COHR’s Business

Coherent's transformation has been fueled by booming demand for AI infrastructure. The company's Datacenter & Communications segment has become its primary growth engine, accounting for 75% of third-quarter fiscal 2026 revenues while delivering 41% year-over-year growth.

This shift is significant because it changes the company's revenue profile. Historically, hardware manufacturers have been exposed to short product cycles and volatile demand. Today, Coherent is increasingly tied to long-duration AI infrastructure spending, providing investors with greater confidence in future earnings.

Unlike traditional semiconductor hardware cycles, AI-related investments are supported by large-scale cloud deployments and multi-year capital spending plans, making demand considerably more predictable.

Long-Term Orders Improve COHR’s Revenue Visibility

One of the biggest positives for Coherent is the dramatic improvement in order visibility.

Rather than experiencing the typical cyclical increase in hardware demand, the company is witnessing a step-change in customer commitments. Record backlog levels now extend into calendar 2028, while long-term supply agreements stretch through 2030.

This level of visibility substantially lowers the risk that new manufacturing investments become underutilized during an economic slowdown.

To support this unprecedented demand, Coherent invested approximately $290 million in capital expenditures during the third quarter of fiscal 2026, more than doubling spending from the prior-year period.

Importantly, this aggressive capacity expansion is backed by contractual customer commitments rather than speculative demand forecasts.

Operating Leverage is Beginning to Pay Off

The surge in AI-related demand is translating directly into stronger profitability.

Higher factory utilization and improved supply chain efficiencies contributed to a 163-basis-point expansion in the adjusted operating margin during the third quarter. Meanwhile, adjusted net income climbed nearly 56% year over year, highlighting the operating leverage created by rising production volumes.

As manufacturing assets become increasingly utilized, incremental revenues are flowing through to earnings at a faster pace, improving the overall quality of Coherent's financial performance.

This combination of expanding margins and stronger earnings suggests the company is benefiting not only from higher sales but also from greater operational efficiency.

Strategic Partnerships Strengthen Financial Flexibility

Coherent has also significantly strengthened its balance sheet.

A major catalyst came from NVIDIA's NVDA $2 billion equity investment, which increased Coherent's cash balance to roughly $3 billion during the third quarter of fiscal 2026 from approximately $1.5 billion in the previous quarter.

Beyond the financial benefits, NVIDIA's investment serves as an important strategic validation of Coherent's technology and its role within the rapidly expanding AI infrastructure ecosystem.

Management has simultaneously accelerated debt reduction. During the quarter, Coherent repaid $162 million of debt, reducing its leverage ratio to 0.5X from 1.7X in the previous quarter.

Lower leverage, higher liquidity and declining interest costs collectively provide the company with considerably greater financial flexibility as it continues investing in future growth.

Premium Valuation Appears Supported by Improving Fundamentals

Coherent currently trades at approximately 37.56 times forward earnings, nearly double the industry's 21.49 times forward earnings multiple.

At first glance, that premium valuation may appear demanding. However, investors are paying for a business that is becoming fundamentally different from the cyclical hardware manufacturer it once was. Multi-year customer commitments, record backlog, expanding margins, stronger cash generation and a healthier balance sheet are all contributing to a more predictable earnings profile.

While short-term volatility is always possible following such a strong rally, Coherent's growing exposure to AI infrastructure spending and long-term customer agreements provides a solid foundation for sustained growth over the coming years.

Coherent's Top and Bottom Line Expectations Remain Robust

Coherent's growth prospects remain compelling, supported by strong demand across AI-driven datacenter infrastructure and improving operating leverage. The Zacks Consensus Estimate projects fiscal 2026 revenues of $7.1 billion, indicating 21.5% year-over-year growth. Momentum is expected to accelerate further in fiscal 2027, with revenues forecast to increase 37.7% from the prior year.

The earnings outlook is equally impressive. The consensus estimate indicates fiscal 2026 EPS of $5.47, suggesting 55% year-over-year growth. Looking ahead, analysts expect EPS to climb another 52.5% in fiscal 2027, indicating confidence that Coherent's expanding AI-related business, improving margins and higher manufacturing utilization will continue to drive profitability.

Such robust top- and bottom-line projections reinforce the investment case that Coherent's transition toward AI infrastructure is creating a stronger, more predictable earnings profile despite the stock's premium valuation.

Peers to Watch: Lumentum and IPG Photonics

Among U.S.-listed peers, Lumentum Holdings LITE and IPG Photonics IPGP offer useful comparisons for investors evaluating Coherent. Like Coherent, both LITE and IPGP operate in optical components and photonics markets that benefit from increasing demand for high-speed data communications and advanced laser technologies. However, Coherent currently stands apart because of its unusually strong AI infrastructure exposure, record backlog extending into 2028, long-term supply agreements through 2030, and a significantly strengthened balance sheet following NVIDIA's strategic investment. These factors have helped improve earnings visibility and differentiate Coherent's growth profile within the photonics industry.

COHR Remains a Buy for Long-Term AI Investors

Coherent’s remarkable rally reflects meaningful improvements in its business rather than market enthusiasm alone. The company has strengthened its revenue visibility through long-term customer commitments, expanded profitability as AI-driven demand boosts operating leverage, and reinforced its balance sheet with greater financial flexibility. Although the stock trades at a premium and could experience periodic volatility after its strong advance, its transformation into a critical supplier for AI infrastructure supports a more durable growth outlook. With robust revenue and earnings expectations, improving execution and favorable industry trends, Coherent remains an attractive buy for investors seeking long-term exposure to the expanding AI ecosystem.

COHR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Coherent Corp. (COHR): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

IPG Photonics Corporation (IPGP): Free Stock Analysis Report

Lumentum Holdings Inc. (LITE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).