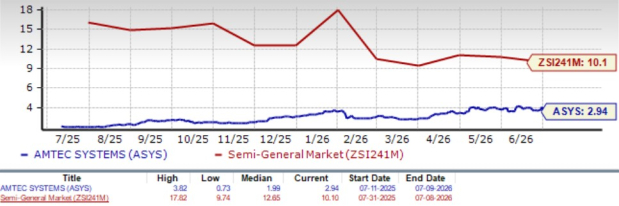

Amtech Systems ASYS appears attractively valued, trading at a discount to both its industry and broader sector benchmarks. The stock currently trades at a forward 12-month price-to-sales (P/S) ratio of 2.94X, representing a 71% discount to the Zacks Semiconductor – General industry's average of 10.1X. The multiple is also significantly lower than the broader Computer and Technology sector average of 6.89X and the S&P 500 average of 5.02X.

This discounted valuation suggests the market may not be fully recognizing Amtech's long-term strategic positioning and AI-driven growth opportunities.

The stock also trades at a lower P/S multiple than its peers, including Intel Corporation INTC, STMicroelectronics STM and Texas Instruments Incorporated TXN. Intel Corporation, STMicroelectronics and Texas Instruments currently trade at forward 12-month P/S ratios of 9.27X, 4.1X and 12.86X, respectively.

ASYS’ Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

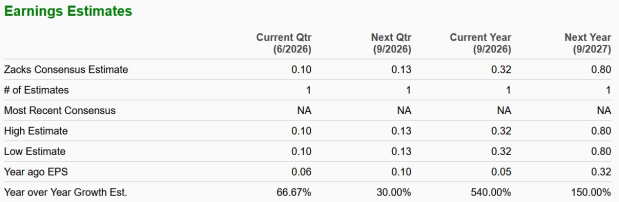

Supporting the valuation case, Amtech Systems' earnings outlook remains encouraging. The Zacks Consensus Estimate for ASYS' fiscal 2026 and 2027 earnings is pegged at 32 cents and 80 cents per share, respectively. Both have remained unchanged over the past 30 days, implying robust year-over-year growth of 540% and 150%, respectively.

Image Source: Zacks Investment Research

This combination of discounted valuation and strong earnings growth raises an important question: Does ASYS’ primary business strength justify this optimism? Let’s take a closer look.

ASYS' AI Packaging Strength Drives Long-Term Growth

Amtech Systems' long-term investment strategy is increasingly centering on AI-driven advanced packaging, where the company has established a differentiated position through its Thermal Processing Solutions business. As AI processors become larger and more complex, advanced packaging technologies such as 2.5D, 3D, CoWoS, panel-level packaging and high-performance server board assembly are becoming essential.

Management noted that AI-related sales exceeded 30% of Thermal Processing Solutions revenues in the second quarter of fiscal 2026 and are expected to surpass 40% in the following quarter. The company is benefiting from its proprietary TrueFlat technology and industry-leading temperature uniformity, which enable higher production yields for complex AI semiconductor packages. It is also investing in next-generation, higher-density packaging systems that could expand its addressable market beyond fiscal 2026.

Amtech believes global AI infrastructure expansion, increasing investments by semiconductor manufacturers and OSATs, and growing adoption of advanced packaging will support sustained equipment demand. In June 2026, the company further strengthened its strategy through a $60 million public offering — which was oversubscribed — with the proceeds earmarked to accelerate the growth of its semiconductor packaging platform and fund strategic acquisitions.

ASYS' Three Growth Pillars Support Expansion

Amtech Systems is leveraging three structural growth opportunities — artificial intelligence, global supply chain diversification, and advanced mobility — to strengthen its long-term growth potential. The company believes rising AI adoption will continue driving demand for its advanced semiconductor packaging equipment, while global manufacturing diversification beyond mainland China is creating new opportunities in regions such as Southeast Asia and Mexico. Meanwhile, increasing adoption of EVs, HEVs and advanced automotive electronics is expected to support demand for its thermal processing and semiconductor fabrication solutions.

To capitalize on these trends, the company is investing in next-generation AI packaging equipment, expanding its consumables portfolio and strengthening technical capabilities. These initiatives are expected to broaden its addressable market, enhance recurring revenue opportunities and support sustainable long-term growth.

While these structural growth drivers strengthen ASYS' long-term outlook, investors should also recognize several business-specific headwinds that could moderate the pace of future growth.

ASYS Faces Pressure From Weak SFS Demand

Amtech Systems' Semiconductor Fabrication Solutions ("SFS") segment remains a key challenge despite the company's strong momentum in AI-driven semiconductor packaging. The company acknowledged that the benefits of customer-centric growth initiatives were largely overshadowed by weak demand for PR Hoffman products, driven by slower spending from key silicon carbide (SiC) customers.

Although promising signs are emerging in this sector — including 15% revenue growth from IDI’s specialty chemicals and a nearly 40% increase in revenues from Entrepix’s parts and services in the second quarter of fiscal year 2026 — these recurring revenue streams have not yet been sufficient to offset the weakness in demand for equipment.

The company is investing in expanding its consumables portfolio, strengthening application development and enhancing technical support to build a more resilient, recurring revenue model. Nevertheless, management expects the benefits of these initiatives to materialize primarily beyond fiscal 2026. From an investor's perspective, the continued slowdown in demand related to silicon carbide and the ongoing transformation of the SFS business could negatively impact overall growth and profitability.

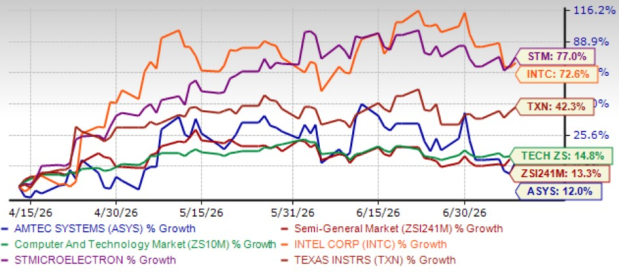

ASYS Stock Underperforms Industry, Sector & Peers

ASYS' shares have gained a modest 12% over the past three months, trailing the broader sector and industry. During the same period, the sector has increased 14.8%, while the industry has returned 13.3%, reflecting relatively weaker near-term market performance for the stock.

The underperformance is even more prominent when compared with peers such as Intel Corporation, STMicroelectronics and Texas Instruments. Over the same three-month period, shares of Intel Corporation, STMicroelectronics and Texas Instruments have appreciated 72.6%, 77% and 42.3%, respectively, underscoring relatively weaker investor sentiment toward ASYS.

ASYS’ Three-Month Price Performance Vs. Peers

Image Source: Zacks Investment Research

Conclusion: Maintain a Hold Stance on ASYS

Amtech Systems offers an attractive valuation, expanding exposure to AI-driven semiconductor packaging and multiple long-term secular growth opportunities. However, persistent weakness in its Semiconductor Fabrication Solutions business, cyclical industry risks and relatively weak stock performance temper the near-term outlook. Considering this balanced risk-reward profile, we recommend investors hold ASYS stock for the time being.

ASYS currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Amtech Systems, Inc. (ASYS): Free Stock Analysis Report

Intel Corporation (INTC): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

STMicroelectronics N.V. (STM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).