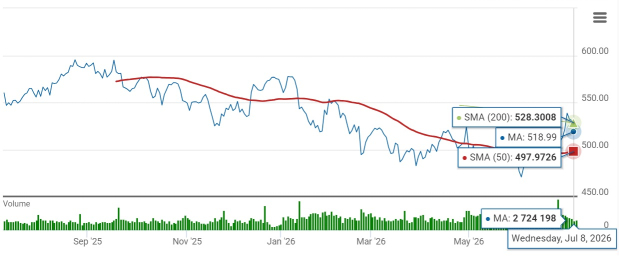

Mastercard Incorporated MA slipped below its 200-day simple moving average (SMA) this week. On July 8, 2026, the stock closed at $518.99, below its 200-day SMA of $528.30. For technical investors, that's a signal worth watching because the 200-day SMA is widely viewed as a gauge of a stock's long-term trend. Trading below it often suggests that bullish momentum has weakened.

The stock has rebounded from its early-June lows and briefly climbed back above its 200-day SMA before slipping below it again. That failure to hold the level suggests buyers are still struggling to regain long-term control. Even so, Mastercard remains comfortably above its 50-day SMA since late June, indicating that short-term momentum has held up even as the longer-term trend remains under pressure. That combination puts the stock at an important technical crossroads, with investors now watching whether it can reclaim the 200-day level for good or face another bout of selling pressure.

Mastercard 50 and 200 Day SMA

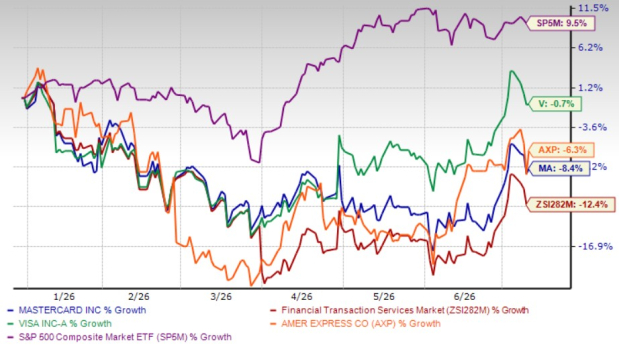

Despite the improvement from early-June levels, the stock is still down 8.4% year to date, trailing rival Visa Inc. V, down 0.7%, and American Express Company AXP, down 6.3%. That said, Mastercard's decline has been milder than the broader industry, which has dropped 12.4% over the same period. The S&P 500, by contrast, has gained 9.5% year to date.

YTD Price Performance – MA, V, AXP, Industry & S&P 500

Even after delivering solid operating results, investors have become less willing to pay elevated multiples as the payments sector faces concerns over global economic growth, prompting a rotation into areas such as energy, industrials and defense and away from richly valued technology and payment names during periods of heightened geopolitical tension.

Beyond that broader sector rotation, a pullback in valuation also likely reflects investors assigning greater weight to regulatory and competitive risks than they have in the past.

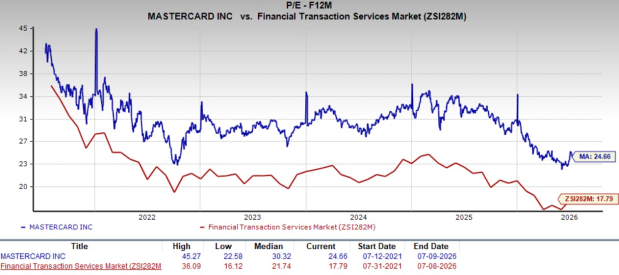

MA’s Valuation Below Historical Levels

Despite the share price decline, Mastercard still commands a premium valuation, though not to the same extent as in recent years. It is currently trading at a forward P/E ratio of 24.66X, lower than its five-year median of 30.32X but still above the industry average of 17.79X. The lower multiple suggests investors have become more cautious, reflecting concerns over regulation, competition and the broader macro environment. By comparison, Visa trades at 24.12X and American Express at 18.28X.

Regulatory and Competitive Risks to Watch

Mastercard continues to face regulatory scrutiny across key markets. In the United States, the Department of Justice has accused Mastercard and Visa of using their dominant positions to maintain high merchant fees, while the bipartisan Credit Card Competition Act remains under consideration, though it has yet to gain significant traction.

In Europe, regulatory pressure is mounting. In June 2025, London's Competition Appeal Tribunal ruled that the companies' multilateral interchange fees breached competition law. Britain's Payment Systems Regulator is also weighing enhanced disclosure requirements for their U.K. operations, a move that could bolster future pricing oversight. At the same time, European policymakers are exploring alternatives to traditional card networks, with U.K. banks assessing domestic payment systems and the European Central Bank advancing the digital euro to reduce reliance on U.S.-based payment providers.

Stablecoins also pose a long-term risk. The concern isn't that they will replace Mastercard overnight, but that large retailers or technology platforms could eventually build payment ecosystems around digital currencies, allowing some transactions to bypass traditional card networks. While that scenario remains speculative, it is a structural risk worth watching. At the same time, fintechs and real-time payment networks continue to intensify competition. As merchants gain access to faster and lower-cost payment alternatives, Mastercard could face increasing pressure on transaction volumes and pricing power.

Nevertheless, rather than viewing fintech and crypto as threats, Mastercard is embedding itself in both. The planned $1.8 billion acquisition of BVNK will expand its stablecoin infrastructure and strengthen connections between blockchain-based payment rails and its global network, reinforcing management's view that digital assets complement rather than replace traditional payments.

The Bigger Picture Extends Beyond the Charts

For a company like Mastercard, long-term performance is ultimately driven by business fundamentals rather than chart patterns alone.

The company continues to benefit from the global shift toward electronic payments, expanding card usage, rising cross-border spending and growing demand for value-added services. These structural trends have supported Mastercard's business for years and remain important drivers of revenue and earnings growth, helping underpin its long-term investment case.

Mastercard is also positioning itself for the next generation of payments through Agent Pay, backed by Google, Microsoft and OpenAI. Nearly all Mastercard cards can now support AI-driven transactions, while its Verifiable Intent technology, launched in the first quarter and adopted by the FIDO Alliance, helps securely authenticate AI-initiated payments. Management believes B2B agent payments represent the biggest long-term opportunity.

The Business is Holding Up

Recent results suggest the business is holding up much better than the stock price would indicate.

In the first quarter of 2026, cross-border volume increased 13% year over year, easing concerns that Middle East tensions would weigh on international travel. Gross dollar volume rose 7% on a local-currency basis to $2.7 trillion, while switched transactions grew 9%, pointing to healthy consumer and commercial spending.

Growth remains strong beyond the core payments business. Revenues from value-added services climbed 22% to $3.5 billion, fueled by demand for cybersecurity, fraud prevention, digital authentication and analytics. As digital payments expand, these higher-margin offerings are becoming an increasingly important driver of growth.

Mastercard also continues to reward shareholders. In the first quarter, it returned $4.8 billion through $4 billion in share repurchases and $777 million in dividends. The company still had $11.7 billion remaining under its buyback authorization as of late April 2026, after repurchasing another $1.7 billion of stock early in the second quarter.

Estimates for MA Remain Favorable

For the full-year 2026, the Zacks Consensus Estimate for earnings now sits at $19.61 per share, indicating 15.3% growth over last year. For 2027, that number climbs to $22.68, implying another 15.7% increase. Revenues are forecast at $37 billion this year and $41.64 billion the next, with nearly 13% growth each year.

Mastercard has also beaten earnings estimates for four consecutive quarters, with an average surprise of 5.5%.

Mastercard Incorporated Price, Consensus and EPS Surprise

Mastercard Incorporated price-consensus-eps-surprise-chart | Mastercard Incorporated Quote

Final Words

Mastercard's drop below its 200-day SMA suggests the stock has yet to regain long-term technical strength, even as short-term momentum improves. For investors considering the recent pullback, the decision comes down to whether strong fundamentals outweigh that technical setup.

Regulatory scrutiny, emerging payment alternatives and a premium valuation may keep sentiment in check in the near term. Still, the company's resilient operating performance, strong earnings outlook and continued investments in AI and digital payments support its long-term growth story. With a Zacks Rank #3 (Hold), investors may prefer to wait for a decisive technical breakout or a more attractive entry point before becoming more constructive on the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Mastercard Incorporated (MA): Free Stock Analysis Report

Visa Inc. (V): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).