Super Micro Computer SMCI is chasing explosive AI-driven revenue growth, while its rising working-capital intensity is something to look at. During the first nine months of fiscal 2026, the company generated more than $1 billion in net income but consumed $7.6 billion in operating cash.

Since June 2025, accounts receivable increased from $2.2 billion to $8.4 billion, while inventories surged from $4.7 billion to $11.1 billion. The cash conversion cycle also nearly doubled sequentially to 106 days. Therefore, it is important to monitor whether receivables and inventory normalize as delayed AI deployments come online or whether heavy working-capital requirements are becoming structural.

Margin sustainability is another critical aspect. SMCI’s non-GAAP gross margin recovered to 10.1% from 6.4% sequentially. However, the company expects it to fall back to 8.2-8.4% in the fourth quarter. Large AI customers generate enormous volumes but also possess significant pricing power.

One customer alone represented 27% of third-quarter revenues, making the customer mix a major determinant of profitability. For SMCI, the success of Data Center Building Block Solutions (DCBBS) will therefore be crucial. By bundling servers with cooling, power, networking, software and services, SMCI aims to capture more value from each deployment and improve margins.

However, investors need clearer evidence that DCBBS is materially changing the company’s economics. SMCI also faces stiff competition as the AI data center market is likely to grow at an unprecedented pace throughout 2026 and 2027.

How Competitors Fare Against SMCI

Big players like Hewlett Packard Enterprise HPE and Dell Technologies DELL are competing with SMCI in this space.

Dell Technologies is a major supplier of servers and storage systems, with a broad customer base across enterprises and cloud providers. Its scale, established distribution and service offerings give it an edge in winning large contracts. However, Dell Technologies has not grown as quickly as SMCI in AI-specific systems; its ability to bundle hardware with services makes it a strong rival.

Hewlett Packard Enterprise is also expanding aggressively into AI and high-performance computing. Its GreenLake platform provides customers with flexible, cloud-like consumption models, which can be attractive to enterprises. Hewlett Packard Enterprise’s focus on hybrid cloud and AI workloads positions it as a direct competitor in areas where SMCI is seeking growth through its DCBBS strategy.

Hewlett Packard Enterprise offers a range of servers, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. Dell Technologies has built the Dell AI Factory in collaboration with NVIDIA. Dell also collaborated with Red Hat Enterprise Linux AI for Dell PowerEdge servers.

SMCI’s Price Performance, Valuation and Estimates

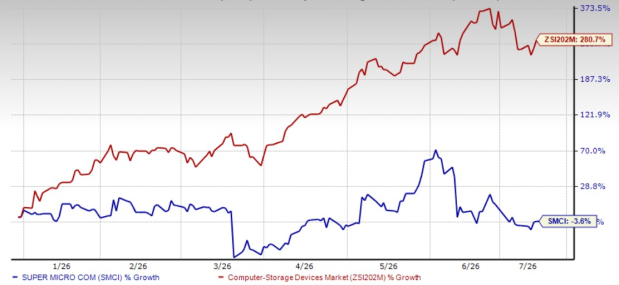

Shares of Super Micro Computer have lost 3.6% year to date against the Zacks Computer – Storage Devices industry’s growth of 280.7%.

SMCI YTD Performance Chart

Image Source: Zacks Investment Research

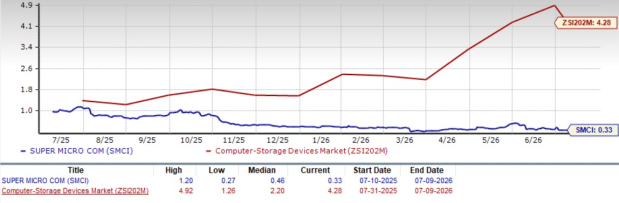

From a valuation standpoint, SMCI is trading at a discount at a forward 12 Month P/S multiple of 0.33X compared with the industry’s P/S multiple of 4.28X.

SMCI Forward 12-Month (P/S) Valuation Chart

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Super Micro Computer’s fiscal 2026 and 2027 earnings implies a year-over-year increase of approximately 24.27% and 22.9%, respectively. Estimates for fiscal 2026 and 2027 earnings have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Super Micro Computer currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Super Micro Computer, Inc. (SMCI): Free Stock Analysis Report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).