ASML Holding ASML is slated to report second-quarter 2026 results before the market opens on July 15, 2026.

ASML expects revenues between €8.4 billion and €9 billion. The Zacks Consensus Estimate is pegged at $10.28 billion, indicating a 17.8% increase from the year-ago quarter’s level.

The Zacks Consensus Estimate for earnings is pegged at $7.98 per share, suggesting an increase of 75.4% from the year-ago quarter’s earnings of $4.55. The estimate has been revised downward by 3 cents over the past 30 days.

Image Source: Zacks Investment Research

The company’s earnings outpaced the Zacks Consensus Estimate twice in the trailing four quarters while missing on two occasions, the average negative surprise being 4.54%.

ASML Holding N.V. Price and EPS Surprise

ASML Holding N.V. price-eps-surprise | ASML Holding N.V. Quote

Q2 Earnings Whispers for ASML Holding

Our proven model does not conclusively predict an earnings beat for ASML this season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. However, that’s not the case here.

ASML Holding currently carries a Zacks Rank #4 (Sell) and has an Earnings ESP of -1.04%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Likely to Have Shaped ASML’s Q1 Performance

ASML Holding’s second-quarter performance is likely to have benefited from the rising demand for its lithography tools, which is gaining traction on the back of the need to produce more complex logic, DRAM, HBM and NAND chips. ASML’s EUV technology is gaining the highest traction among DRAM, followed by HBM and DDR.

Shift toward High NA-EUV technology, strong usage of ASML’s DUV technology in China and EUV in the rest of the world are likely to have driven the company’s top line in the to-be-reported quarter. As AI and high-performance computing processes like training and inference require better HBM and DRAM chips, ASML’s advanced etching tools will remain in demand.

The growing popularity of ASML Holding’s NXE:3800 low numerical aperture (NA) machine, which can process 220 wafers per hour, is likely to have driven substantial EUV sales in the to-be-reported quarter. The industry’s shift from 4nm to 2nm nodes has led to single-exposure EUV technology gaining popularity. EUV is likely to have gained traction in the to-be-reported quarter.

ASML Holding’s upgrade and service business has been a strong contributor to its Installed Base Management segment throughout the past year. In the first quarter of 2026, ASML’s IBM sales increased 25% year over year to €2.5 billion, driven by higher service and upgrades of its wafer fabrication equipment business, which is likely to have persisted in the second quarter of 2026.

ASML’s Price Performance, Valuation and Estimates

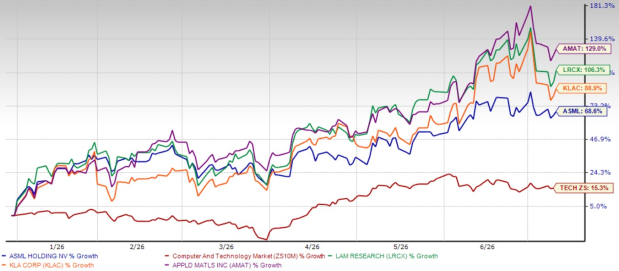

Shares of ASML Holding have gained 68.6% year to date compared with the Computer and Technology sector’s growth of 15.3%. However, compared with semiconductor peers, ASML stock has underperformed KLA Corporation KLAC, Lam Research Corporation LRCX and Applied Materials, Inc. AMAT. YTD, shares of KLA Corporation, Lam Research and Applied Materials have jumped 88.9%, 106.3% and 129%, respectively.

ASML Holding YTD Price Return Performance

Image Source: Zacks Investment Research

Now, let’s look at the value that ASML offers to its investors at the current level. Currently, ASML Holding is trading at a premium. With a forward 12-month P/E of 41.62X, ASML is trading marginally higher than the sector’s average of 24.53X.

ASML Holding Forward 12-Month Price-To-Earnings Ratio

Image Source: Zacks Investment Research

Compared to semiconductor peers, the stock trades at a higher multiple than Applied Materials, while at a lower multiple than Lam Research and KLA Corporation. Currently, Applied Materials, Lam Research and KLA Corporation have a forward 12-month P/E ratio of 39.82, 44.66 and 45.88, respectively.

Investment Thesis for ASML Holding Stock

ASML has a clear advantage in the chip equipment market. It is the only company capable of producing EUV lithography machines at scale. These machines are needed to make chips at 5nm, 3nm and soon 2nm levels — key to powering AI processors, mobile devices and data centers.

ASML Holding is already rolling out its next-generation High-NA EUV machines, which will be used for even smaller chips. As demand for faster and more efficient chips rises, especially with the growth of AI, ASML Holding stands to benefit. Its machines are a necessary part of the chip supply chain, and its customers, including TSMC, Intel and Samsung, will rely on ASML’s technology for years to come.

However, one concern is the company’s exposure to China. U.S. pressure on the Dutch government has led to export restrictions on some of ASML’s most advanced equipment, which could limit future sales in that market. Still, strong demand from other regions may offset that risk.

Another key risk is rising competition. Increasing participation from semiconductor equipment manufacturers, particularly in segments such as etching, could intensify competitive pressures as rivals leverage specialized technologies to secure customer contracts.

Final Thoughts: Exit From ASML Stock for Now

Though ASML Holding holds a dominant position in the EUV and High-NA EUV technologies, export restrictions on advanced semiconductors and equipment to China and rising competition may hurt the company’s prospects in the near term. A high valuation multiple also suggests a cautious approach to the stock. Therefore, it is wise for investors to stay away from the stock for now and make their investment decision once the company reports its second-quarter results.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ASML Holding N.V. (ASML): Free Stock Analysis Report

KLA Corporation (KLAC): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).