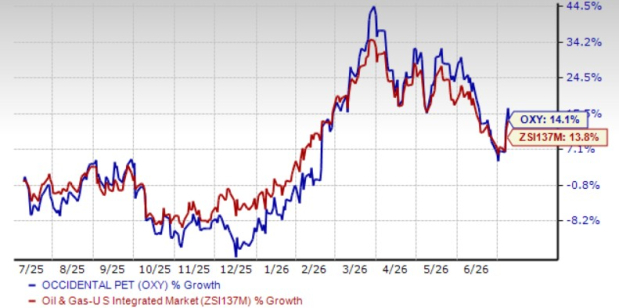

Occidental Petroleum Corporation’s OXY shares have gained 14.1% in the past nine months compared with the Zacks Oil and Gas-Integrated-United States industry’s rise of 13.8%.

The company’s strategic investments and consistent production growth continue to enhance its cash flow generation potential. The acquisition of CrownRock L.P. has significantly expanded the company’s presence in the Permian Basin, strengthening its long-term production profile and operational efficiency. In addition, the discovery of high-quality oil at the Bandit prospect in the Gulf of America is expected to support production growth over the long term.

On the downside, persistent geopolitical tensions in the Middle East and the resulting logistical challenges are expected to pressure Occidental’s sulfur sales volumes from the region during the second quarter.

Price Performance (Nine Months)

Image Source: Zacks Investment Research

Another operator in the same industry, Devon Energy Corporation DVN, has a multi-basin portfolio and focuses on high-margin assets that hold significant long-term growth potential. In the past nine months, DVN’s shares have gained 23.7%.

Should investors add Occidental stock to their portfolios solely based on its recent share price strength? Let's take a closer look at the company's fundamentals and key growth drivers to determine whether the current level offers an attractive entry point.

Tailwinds for Occidental

Occidental continues to strengthen its Permian Basin position through strategic investments and acquisitions. With nearly a decade of high-return drilling inventory and growing production from the acquired CrownRock assets, the company is well positioned to drive long-term production growth.

The Permian Basin remains Occidental’s primary production driver. The company expects Permian production of 783-803 thousand barrels of oil equivalent per day (Mboe/d) and total output of 1,390-1,430 Mboe/d in the second quarter of 2026. Additionally, Occidental plans to bring 460-510 wells online in the Permian and 150-170 wells in the Rockies during 2026, supporting further production growth.

OXY recently announced an oil discovery at the Bandit prospect in the Gulf of America, where drilling confirmed extensive, high-quality oil-bearing Miocene sands. This discovery is expected to support the company's long-term production growth. For second-quarter 2026, Occidental projects Gulf of America production of 128-136 Mboe/d.

Occidental’s low-cost operations and high-quality asset base provide a competitive advantage. Supported by strong cost discipline, capital efficiency and technology-driven optimization, the company expects to achieve $500 million in sustainable cost savings in 2026 compared with 2025 levels.

Occidental continues to strengthen its balance sheet through disciplined debt reduction. The company has lowered principal debt to $13.2 billion and aims to reduce it to $10 billion, enhancing financial flexibility and margins. Lower debt has already cut annual interest expense by $830 million, while steady cash flows are expected to support further deleveraging and increased shareholder returns through share repurchases.

Headwinds for Occidental Stock

Occidental’s earnings remain sensitive to fluctuations in global and regional commodity prices. With no active commodity hedges in place as of Dec. 31, 2025, the company is fully exposed to price volatility. A sustained decline in oil and gas prices could weigh on OXY’s financial performance.

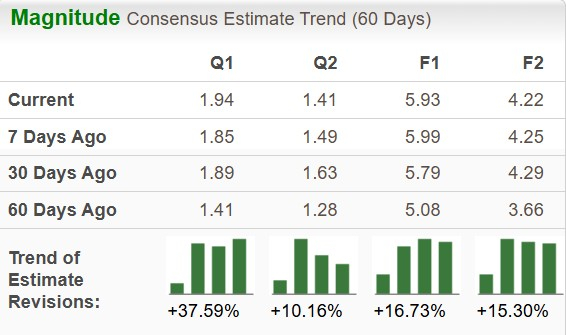

Occidental’s Earnings Estimates Are Going Up

The Zacks Consensus Estimate for Occidental’s 2026 and 2027 earnings per share indicates an increase of 16.73% and 15.3%, respectively, in the past 60 days.

Image Source: Zacks Investment Research

The same for Devon Energy’s 2026 and 2027 earnings per share indicates a decline of 10.76% and 3.18%, respectively, in the past 60 days.

OXY Stock’s Earnings Surprise History

The stable performance of the company allowed its earnings to surpass estimates in each of the last four reported quarters, the average surprise being 49.72%.

Image Source: Zacks Investment Research

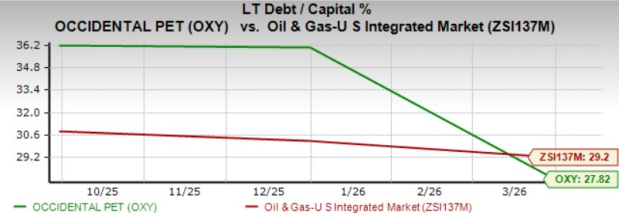

Occidental’s Long-Term Debt to Capital

Debt is essential in the oil and gas industry, helping companies finance capital-intensive exploration, production, infrastructure expansion and acquisitions while preserving liquidity. Effective debt management also enhances financial flexibility during commodity price cycles. Reflecting its disciplined approach, Occidental’s long-term debt-to-capital stands at 27.82%, below the industry average of 29.2%.

Image Source: Zacks Investment Research

Another oil and gas company, Chevron Corporation CVX, has substantial domestic and international oil and gas operations. The long-term debt-to-capital of CVX stands at 17.3%, lower than the industry average.

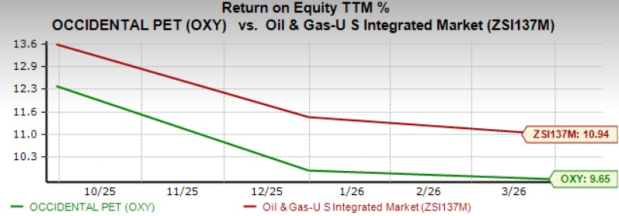

Return on Equity

Return on equity (“ROE”) is a key indicator of a company’s financial performance. It reflects how effectively a corporation uses shareholders' equity to generate profits and is widely regarded as a measure of profitability and operational efficiency.

Occidental’s ROE is lower than the industry average in the trailing 12 months. ROE of OXY is 9.65% compared with the industry average of 10.94%.

Image Source: Zacks Investment Research

Chevron’s ROE is currently pegged at 6.9% lower than its industry average.

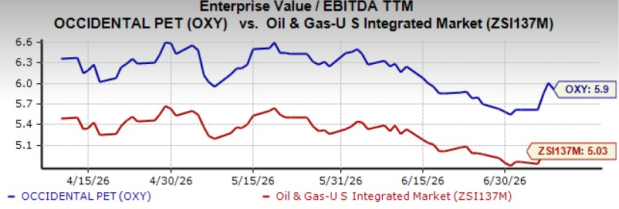

OXY’s Shares Are Trading at a Premium

Occidental’s shares are currently expensive on a relative basis, with the current trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA TTM) being 5.9X compared with its industry average of 5.03X.

Image Source: Zacks Investment Research

Rounding Up

Occidental’s focus on debt reduction, backed by the strength of its domestic and international operations and recent oil discoveries, is expected to support the overall financial and operational performance.

The company’s ongoing debt reduction efforts, improving earnings estimates and consistent operational performance enhance its investment appeal.

However, OXY is trading at a premium to its industry, while its ROE remains below the industry average. Given its current valuation, existing investors may consider holding this Zacks Rank #3 (Hold) stock, whereas prospective investors may be better off waiting for a more attractive entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Occidental Petroleum Corporation (OXY): Free Stock Analysis Report

Devon Energy Corporation (DVN): Free Stock Analysis Report

Chevron Corporation (CVX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).