Texas Instruments Incorporated’s TXN embedded processing business has returned to healthy growth, raising hopes that the segment can remain an important driver of the company’s long-term performance. Although the analog business remains the largest contributor, embedded processing is benefiting from improving industrial demand and increasing semiconductor content across connected devices, vehicles and factory automation.

In the first quarter of 2026, embedded processing revenues increased 12% year over year to $723 million. The segment’s operating profit more than tripled to $122 million from $40 million a year earlier, reflecting stronger sales and better factory utilization. The recovery shows that customer inventory adjustments are easing and end-market demand is gradually improving.

Texas Instruments is well-positioned to benefit from long-term growth trends. Its portfolio of microcontrollers and processors is widely used in industrial equipment, automotive systems, medical devices and communications infrastructure. Growing adoption of smart factories, advanced driver-assistance systems and connected industrial equipment is expected to increase demand for embedded chips over the coming years.

The company also benefits from its manufacturing strategy. Greater use of internally produced 300-millimeter wafers helps lower production costs while improving supply reliability. This gives Texas Instruments an advantage in serving customers during periods of rising demand.

However, management remains cautious about the second half of 2026 due to macroeconomic uncertainty and uneven demand across some markets. Automotive demand also remains mixed in certain regions. Even so, improving industrial activity, growing automation investments and expanding applications for embedded processors provide a favorable backdrop.

If these trends continue, Texas Instruments’ embedded business appears well-positioned to extend its double-digit growth run and contribute meaningfully to overall revenue and profit growth. The Zacks Consensus Estimate for TXN’s 2026 embedded processing revenues is currently pegged at $3 billion, indicating 11.4% year-over-year growth.

How Rivals Fare Against TXN in the Embedded Chip Market

Microchip Technology Incorporated MCHP and NXP Semiconductors N.V. NXPI are two leading competitors of Texas Instruments in the embedded processing market.

Microchip Technology offers a broad portfolio of microcontrollers, microprocessors and connectivity solutions used in industrial automation, automotive electronics and aerospace applications. The company is benefiting from broad-based demand improvement across end markets, stronger customer engagement and normalization of inventory levels across its supply and distribution channels. In the last reported financial results for the fourth quarter of fiscal 2026, Microchip Technology’s revenues surged 35% year over year to $1.31 billion.

NXP Semiconductors is another strong rival, with a leading position in automotive processors, secure connectivity and industrial embedded systems. Automotive accounts for more than half of NXPI’s revenue, supported by growing semiconductor content in electric vehicles and advanced driver-assistance systems. NXP Semiconductors is also expanding its edge AI and industrial IoT offerings to capture long-term growth opportunities. However, softer vehicle production in Europe and China has weighed on near-term sales. In the first quarter of 2026, NXP Semiconductors’ revenues increased 12% year over year to $3.18 billion.

TXN’s Price Performance, Valuation and Estimates

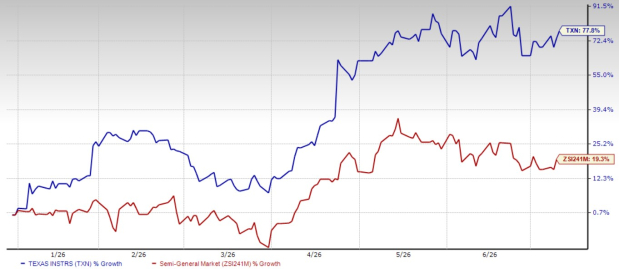

Shares of Texas Instruments have soared 77.8% year to date compared with the Zacks Semiconductor - General industry’s 19.3% growth.

Texas Instruments YTD Price Return Performance

Image Source: Zacks Investment Research

From a valuation standpoint, TXN trades at a forward price-to-earnings ratio of 37.43, significantly higher than the industry’s average of 22.65.

Texas Instruments Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Texas Instruments’ 2026 and 2027 earnings implies a year-over-year increase of 40.6% and 14.4%, respectively. Estimates for 2026 have remained unchanged over the past 60 days, while estimates for 2027 have been revised upward during the same time frame.

Image Source: Zacks Investment Research

Texas Instruments currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Microchip Technology Incorporated (MCHP): Free Stock Analysis Report

NXP Semiconductors N.V. (NXPI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).