Qualcomm Incorporated QCOM and Monolithic Power Systems MPWR are prominent players in the semiconductor space. While Monolithic focuses on power management solutions that improve efficiency in AI servers and data center infrastructure, Qualcomm develops AI-capable processors powering smartphones, connected vehicles and edge devices.

The semiconductor industry is witnessing robust growth, fueled by the rapid adoption of AI, cloud computing and high-performance computing. Rising investments in AI data centers, enterprise servers and advanced computing infrastructure are driving demand for both compute and power management technologies. Let us analyze in depth the competitive strengths and weaknesses of the companies to understand who is in a better position to maximize gains from the emerging market trends.

The Case for Qualcomm

Growing AI proliferation is reshaping the semiconductor industry and Qualcomm is positioning itself to capture the emerging opportunities. For a long time, Qualcomm generated most of its revenues from smartphones. However, that market has become mature. The company is also facing competition from several other players in the industry, such as MediaTek and Samsung Exynos. Amid this backdrop, QCOM has undertaken a prudent approach to diversify its revenue stream.

AI adoption is set to create opportunities across a broad spectrum beyond smartphones, that includes PCs, cars, robotics, industrial equipment, networking gear and data centers. Legacy data centers primarily handled applications such as databases, websites and enterprise software. Rising usage of generative AI and AI agents has significantly increased demand for computing power. AI data centers must support large language model inference, multimodal AI, reasoning and memory-intensive workloads. Qualcomm is aiming to capitalize on this domain.

The company boasts decades of expertise in designing high-performance, low-power processors. This might give the company a competitive edge. Qualcomm recently launched a comprehensive data center portfolio that includes the Dragonfly C1000 CPU, designed for AI orchestration, agentic workloads and general-purpose computing; the Dragonfly AI300 inference accelerator for AI inference applications. It has also introduced a new memory architecture, Qualcomm High Bandwidth Compute, engineered to address the issues related to memory bandwidth bottlenecks while improving energy efficiency.

Backed by solid momentum, Qualcomm significantly raised its long-term financial targets. The company increased the fiscal 2029 non-handset revenue target to $40 billion, nearly double its previous target of $22 billion. The revised outlook includes more than $15 billion in data center revenues, $10 billion in automotive revenues and more than $14 billion in IoT revenues by fiscal 2029. The company projects non-GAAP earnings per share to exceed $18 by fiscal 2029.

The case for Monolithic

Monolithic is steadily increasing its investment in Enterprise Data, communications and server portfolio, which continue to benefit from growing spending in AI infrastructure by businesses. Strong demand for AI accelerators, CPUs and server power management solutions is driving demand in the Enterprise Data segment.

Its strong focus on innovation is a positive factor. MPWR is actively testing its first high-speed DDR5 interface products with major customers. This could create more growth opportunities in storage and computing markets over time. Robotics and physical AI are an emerging long-term growth driver. AI adoption in robotics has already started to create commercial opportunities. Recognizing this trend, Monolithic is broadening its exposure to robotics, building automation and portable AI devices.

However, Monolithic operates in a highly competitive analog semiconductor market populated by larger companies such as Analog Devices, Inc. (ADI) and Texas Instruments. These companies have broader product portfolios and deeper financial resources. Analog Devices boasts a strong presence in Industrial, Automotive and Communications markets. The company is set to acquire Empower Semiconductor for $1.5 billion in cash. Analog Devices is aiming to expand its AI-focused high-density power management solutions for hyperscalers and data centers. Such initiatives may impact Monolithic’s initiatives in the power management space.

Semiconductor manufacturing also requires substantial capital investments to drive innovation and maintain a competitive edge in the long term. This pressure on profitability is particularly high during periods of industry downturns.

Monolithic derives a substantial portion of revenues from Asia, making results sensitive to foreign exchange movements, tariffs and changing trade policies. Management continues to highlight geopolitical and macroeconomic uncertainty, particularly surrounding export controls and evolving global tariff policies.

How Do the Estimates Compare for QCOM & MPWR?

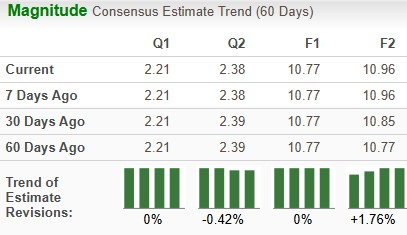

The Zacks Consensus Estimate for Monolithic’s 2026 sales and EPS indicates year-over-year growth of 32.78% and 35.3%, respectively. The EPS estimates for 2026 have remained unchanged over the past 60 days.

Image Source: Zacks Investment Research

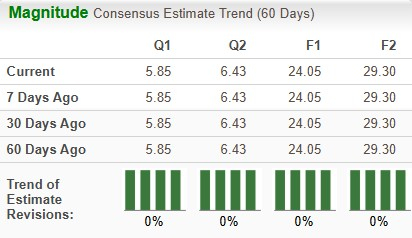

The Zacks Consensus Estimate for Qualcomm’s 2026 sales and EPS implies a year-over-year decline of 3.44% and 10.47%, respectively. The EPS estimates for 2026 have remain unchanged over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of QCOM & MPWR

Over the past year, Monolithic has increased 85.6%, while Qualcomm has increased 20.1%.

Image Source: Zacks Investment Research

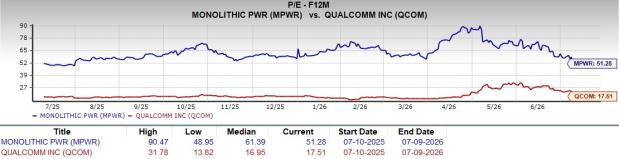

Qualcomm looks more attractive than Monolithic from a valuation standpoint. Going by the price/earnings ratio, QCOM’s shares currently trade at 17.51 forward earnings, significantly lower than 51.28 for Monolithic.

Image Source: Zacks Investment Research

QCOM or MPWR: Which Is a Better Pick?

Both Qualcomm and Monolithic carry a Zacks Rank 3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Qualcomm and Monolithic are taking several steps to strengthen their portfolio and gain from expanding their AI data center portfolio. Monolithic is venturing into high-growth markets such as robotics and physical AI. However, competition remains intense across power management, AI infrastructure and communications applications, where customers often require aggressive pricing and rapid innovation cycles. Qualcomm’s aggressive approach to diversify its revenue base, a comprehensive AI infrastructure roadmap spanning CPUs, inference accelerators and networking bodes well for long-term growth. Owing to these factors, a diverse portfolio and better valuation, Qualcomm is a better investment option at present.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).