Morgan Stanley MS is scheduled to announce second-quarter 2026 earnings on July 15 before market open. The company’s financial results and subsequent management conference call are expected to attract significant attention from analysts and investors seeking insights into how it is navigating the current operating environment.

Morgan Stanley’s first-quarter 2026 performance was impressive, driven by robust trading and deal-making activities. The company’s results in the to-be-reported quarter are likely to have benefited from similar positive factors. The Zacks Consensus Estimate for second-quarter revenues of $19.38 billion suggests 15.4% year-over-year growth.

In the past seven days, the consensus estimate for earnings for the to-be-reported quarter has been revised 4% upward to $2.89. The figure indicates a 35.7% jump from the prior-year quarter.

Estimate Revision Trend

Image Source: Zacks Investment Research

MS has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in each of the trailing four quarters, with the average beat being 17.07%.

Earnings Surprise History

Image Source: Zacks Investment Research

Factors to Influence Morgan Stanley’s Q2 Results

IB Income: After an impressive first-quarter performance, global deal-making activity moderated as geopolitical uncertainty, persistent valuation gaps, slowing economic growth, elevated inflation and interest rates, and a stubbornly high backlog of private equity exits weighed on transaction value. However, strategic buyers remained active, targeting deals that could expand scale, bolster resilience and strengthen supply chain security amid the challenging operating environment.

So, while global mergers and acquisitions (M&As) volume improved year over year, deal value fell as only a handful of big transactions dominated the space. This, along with Morgan Stanley’s position as one of the leading players in the space, is expected to have driven advisory fees in the second quarter. The Zacks Consensus Estimate for advisory fees is pegged at $684.6 million, indicating a year-over-year jump of 34.8%.

The quarter witnessed strong IPO activity and equity issuances. Morgan Stanley’s prominent underwriting role in SpaceX’s mega IPO is likely to have boosted its equity underwriting fees. Further, global bond issuance volume was solid, driven by corporate refinancing and infrastructure builds. So, Morgan Stanley’s equity and fixed income underwriting fees are expected to have increased on a year-over-year basis.

The Zacks Consensus Estimate for equity underwriting fees of $554.4 million suggests year-over-year growth of 10.9%. The consensus estimate for fixed-income underwriting fees is pegged at $704.9 million, indicating a surge of 32.5%. The consensus estimate for total underwriting fees of $1.26 billion implies a jump of 22%.

The Zacks Consensus Estimate for IB income of $2.3 billion indicates a year-over-year jump of 40%.

Trading Revenues: The performance of Morgan Stanley’s trading business (constituting a significant portion of its top line) is expected to have been solid in the second quarter of 2026, supported by increased client activity and market volatility. Trading conditions were shaped by evolving expectations surrounding artificial intelligence, ongoing geopolitical tensions, persistent inflationary pressures and a more hawkish Federal Reserve. These factors contributed to heightened volatility across equities and other asset classes, including commodities, fixed income and foreign exchange.

The Zacks Consensus Estimate for the company’s equity trading revenues is pegged at $4.42 billion, suggesting a rise of 18.7% from the prior-year quarter. The consensus estimate for fixed-income trading revenues of $2.31 billion indicates a gain of 6%.

Net Interest Income (NII): In the to-be-reported quarter, the Fed kept interest rates unchanged, while signaling a hike later in the year because of persistently high inflation. This created a favorable backdrop for Morgan Stanley.

Further, the lending scenario is likely to have improved in the second quarter, which, along with stabilizing funding/deposit costs, is expected to have offered much-needed support. Hence, Morgan Stanley’s NII is likely to have witnessed a decent improvement in the quarter.

The Zacks Consensus Estimate for net interest revenues is pegged at $2.62 billion, suggesting a rise of 11.5% on a year-over-year basis.

For the wealth management segment, management expects NII to rise modestly on a sequential basis.

Expenses: Cost reduction, which has long been Morgan Stanley's primary strategy for remaining profitable, is unlikely to have provided much support in the June-ended quarter. As the company has been investing in franchises, overall costs are likely to have been elevated.

What Our Quantitative Model Unveils for MS

Our proven model predicts an earnings beat for Morgan Stanley this time around. This is because it has the right combination of the two key ingredients — a positive Earnings ESP and a Zacks Rank #3 (Hold) or better.

The Earnings ESP for Morgan Stanley is +0.86%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

MS currently carries a Zacks Rank #3. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

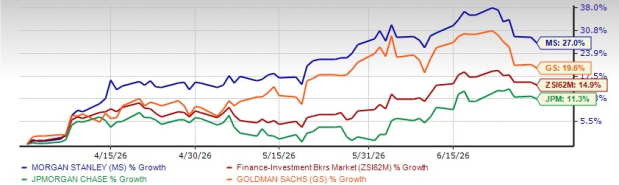

Morgan Stanley’s Price Performance

In the second quarter, Morgan Stanley’s share performance was impressive as the operating backdrop turned favorable. The stock fared better than the industry as well as its peers, Goldman Sachs GS and JPMorgan JPM.

2Q26 Price Performance

Image Source: Zacks Investment Research

Goldman and JPMorgan are scheduled to announce second-quarter 2026 numbers tomorrow.

Over the past seven days, the Zacks Consensus Estimate for Goldman’s second-quarter 2026 earnings has been revised north to $14.47. The consensus estimate for JPMorgan’s second quarter 2026 earnings has been revised upward to $5.59 over the past week. At present, both GS and JPM carry a Zacks Rank #2 (Buy).

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Morgan Stanley (MS): Free Stock Analysis Report

The Goldman Sachs Group, Inc. (GS): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).