Citigroup Inc. C is slated to report second-quarter 2026 results on July 14, 2026, before market open.

In the first quarter of 2026, Citigroup witnessed increases in net interest income (NII) and non-interest revenues. The company also registered a solid increase in Investment Banking (IB) revenues.

This globally diversified financial service holding company is expected to have registered bottom and top-line increases in the to-be-reported quarter.

The Zacks Consensus Estimate for second-quarter revenues is pegged at $23.68 billion, indicating a 9.3% year-over-year increase.

The consensus estimate for earnings for the to-be-reported quarter has been revised upward to $2.72 over the past seven days. The figure indicates a 38.8% rise from the prior-year quarter’s actual.

Estimate Revision Trend

Image Source: Zacks Investment Research

The company also has an impressive earnings surprise history. Its earnings outpaced the Zacks Consensus Estimate in the trailing four quarters, the average surprise being 16.16%.

Earnings Surprise History

Image Source: Zacks Investment Research

Factors to Influence Citigroup’s Q2 Results

NII: In the second quarter of 2026, the Federal Reserve kept interest rates unchanged and signaled a hike later this year amid persistently higher inflation. This has resulted in a favorable backdrop for Citigroup.

Building on the first quarter’s momentum, lending activity was decent in the to-be-reported quarter. Per the Fed’s latest data, the demand for commercial and industrial loans, and consumer credit remained healthy in the second quarter of 2026, while real estate loan demand was relatively modest. Hence, improving loan demand, coupled with easing deposit and funding costs, is expected to have provided meaningful support to C’s NII.

The Zacks Consensus Estimate for NII is pinned at $16.2 billion, suggesting a 6.5% year-over-year rise.

Fee Income: Following a record-setting first quarter, global merger and acquisition (M&A) activity moderated during the second quarter as geopolitical uncertainty, persistent valuation gaps, slowing economic growth, elevated inflation and interest rates, and a sizable backlog of private equity exits weighed on deal-making. Despite these headwinds, strategic acquirers continued to pursue transactions focused on expanding scale, enhancing operational resilience and strengthening supply-chain security.

As a result, while global M&A volumes increased year over year, overall deal value declined, with only a limited number of large transactions driving activity. Even so, these trends are expected to have supported Citigroup’s IB revenues during the quarter. Management has guided for second-quarter 2026 IB fees to increase year over year in the mid-teens, supported by stronger equity capital market activity, including initial public offerings and follow-on offerings.

Citigroup also expects second-quarter 2026 trading revenues to grow in the high single digit to low double digits from the prior-year period’s actual. Although client activity and market volatility eased compared with the exceptionally strong first quarter, both remained elevated during the second quarter. Trading conditions were shaped by evolving expectations around artificial intelligence, ongoing geopolitical tensions, persistent inflation concerns and a more hawkish Federal Reserve.

Further, elevated volatility across equities, commodities, fixed income and foreign exchange markets is expected to have supported the company's markets revenues. The Zacks Consensus Estimate for markets revenues is $6.28 billion, implying a 6.8% year-over-year increase.

The Zacks Consensus Estimate for income from commissions and fees is pinned at $2.76 billion, which indicates a nearly 1% year-over-year rise.

The Zacks Consensus Estimate for income from principal transactions is pegged at $3.1 billion, which suggests an 8% decline from the prior-year quarter’s actual.

The Zacks Consensus Estimate for administration and other fiduciary fees is pinned at $1.18 billion, which implies a year-over-year increase of 31.7%.

The Zacks Consensus Estimate for total non-interest income for the second quarter of 2026 is pegged at $7.58 billion, which suggests a 16.7% rise from the prior-year quarter’s actual.

Expenses: Though Citigroup is focused on lowering expenses through organizational simplification, cost reductions and productivity savings, the bank’s increased investments in business transformation efforts, technological advancements and higher volume-related expenses are likely to have kept the expense base elevated in the second quarter of 2026.

Asset Quality: After setting aside a decent amount for potential loan losses in the first quarter, Citigroup is likely to have maintained a similar provisioning trend in the quarter under review, given persistent inflation and expectations of a rate hike later this year.

The Zacks Consensus Estimate for non-accrual loans is pegged at $3.72 billion, indicating a jump of 11.2% from the prior year’s reported figure.

What Our Model Unveils for C

Our proven model does conclusively predict an earnings beat for Citigroup this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is exactly the case here, as you can see below.

Citigroup has an Earnings ESP of +0.64%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Citigroup’s Price Performance & Valuation

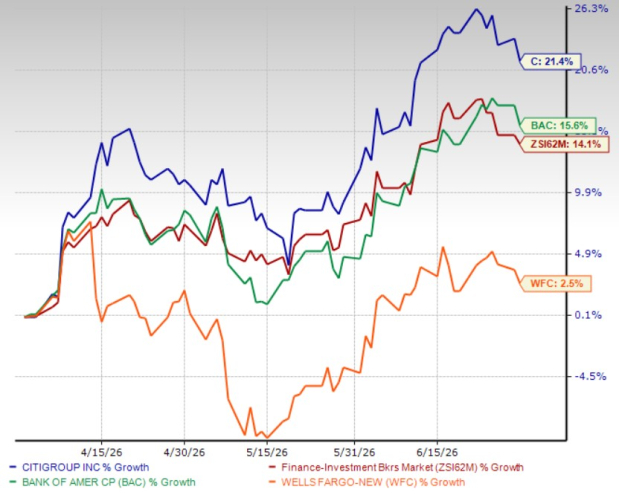

In the second quarter of 2026, C shares gained 21.4% compared with the industry’s rise of 14.1%. Shares of its peer Bank of America BAC rose 15.6% and Wells Fargo WFC gained 2.5% in the same period.

Price Performance

Image Source: Zacks Investment Research

Both Wells Fargo and Bank of America are slated to announce quarterly numbers on the same day as Citigroup.

Now, let us look at the value that Citigroup offers investors at the current levels.

Currently, C is trading at 11.95X forward 12-month earnings, below the industry’s forward price/earnings (P/E) multiple of 14.59X. The company’s valuation looks inexpensive compared with the industry average.

Price-to-Earnings F12M

Image Source: Zacks Investment Research

Citigroup’s stock is also trading at a discount compared with Bank of America’s P/E of 12.32X and Wells Fargo's P/E of 11.69X.

Evaluating Citigroup Stock Ahead of Q2 Earnings

Citigroup continues to benefit from its multi-year strategy aimed at simplifying operations and sharpening its focus on core businesses. In June 2026, the company completed the sale of its Polish consumer banking unit to VeloBank, marking the final major divestiture of its international consumer franchises. This excludes the largely completed wind-downs and the ongoing Banamex divestiture.

These strategic moves are expected to free up capital and enable Citigroup to invest more aggressively in higher-return areas such as wealth management and investment banking, thereby supporting fee income growth. Backed by these initiatives, management projects revenues to see a 4-5% compound annual growth rate through 2026.

From a profitability standpoint, Citigroup is targeting a return on tangible common equity (RoTCE) of 10-11% in 2026. The bank expects this to improve to 11-13% in 2027 and 2028 (excluding notable items), with a longer-term goal of reaching 14-15% between 2029 and 2031. This trajectory reflects management’s confidence that the firm’s streamlined structure will enhance efficiency and better translate revenue growth into shareholder value.

Cost optimization remains a key pillar of the transformation strategy. Citigroup plans to eliminate 20,000 roles by 2026 and has already reduced its workforce by more than 10,000 employees. Alongside headcount reductions, the company is focusing on process simplification, automation and the increasing use of artificial intelligence to reduce manual intervention and improve operational efficiency.

Shareholder returns are also a bright spot. Following the successful completion of the 2026 Federal Reserve stress test, Citigroup intends to increase its quarterly dividend 12% to 67 cents per share (from 60 cents), starting in the third quarter of 2026, subject to board approval. The company has launched a $30-billion multi-year share repurchase program, underscoring its commitment to returning capital to investors.

Despite these positives, near-term challenges remain. The ongoing restructuring efforts are likely to keep expenses elevated in the short run, while concerns around asset quality persist amid an uncertain macroeconomic backdrop.

Given this mixed outlook, investors may prefer to wait for the upcoming quarterly results before initiating new positions, as the earnings release could provide clearer visibility and potentially a more attractive entry point. Management’s commentary on geopolitical risks, market volatility and credit trends will be particularly important. However, existing shareholders may consider holding their positions, as Citigroup’s long-term fundamentals remain intact despite near-term headwinds.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

Wells Fargo & Company (WFC): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).