Costco Wholesale Corporation's COST valuation remains among the highest in the retail sector, leaving little room for operational missteps. That makes monthly sales updates closely monitored by investors. June's sales results once again highlighted resilient consumer demand, decent comparable sales growth and strong digital momentum, but are these trends enough to support the stock's premium multiple going forward?

A Closer Look at Costco's June Sales

For a retailer trading at a premium multiple, the quality and consistency of growth matter as much as the pace. Costco’s June report certainly provided encouraging evidence. Net sales increased 10.6% year over year to $29.24 billion during the five weeks ended July 5, 2026. Comparable sales rose 8.8% companywide, while adjusted comparable sales, excluding gasoline price and foreign exchange impacts, advanced 7%. Those figures point to broad-based demand rather than growth driven solely by external factors.

Although June comparable sales remained strong, they moderated from the 12.5% and 11.6% growth recorded in May and April, respectively. The sequential slowdown does not undermine Costco's performance, but it highlights the broad-based growth needed to support its premium valuation.

Digital performance remained another bright spot. Costco's digitally enabled comparable sales climbed 20.9% on a reported basis and 21.5% after adjusting for fuel and currency effects. Sustained online growth of this magnitude complements warehouse traffic and reinforces the company's ability to expand sales beyond its physical footprint without compromising its value proposition.

Do Costco’s Latest Metrics Justify Its Premium Valuation?

Costco trades at a forward 12-month price-to-earnings ratio of 41.30, well above the industry’s ratio of 30.05. The premium reflects investors' confidence in the company's membership-driven business model, recurring fee income, resilient sales growth and disciplined execution. Even so, the multiple remains below its 12-month median of 46.32, indicating that valuation has moderated from historical levels.

The premium is even more evident when compared with mass-merchandise retailers. Costco continues to command a meaningful premium over Dollar General Corporation DG and Target Corporation TGT. Costco is trading at a premium to Dollar General (forward 12-month P/E of 15.53) and Target (15.73).

Image Source: Zacks Investment Research

Why Has Costco Stock Pulled Back?

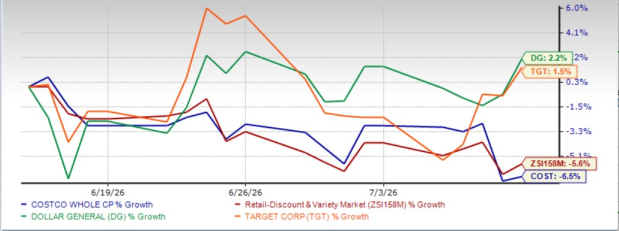

Despite another month of resilient sales growth, Costco shares have dropped 6.5% over the past month, modestly underperforming the industry's 5.6% decline. The softness may be tied to the stock’s rich valuation rather than to any deterioration in underlying fundamentals. The moderation in June’s comparable sales growth from the stronger gains recorded in May and April may have also tempered investor enthusiasm.

Over the same period, shares of Dollar General have gained 2.2%, while Target has advanced 1.5%.

Image Source: Zacks Investment Research

How Are Costco's Earnings Estimates Trending?

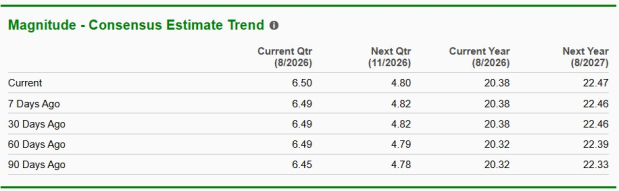

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 9.6% and 13.3%, respectively. For the next fiscal year, the consensus estimate indicates a 7.9% rise in sales and 10.2% growth in earnings.

The consensus estimate for earnings per share for the current and next fiscal year has increased by 6 cents and 8 cents to $20.38 and $22.47, respectively, over the past 60 days. The upward revisions suggest that analysts remain confident in Costco's ability to deliver steady earnings growth.

Image Source: Zacks Investment Research

Can Costco Continue to Command a Premium?

Costco’s June sales once again reinforced the strength of its membership-driven business model, supported by healthy comparable sales growth and continued digital momentum. Improving earnings estimates further lend support. However, given its significant premium to the industry, Costco will need to sustain strong execution to justify its valuation and drive the stock higher.

Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Target Corporation (TGT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).