Lam Research Corporation LRCX is slated to report its fourth-quarter fiscal 2026 results in late July, and investors must be wondering if the company will reach its record revenue target of $6.6 billion. We believe that the ongoing boom in artificial intelligence (AI) chips could help Lam Research achieve that goal. Demand for advanced semiconductor equipment continues to rise as chipmakers expand capacity for AI processors, high-bandwidth memory (HBM) and next-generation logic devices.

Lam Research delivered strong momentum in the third quarter of fiscal 2026. Revenues increased 24% year over year to a record $5.84 billion, while systems revenues climbed to $3.73 billion. Non-GAAP earnings per share jumped 41% and reached a record $1.47, while non-GAAP gross margin improved 90 basis points to 49.9%, reflecting a favorable product mix and operational execution. These results provide a solid foundation for another quarter of growth.

AI is becoming LRCX’s biggest growth engine. The company is benefiting from rising investments in advanced DRAM, HBM and leading-edge foundry technologies, all of which require Lam Research’s etch and deposition equipment. Management also expects advanced packaging revenues to grow more than 50% in calendar year 2026 as AI processors become more complex and require sophisticated chip integration technologies.

Industry conditions remain favorable. Lam Research estimates global wafer fabrication equipment spending of approximately $140 billion in calendar year 2026, reflecting stronger AI-related investments across memory and logic markets. The company also expects industry growth to continue into 2027.

If AI infrastructure spending remains robust and customers continue expanding advanced chip production, Lam Research appears well-positioned to achieve its record fourth-quarter sales target and sustain its strong growth momentum. The Zacks Consensus Estimate for fourth-quarter fiscal 2026 revenues is currently pegged at $6.67 billion, higher than the midpoint of management’s guidance range and indicating a year-over-year increase of more than 29%.

Lam Research’s Rivals Also Benefit From AI Chip Demand

LRCX’s main competitors, Applied Materials, Inc. AMAT and KLA Corporation KLAC, are also benefiting from the AI chip boom. Both companies have broad exposure to advanced semiconductor manufacturing and are seeing strong demand from AI-related investments.

Applied Materials is Lam Research’s closest rival in wafer fabrication equipment. The company generated revenues of $7.91 billion in the second quarter of fiscal 2026, with its Semiconductor Systems segment contributing the majority of sales. Applied Materials reported record DRAM revenue and continues to benefit from growing demand for advanced logic, HBM and advanced packaging solutions used in AI servers. Its broad product portfolio positions it to capture a significant share of rising semiconductor capital spending.

KLA Corporation competes through inspection and process control equipment, which are essential for manufacturing advanced AI chips. The company’s third-quarter fiscal 2026 revenues increased 11.5% year over year to $3.42 billion as it continues to benefit from increasing process complexity at leading-edge nodes. As AI processors and HBM stacks require tighter quality control and higher production yields, KLAC's inspection tools are becoming increasingly important.

For Lam Research, sustaining record quarterly revenues will depend on maintaining its leadership in etch and deposition technologies while competing effectively with Applied Materials and KLA Corporation across the rapidly expanding AI semiconductor ecosystem.

LRCX’s Share Price Performance, Valuation and Estimates

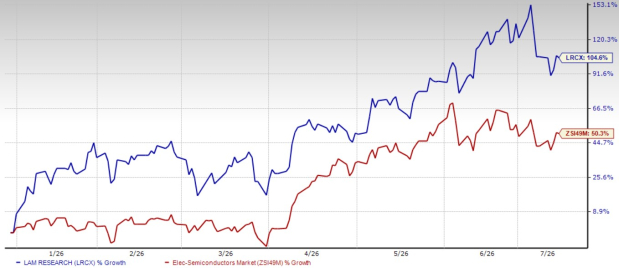

Shares of Lam Research have surged 104.6% year to date compared with the Zacks Electronics – Semiconductors industry’s rise of 50.3%.

Lam Research YTD Price Return Performance

Image Source: Zacks Investment Research

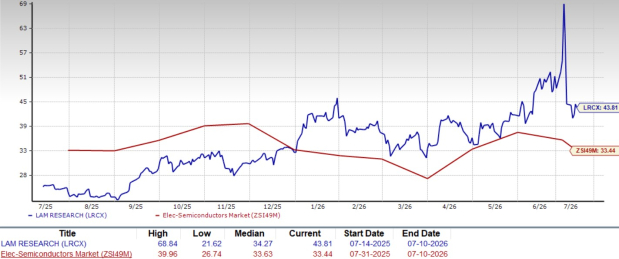

From a valuation standpoint, Lam Research trades at a forward price-to-earnings ratio of 43.81, significantly higher than the industry’s average of 33.34.

Lam Research Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Lam Research’s fiscal 2026 and 2027 earnings implies a year-over-year increase of approximately 37.2% and 39.6%, respectively. Estimates for fiscal 2026 have been revised upward over the past 30 days, while estimates for fiscal 2027 have been raised northward over the past seven days.

Image Source: Zacks Investment Research

Lam Research currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lam Research Corporation (LRCX): Free Stock Analysis Report

KLA Corporation (KLAC): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).