Bank of America BAC is scheduled to announce second-quarter 2026 results on July 14, before the opening bell.

The company began 2026 on a positive note, with robust trading and investment banking (IB) performance driving first-quarter results. BAC’s upcoming quarterly results are also expected to be solid despite rate uncertainty and lingering geopolitical headwinds. The Zacks Consensus Estimate for the company’s second-quarter revenues is pegged at $30.62 billion, indicating 15.7% year-over-year growth.

In the past seven days, the consensus estimate for earnings for the to-be-reported quarter has been revised higher to $1.13. The figure suggests a 27% rise from the prior-year quarter, as higher net interest income (NII) and solid capital markets business are likely to have supported BAC’s bottom-line growth.

Estimate Revision Trend

Image Source: Zacks Investment Research

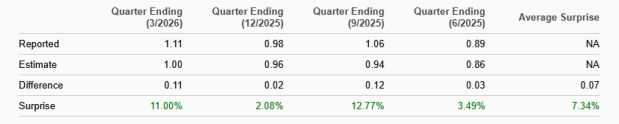

Bank of America has an impressive earnings surprise history. The company’s earnings outpaced the Zacks Consensus Estimate in the trailing four quarters, the average beat being 7.3%.

Earnings Surprise History

Image Source: Zacks Investment Research

Key Drivers of Bank of America’s Q2 Performance

NII: The interest rate environment remained supportive for Bank of America’s NII in the second quarter. The Federal Reserve paused its rate-cutting cycle and has signaled the possibility of a rate hike later this year as inflation remains stubbornly above its target. Sustained healthy lending yields have been favorable for banks, including BAC.

Building on the momentum seen in the first quarter, Bank of America’s lending activity is expected to have strengthened further in the to-be-reported quarter. According to the Federal Reserve’s latest data, the demand for commercial and industrial loans, and consumer credit remained resilient in the second quarter, while the demand for real estate loans was comparatively modest.

Thus, robust loan growth, combined with easing deposit and funding costs, is likely to have supported BAC’s NII growth. The Zacks Consensus Estimate for the company’s second-quarter tax-equivalent NII is $16.24 billion, indicating a 9.6% increase from the year-ago quarter’s actual.

IB Fees: After a record-setting first quarter, global deal-making activity moderated amid geopolitical uncertainty, persistent valuation gaps, slowing economic growth, elevated inflation and interest rates, and a stubbornly high backlog of private equity exits. Nevertheless, strategic buyers remained active, pursuing transactions aimed at enhancing scale, strengthening resilience and improving supply-chain security in response to the challenging operating environment.

Hence, while deal value declined in the second quarter (as only a handful of big transactions dominated the space), the volume of global mergers and acquisitions (M&As) improved year over year. This is expected to have supported Bank of America’s advisory fees.

Then, the second quarter saw strong IPO activity and equity issuances, including a blockbuster mega offering from SpaceX and Google parent Alphabet Inc. Likewise, global bond issuance volume was solid, driven by corporate refinancing and infrastructure builds. Thus, growth in BAC’s underwriting fees (accounting for almost 40% of total IB fees) is expected to have been strong in the to-be-reported quarter.

The Zacks Consensus Estimate for BAC’s total IB income of $1.96 billion for the second quarter indicates a rise of 37% from the prior-year quarter’s actual.

Trading Income: Client activity and market volatility were strong in the second quarter, though both were less pronounced compared with the preceding quarter. Trading conditions were influenced by shifting expectations around artificial intelligence, persistent geopolitical tensions, lingering inflation concerns and a more hawkish stance from the Fed. Volatility was high in equity markets and other asset classes, including commodities, bonds and foreign exchange. Thus, BAC is likely to have recorded a strong trading performance this time as well.

The Zacks Consensus Estimate for market making and similar activities of $3.93 billion for the to-be-reported quarter suggests a 24.5% rise on a year-over-year basis. Management anticipates trading revenues in the second quarter to increase 15% year over year.

Expenses: While Bank of America managed expenses prudently in the past, expansion into new markets by opening financial centers and efforts to digitize operations and upgrade existing financial centers are expected to have kept non-interest expenses elevated in the to-be-reported quarter.

Asset Quality: After setting aside a modest amount for potential loan losses in the first quarter, Bank of America is likely to have maintained a similar provisioning trend in the quarter under review. Although the period began with concerns related to the Middle East conflict, oil price volatility and persistent inflation, the subsequent ceasefire helped drive a meaningful decline in crude prices. This, coupled with resilient economic growth and broadly stable credit conditions, is expected to have supported a decline in the company’s provision for credit losses.

The Zacks Consensus Estimate for non-performing loans and leases of $6.68 billion implies an 11.6% increase from the prior-year quarter.

What Our Model Reveals About BAC’s Q2 Earnings

Per our proven model, the chances of an earnings beat for BAC are high this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is the case here, as you can see below.

Bank of America has an Earnings ESP of +0.64%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

BAC’s Price Performance & Valuation Analysis

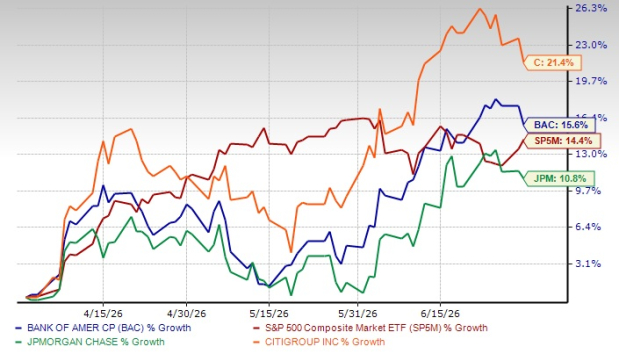

In the second quarter, BAC shares gained 15.6%, outperforming the S&P 500 Index. In the same time frame, shares of two of its close peers JPMorgan JPM and Citigroup C rallied 10.8% and 21.4%, respectively.

2Q26 Price Performance

Image Source: Zacks Investment Research

Both JPMorgan and Citigroup are slated to announce quarterly numbers on the same day as BAC.

Let us check out the value Bank of America offers investors at current levels. BAC stock is trading at a 12-month trailing price-to-tangible book (P/TB) of 2.14X. This is below the industry’s 3.38X. This shows that the stock is relatively inexpensive.

Price-to-Tangible Book (TTM)

Image Source: Zacks Investment Research

The BAC stock is trading at a discount compared with JPMorgan, which has a P/TB of 3.27X. However, Citigroup has a P/TB of 1.47X, making it inexpensive compared with Bank of America.

How to Approach BAC Shares Before Q2 Earnings?

Bank of America is well-positioned to continue to benefit from its vast scale, extensive capital markets operations and international footprint (which will drive significant fee income).

Given the industry-wide solid lending scenario, along with stabilizing funding costs and the possibility of a rate hike later this year, the company’s NII growth is expected to be robust. Management expects NII (FTE basis) to grow in the upper end of 6-8% in 2026.

BAC’s aggressive branch expansion across the United States as part of a broader strategy to solidify customer relationships and tap into new markets will further drive interest income growth over time. This will also help capitalize on cross-selling opportunities.

However, while Bank of America’s outlook remains constructive, investors may want to avoid rushing to buy the stock. Instead, they should closely watch management’s commentary on how geopolitical risk and market volatility affect the company’s performance and how the firm plans to navigate the current environment. Any revisions to BAC’s 2026 guidance for NII, IB, non-interest expenses and asset quality will be especially important, given the recent macro developments. Broader macroeconomic and policy trends that could materially shape the company’s performance trajectory should also be carefully considered.

Existing shareholders may hold BAC stock, given its strong fundamentals and proven resilience. Potential investors should carefully weigh these factors and assess their risk tolerance before initiating new positions.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

Citigroup Inc. (C): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).