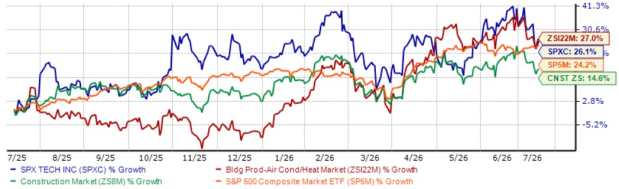

SPX Technologies, Inc. SPXC has delivered a strong share price performance, reflecting solid execution, resilient demand across its key end markets and growing confidence in its long-term growth strategy. Momentum in its HVAC and Detection & Measurement businesses, accelerating demand for data center cooling solutions and disciplined acquisitions have strengthened the company's growth outlook. SPXC stock has climbed 26.1% over the past year, broadly matching the Zacks Building Products - Air Conditioner and Heating industry’s 27% rise while outperforming the Construction sector’s 14.6% gain and the S&P 500 Index’s 24.2% increase.

The outlook remains encouraging. Management raised its full-year guidance after a stronger-than-expected first quarter of 2026, citing robust execution, sustained demand across key markets and additional data center-related volumes expected in the second half of 2026. Continued investments in manufacturing capacity, product innovation and strategic acquisitions should further strengthen SPX Technologies' competitive position.

SPXC’s 1-Year Price Performance

Image Source: Zacks Investment Research

Over the past year, SPX Technologies has substantially outperformed several industry peers. While Carrier Global Corporation CARR and Pentair plc PNR posted declines of 9.5% and 28.7%, respectively, Trane Technologies plc TT gained 9.2%.

SPXC's Data Center Strategy Continues to Drive Long-Term Growth

SPX Technologies continues to benefit from one of the strongest structural growth trends in industrial markets: data center infrastructure. Management noted that demand for its cooling systems and custom air-handling solutions remains exceptionally strong, prompting the company to increase its 2026 data center growth outlook from approximately 50% to 70%. SPXC also emphasized that demand continues to accelerate, supported by increasing activity from hyperscale and colocation customers.

To support this opportunity, SPX Technologies is expanding production capacity across multiple facilities. New manufacturing lines at its Tennessee and Kansas plants have already begun production, while the Alabama expansion remains on schedule to add additional assembly and manufacturing capacity through 2027. Management believes these investments, together with strong customer visibility and a diversified customer base, position the company for sustained growth beyond 2026.

SPXC's Operational Execution Continues to Support Profit Growth

SPX Technologies continues to execute well across both operating segments despite ongoing investments in capacity expansion. Consolidated segment income rose 22% year over year to $135 million, while segment margin expanded 100 basis points to 23.9%, supported by higher volumes, a favorable product mix and increased software revenues within Detection & Measurement.

HVAC segment’s income increased 20% to $88.6 million, benefiting from organic growth and acquisition contributions. Segment margin declined 40 basis points to 22.5%, mainly due to planned start-up costs associated with new production capacity. Management expects most of the estimated $8-$9 million in start-up expenses to be incurred during the first half of 2026. As the new facilities ramp up, operating leverage is expected to improve and support stronger profitability over time.

The company's disciplined acquisition strategy also continues to enhance its growth profile. Recent additions such as Thermolec and Crawford's commercial air-handling business expand SPX Technologies' HVAC capabilities, while the divestiture of Crawford United's non-core industrial and transportation businesses sharpens management's focus on higher-growth markets.

SPXC's Financial Strength Supports Future Growth

SPX Technologies maintains a healthy balance sheet that provides ample flexibility to invest in organic growth and pursue strategic acquisitions. The company ended the first quarter with approximately $158 million in cash and a leverage ratio of roughly 0.9x, well below its long-term target range. This financial strength provides significant capacity to pursue additional value-enhancing acquisitions while continuing to invest in manufacturing expansion and innovation.

The company also continues to generate positive operating cash flow while actively reshaping its portfolio. During the quarter, SPX Technologies completed the divestiture of Crawford United's non-core industrial and transportation businesses, allowing management to sharpen its focus on higher-growth HVAC and Detection & Measurement markets. Combined with a robust acquisition pipeline and raised full-year guidance, the balance sheet positions SPXC to continue executing its long-term growth strategy.

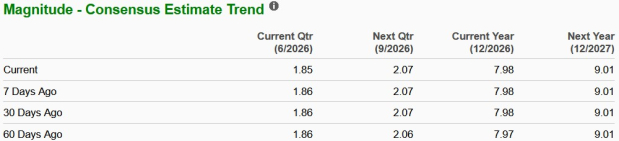

Earnings Estimate Revision of SPXC Stock

SPXC’s earnings outlook has improved over the past 60 days, with the Zacks Consensus Estimate for 2026 rising to $7.98 per share. The consensus estimate for 2027 has remained unchanged over the same period, as shown below. The current projections imply earnings growth of 18.1% in 2026, followed by an additional 12.9% increase in 2027.

Image Source: Zacks Investment Research

SPXC's earnings growth outlook also compares favorably with its peers. Carrier Global is expected to grow earnings by 7.7% this year, while Pentair and Trane Technologies are projected to deliver growth of 8.7% and 13.6%, respectively.

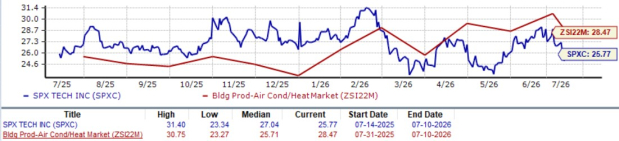

SPXC Stock Trades at a Discount

SPX Technologies trades at a forward 12-month P/E ratio of 25.77X, below the industry average. The valuation reflects investor confidence in the company's disciplined execution, expanding data center opportunity, resilient demand across key end markets and continued investments in manufacturing capacity, product innovation and strategic acquisitions. These initiatives are expected to support long-term earnings growth.

However, following the stock's strong run, execution remains critical. Delays in ramping new manufacturing capacity, slower-than-expected data center demand, integration challenges related to recent acquisitions or a greater-than-expected impact from tariffs could pressure margins and weigh on investor sentiment.

SPXC P/E Ratio (Forward 12 Months) Vs Industry

Image Source: Zacks Investment Research

Among peers, Carrier Global trades at a forward 12-month P/E multiple of 23.27X, while Pentair trades at 13.57X. Trane Technologies carries a higher valuation of 30.06X on the same basis. SPXC therefore trades at a premium to Carrier and Pentair but at a discount to Trane Technologies, placing it within the broader peer valuation range.

Is SPXC Stock Still a Buy After Its Strong Run?

SPX Technologies remains well positioned to benefit from structural growth trends across data centers, HVAC and Detection & Measurement markets. The company continues to execute its value creation strategy through capacity expansion, product innovation and disciplined acquisitions, while its raised guidance and robust backlog underscore confidence in long-term growth. These initiatives, combined with resilient demand across key end markets, should support sustained earnings growth over time.

SPXC also maintains financial flexibility to invest in organic expansion and pursue strategic acquisitions. However, risks remain from delays in ramping new manufacturing capacity, slower-than-expected data center demand, acquisition integration challenges and tariff-related pressures. While the stock trades at a discount to the broader peer group, sustained execution will be important to justify its valuation. Encouragingly, rising earnings estimates suggest analysts remain confident in the company's growth prospects.

SPXC stock currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

SPX Technologies, Inc. (SPXC): Free Stock Analysis Report

Pentair plc (PNR): Free Stock Analysis Report

Trane Technologies plc (TT): Free Stock Analysis Report

Carrier Global Corporation (CARR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).