ServiceNow NOW and Atlassian TEAM are two of the most important enterprise cloud software companies, helping large organizations modernize operations, automate workflows and manage critical business processes.

While both benefit from long-term digital transformation trends, their business momentum and execution profiles differ meaningfully. For investors trying to choose between these two software leaders, a closer look at their fundamentals, growth outlook and risks helps determine which stock currently offers a stronger investment case.

The Case for ServiceNow Stock

ServiceNow has been benefiting from the rising adoption of its workflows by enterprises undergoing digital transformation. The company expects to achieve $1.5 billion in AI revenues in 2026 on the back of rising adoption of ServiceNow's AI products, such as Now Assist, across its customer base, where customers are deploying AI faster and on a much larger scale.

Deals including three or more Now Assist products grew nearly 70% year over year in the first quarter, suggesting that customers are expanding AI usage across multiple workflows rather than testing a single AI feature. This bodes well for ServiceNow's prospects as customers are increasingly moving from AI pilots to full production deployments across their organizations and are now investing in AI across multiple business functions.

Now Assist is also helping ServiceNow grow other AI products. The company stated that the adoption of Now Assist is driving demand for AI Control Tower and RaptorDB Pro. In the first quarter, AI Control Tower’s average deal sizes more than doubled sequentially, while RaptorDB Pro deal volume increased 80% year over year. Rising customer adoption and higher AI revenue expectations are positioning Now Assist to become an important driver of ServiceNow's AI growth strategy.

However, ServiceNow is integrating several acquisitions at the same time, including Moveworks, Armis, Veza and Pyramid Analytics. As a result of its back-to-back acquisitions, ServiceNow will need to integrate the acquired products, employees, technologies and sales teams into its existing business. As a result, the company will incur higher costs. These costs are expected to hurt the company's profitability before the benefits of synergies from acquisitions are fully realized.

For instance, the Armis acquisition is also expected to put pressure on profitability in 2026. Management expects Armis to reduce 2026 subscription gross margin by 25 basis points, operating margin by 75 basis points and free cash flow margin by 200 basis points. For the second quarter of 2026, Armis is expected to reduce its operating margin by 125 basis points. If customer adoption is slower than expected, the revenue contribution from these businesses could take longer to materialize.

The Case for Atlassian Stock

Atlassian's cloud business remained a key growth driver in the third quarter of fiscal 2026. Cloud revenues increased 29% year over year to more than $1.1 billion, helping total revenues grow 32% to $1.8 billion. The strong performance was driven by higher customer adoption, cross-selling and continued demand for the company's cloud-based products.

AI is playing an important role in this growth. Management said customers using its AI product, Rovo, are growing their annual recurring revenues (ARR) at about twice the rate of customers that do not use Rovo. Rovo's credit usage is growing more than 20% month over month, while millions of users are actively using the platform. In addition, more customers are adopting Teamwork Collection, which combines Jira, Confluence, Loom and Rovo into one offering. This bundle is helping Atlassian sell more products to existing customers and increase cloud spending.

The company's cloud business is benefiting from steady enterprise adoption. Management said cloud migrations from the Data Center remain on track and are expected to contribute mid- to high-single-digit cloud growth over time. TEAM's seat expansion remains healthy, while Net Revenue Retention stayed above 120% in the third quarter, as customers continue to adopt more products and expand their spending across the Atlassian platform.

The above-mentioned factors show that Atlassian's cloud business appears well positioned for continued growth. Rising AI adoption, higher cross-selling through Teamwork Collection and ongoing cloud migrations are helping the company expand its customer relationships. If these trends continue, the cloud business is likely to remain Atlassian's biggest growth driver in the coming quarters.

How do Earnings Estimates Compare for NOW & TEAM?

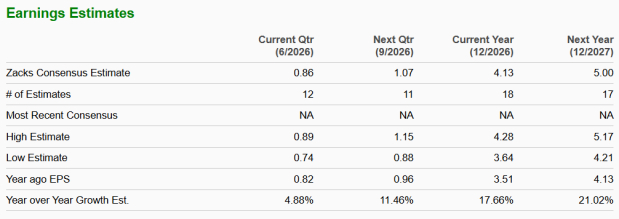

The Zacks Consensus Estimate for NOW’s 2026 EPS is pegged at $4.13, unchanged over the past 30 days, indicating year-over-year growth of 17.7%.

Image Source: Zacks Investment Research

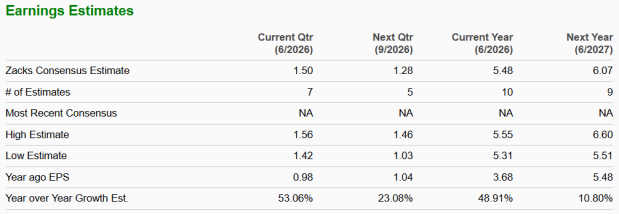

The Zacks Consensus Estimate for TEAM’s fiscal 2026 EPS is pinned at $5.48, unchanged over the past 30 days, indicating year-over-year growth of 48.9%.

Image Source: Zacks Investment Research

NOW vs. TEAM: Price Performance and Valuation

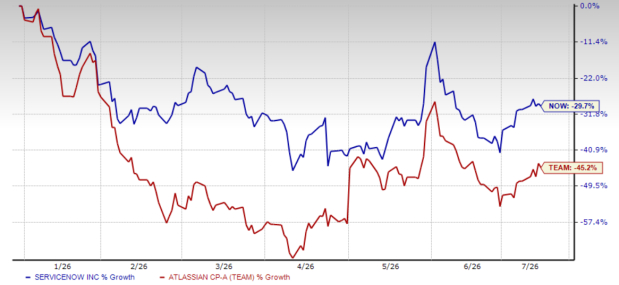

Year to date, shares of NOW and TEAM have plunged 29.7% and 45.2%, respectively.

NOW Vs. TEAM: YTD Price Return Performance

Image Source: Zacks Investment Research

Currently, TEAM is trading at a forward sales multiple of 3.06X, lower than NOW’s forward sales multiple of 6.26X. TEAM’s reasonable valuation makes it more attractive for investors looking for value and stability.

NOW vs. TEAM: Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Conclusion: TEAM Has an Edge Over NOW

Both ServiceNow and Atlassian are well-positioned to benefit from the AI wave. However, ServiceNow faces near-term risks, such as dilutive impact on margins as a result of its back-to-back acquisitions, which could hurt the company’s prospects in the near term.

In contrast, Atlassian shows steadier execution, where the company is witnessing strong momentum in its cloud business, driven by robust adoption of its AI products. TEAM’s reasonable valuation offers some downside protection as well, giving TEAM a clear edge over NOW.

Currently, NOW and TEAM carry a Zacks Rank #3 (Hold) each at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

ServiceNow, Inc. (NOW): Free Stock Analysis Report

Atlassian Corporation PLC (TEAM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).