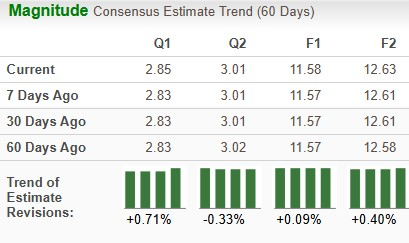

Johnson & Johnson JNJ will begin the earnings season for the drug & biotech sector when it reports its second-quarter 2026 results on July 15. The Zacks Consensus Estimate for second-quarter sales and earnings is pegged at $25.18 billion and $2.85 per share, respectively.

The Zacks Consensus Estimate for 2026 earnings has risen from $11.57 per share to $11.58 over the past 60 days, while that for 2027 earnings has gone up from $12.58 per share to $12.63 over the same time frame.

JNJ Estimate Movement

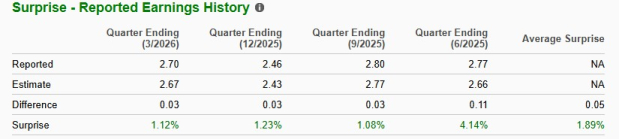

JNJ’s Earnings Surprise History

The healthcare bellwether’s performance has been pretty impressive, with the company exceeding earnings expectations in each of the trailing four quarters. It delivered a four-quarter earnings surprise of 1.89%, on average. In the last reported quarter, the company delivered an earnings surprise of 1.12%.

JNJ’s EPS Surprise

J&J has an Earnings ESP of +2.08% and a Zacks Rank #3 (Hold), indicating a likely positive surprise. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Per our proven model, companies with the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), #2 (Buy) or #3 have a good chance of delivering an earnings beat. You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors Shaping JNJ’s Upcoming Results

Sales in J&J’s Innovative Medicine segment are expected to have been driven by higher sales of key products such as Darzalex, Tremfya and Erleada due to strong market growth and share gains.

The Zacks Consensus Estimate for Darzalex, Tremfya and Erleada is pegged at $4.16 billion, $1.85 billion and $1.05 billion, respectively.

Other products like Uptravi and Opsumit are likely to have witnessed continued growth. The rapid adoption of new drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato is likely to have contributed to top-line growth. However, sales of Xarelto, Simponi/Simponi Aria and Remicade declined in the first quarter, a trend likely to have continued in the second quarter.

J&J’s newly launched therapy, Inlexzo, for certain types of bladder cancer, generated sales of slightly above $30 million in the first quarter. J&J received a permanent J-code for Inlexzo reimbursement in April that should have boosted patient access and sales for the therapy in the second quarter. Investors will also look out for initial sales numbers of its newly launched oral pill for plaque psoriasis, Icotyde.

Sales of its key drug Stelara are likely to have declined due to the impact of biosimilar competition.

Several biosimilar versions of Stelara were launched in the United States in 2025. According to patent settlements and license agreements, Amgen AMGN, Teva Pharmaceutical Industries TEVA, Samsung Bioepis/Sandoz and some other companies launched Stelara biosimilars in 2025. Stelara’s LOE negatively impacted the Innovative Medicines segment’s growth by 9.2% in the first quarter. We expect the negative impact to be steeper in the second quarter of 2026.

The Zacks Consensus Estimate for Stelara sales is pegged at $654 million.

Imbruvica sales are likely to have declined due to rising competitive pressure in the United States due to new oral competition. The Zacks Consensus Estimate for Imbruvica stands at $630.0 million.

The Zacks Consensus Estimate for J&J’s Innovative Medicine unit is pegged at $16.16 billion.

J&J’s MedTech business is expected to continue seeing strong momentum in three focus areas: Cardiovascular, Surgery and Vision in the second quarter, backed by increased adoption of newly launched products.

J&J’s MedTech business has been facing continued headwinds in China, where sales are being hurt by the impact of the volume-based procurement (VBP) program. VBP is a government-driven cost containment effort in China. In the second quarter, sales in China are likely to have been hurt by the impact of the VBP program once again.

The Zacks Consensus Estimate for J&J’s MedTech segment stands at $8.96 billion.

Nonetheless, a single quarter’s results are not so important for long-term investors. Let us delve deeper to understand whether to buy, sell or hold J&J stock ahead of earnings.

JNJ’s Stock Price Performance & Valuation

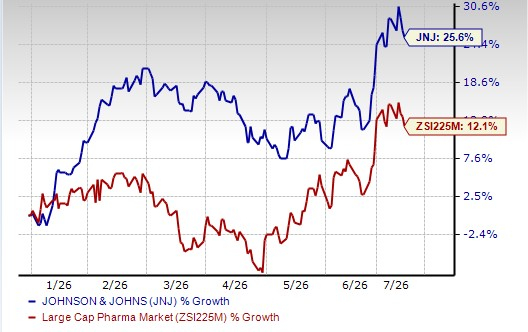

J&J’s shares have outperformed the industry so far this year. The stock has risen 25.6% year to date compared with 12.1% appreciation of the industry.

JNJ Stock Outperforms Industry

From a valuation standpoint, J&J is slightly expensive. Going by the price/earnings ratio, the company’s shares currently trade at 21.17 forward earnings, higher than 18.49 for the industry. The stock is also trading above its five-year mean of 15.65.

JNJ Stock Valuation

Investment Thesis on JNJ

J&J’s biggest strength is its diversified business model, as it not only has pharmaceuticals but also medical devices, which help it withstand economic cycles more effectively.

J&J’s Innovative Medicine unit is showing a growth trend despite Stelara LOE, driven by J&J’s key drugs like Darzalex, Erleada and Tremfya. New drugs like Carvykti, Tecvayli, Talvey, Rybrevant and Spravato also contributed significantly to growth. The company’s MedTech business has improved in the past four quarters.

J&J also rapidly advanced its pipeline in the past year, attaining significant clinical and regulatory milestones that will help drive growth through the back half of the decade. Backed by regular pipeline success, J&J expects a more pronounced impact from new products in 2026 than in 2025.

J&J expects 2026 to be a year of accelerated growth. The company expects both its Innovative Medicines and MedTech segments to deliver stronger growth this year. The company is confident that it can achieve its target of generating around $100 billion in revenues in 2026. It expects sales to continue to improve in 2027, with a “line of sight” to double-digit growth by the end of the decade.

However, J&J faces its share of headwinds like the legal battle surrounding its talc lawsuits, the Stelara patent cliff, the upcoming LOE of key drugs Opsumit and Simponi, and softness in MedTech China.

Stay Invested in J&J Stock

J&J has shown steady revenue and EPS growth for years and expects further growth in 2026. Despite headwinds like the legal battle surrounding its talc lawsuits, the Stelara patent cliff, the upcoming LOE of key drugs Opsumit and Simponi and softness in MedTech China, J&J looks quite confident that it will be able to navigate these challenges.

No matter how the second-quarter’s results play out, one should stay invested in JNJ, considering its price appreciation, rising estimates, consistent earnings and sales growth, important new launches, and pipeline depth.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Amgen Inc. (AMGN): Free Stock Analysis Report

Teva Pharmaceutical Industries Ltd. (TEVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).