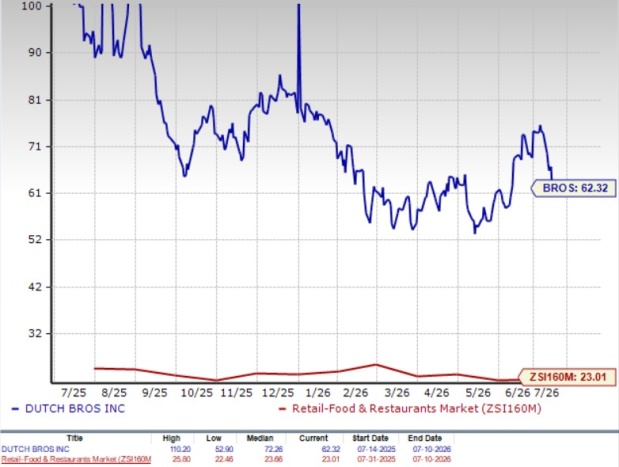

Dutch Bros Inc. BROS is trading at a premium valuation, raising the question of whether the stock still has room to run after its strong rally. The company currently carries a forward 12-month price-to-earnings (P/E) ratio of 62.32, significantly higher than the industry average of 23.01, underscoring investors' high expectations for its growth.

P/E (F12M)

Image Source: Zacks Investment Research

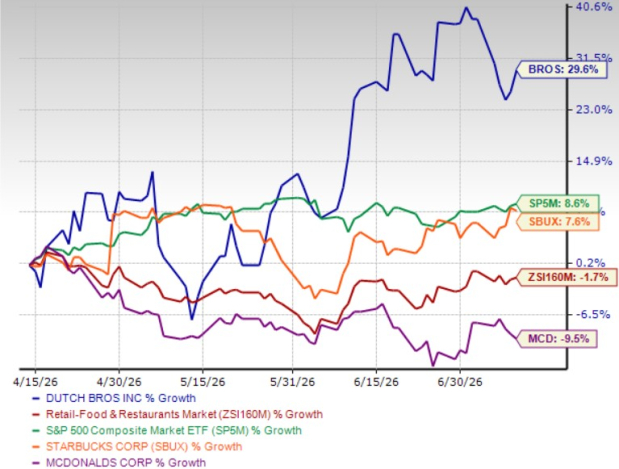

The optimism has been reflected in the stock's performance. Over the past three months, BROS’ shares have climbed 29.6%, handily outperforming the industry's 1.7% decline and the S&P 500's 8.6% rise. Such a sharp advance has left investors weighing whether the company's growth prospects justify its premium valuation or whether much of the upside is already reflected in the share price.

BROS has also outpaced key restaurant peers over the same period, including Starbucks Corporation SBUX and McDonald's MCD, highlighting continued investor confidence in its expansion strategy and long-term growth potential.

Price Performance

Image Source: Zacks Investment Research

Strong Operating Momentum Supports the Bull Case

Dutch Bros reinforced investor optimism with an impressive first-quarter 2026 performance. Revenues climbed 31% year over year to $464 million, while system same-shop sales increased 8.3%, driven primarily by a 5.1% rise in transactions. The company also delivered its seventh consecutive quarter of transaction growth, highlighting sustained customer demand despite an uncertain consumer environment.

Management attributed the performance to its differentiated beverage platform, product innovation, expanding food offerings and continued focus on customer experience. The company noted that all-day beverage demand, customized drinks and operational improvements continue to strengthen customer engagement while supporting higher transaction volumes.

Expansion Story Remains Intact

Dutch Bros continues to execute one of the fastest expansion strategies in the restaurant industry. The company opened 41 new shops during the first quarter and reiterated confidence in reaching 2,029 locations by 2029. Encouraged by its strong start to the year, management raised its 2026 development target to at least 185 new shops.

Importantly, growth is not coming at the expense of store productivity. Average unit volumes reached record levels, while new stores continued to perform in line with system averages. The company also highlighted exceptional early performance from converted Clutch Coffee locations, with reopened stores generating more than three times their pre-conversion sales volumes.

Innovation Continues to Drive Traffic

A major reason behind Dutch Bros' premium valuation is its ability to consistently create new customer occasions. The company reported that its food rollout continues to exceed expectations, with food attachment rates running slightly ahead of early projections. Management now expects the rollout across company-operated stores to be substantially complete by the end of the third quarter.

Limited-time beverages remain another important traffic driver. During the quarter, promotional beverage launches generated approximately 30% higher unit velocity than the prior year, while merchandise promotions also delivered significantly stronger customer engagement.

Dutch Bros also introduced Myst, a plant-powered energy beverage, aimed at expanding its fast-growing energy platform. Management believes Myst complements its existing Rebel energy drinks by targeting different consumption occasions rather than replacing existing demand, helping the company capture a broader customer base.

Digital Ecosystem Strengthens Customer Loyalty

Customer engagement continues to improve through Dutch Rewards. During the first quarter, 74% of all transactions flowed through the loyalty program, while mobile Order Ahead represented approximately 15% of total transactions. These digital initiatives provide valuable customer data, support personalized promotions and encourage repeat visits.

Management also noted that increased segmentation within the rewards platform is improving offer effectiveness and driving stronger engagement among Gen Z and millennial customers, supporting long-term traffic growth.

Management Raises Outlook

Confidence in business momentum prompted management to increase full-year 2026 guidance. Dutch Bros now expects revenues of $2.05-$2.08 billion, system same-shop sales growth of 4-6%, adjusted EBITDA of $370-$380 million and at least 185 new shop openings this year.

The guidance increase reflects continued sales momentum entering the second quarter and reinforces management's confidence in its long-term growth strategy.

BROS' Earnings Estimates

Over the past 30 days, the Zacks Consensus Estimate for BROS’ 2026 earnings per share has increased from 92 cents to 93 cents. The company’s sales and earnings in 2026 are likely to witness growth of 27.1% and 22.4% year over year, respectively,

On the other hand, Starbucks and McDonald's earnings in 2026 are likely to grow 12.7% and 5.8% year over year, respectively.

BROS Earnings Estimate Trend

Image Source: Zacks Investment Research

Buy Now or Wait?

Despite its premium valuation, Dutch Bros appears well positioned for long-term investors thanks to its strong execution and multiple growth drivers. The company continues to generate healthy customer traffic through product innovation, menu expansion, digital engagement and an accelerating store expansion strategy, while management has grown increasingly confident in the business outlook by raising its guidance.

Positive earnings estimate revisions further reinforce expectations for sustained profit growth, with the company projected to deliver faster earnings growth than key restaurant peers. Given its ability to consistently outperform both the industry and competitors while expanding its market presence, BROS remains an attractive choice for growth-oriented investors willing to pay a premium for a business with a long runway for expansion.

BROS currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Starbucks Corporation (SBUX): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Dutch Bros Inc. (BROS): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).