Central Garden & Pet Company CENT noted that its Cost and Simplicity program has fundamentally strengthened the business. The company believes that these efforts have improved operational efficiency, enhanced organizational resilience and created a better-run business. Management also emphasized that this focus on cost discipline and simplification is now embedded in the company’s operating model and continues to shape the way it manages and executes its business.

The company expanded second-quarter fiscal 2026 gross margin by 30 basis points to 33.1%, while operating margin improved to 12.6% from 11.2% in the prior-year period. Higher sales leverage, prudent cost management and ongoing organizational simplification supported margin expansion while allowing continued investment in key growth initiatives. Management highlighted multiple initiatives to simplify the business while enhancing execution and operational efficiency. As part of these efforts, the company relocated its DoMyOwn business to its Covington fulfillment center to improve delivery speed, reduce costs and increase network flexibility.

Additionally, in the last earnings call transcript the company noted that it is consolidating Top Dog Best Bully Sticks manufacturing into its dog and cat platform in New Jersey to leverage scale and manufacturing capabilities better. The company also entered into a joint venture with Phillips Pet Food & Supplies while retaining a 20% ownership stake. Management believes that the partnership will strengthen and enhance the agility of its nationwide distribution network, simplify operations and allow the company to focus more directly on expanding its Central branded portfolio.

The company believes that the streamlined structure supports better execution, stronger productivity and improved cost control while creating room to continue investing behind brands and innovation. Management also reaffirmed fiscal 2026 earnings guidance, noting that ongoing margin discipline and portfolio optimization remain central to its operating strategy despite inflation, tariffs and a promotional retail environment. Management expects adjusted earnings to be $2.70 per share or better.

The Zacks Rundown for CENT

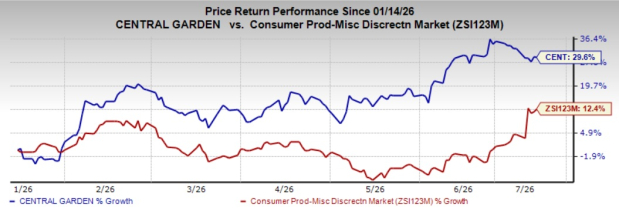

Shares of this Zacks Rank #3 (Hold) company have soared 29.6% in the past six months compared with the industry’s growth of 12.4%.

Image Source: Zacks Investment Research

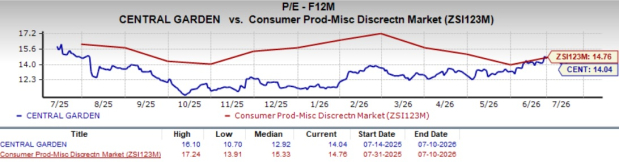

From a valuation standpoint, CENT trades at a forward price-to-earnings ratio of 14.04, lower than the industry’s average of 14.76.

Image Source: Zacks Investment Research

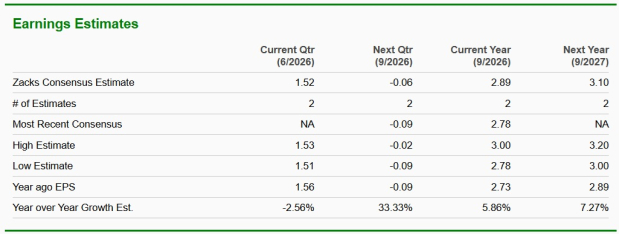

The Zacks Consensus Estimate for CENT’s current and next fiscal year earnings implies year-over-year growth of 5.9% and 7.3%, respectively.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

ARKO Corp. ARKO operates a chain of convenience stores in the United States. ARKO currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for ARKO's current fiscal-year sales implies a decline of 2.8%, while the same for current fiscal-year earnings implies growth of 93.3% from the year-ago reported figures. ARKO delivered a trailing four-quarter earnings surprise of 43.2%, on average.

Colruyt Group N.V. CUYTY together with its subsidiaries, engages in the retail, wholesale, food service, and other activities in Belgium, France, and internationally. It presently flaunts a Zacks Rank #1.

The Zacks Consensus Estimate for CUYTY's current financial-year sales and earnings indicates 7.4% and 2.5% growth, respectively, from the last year.

Phibro Animal Health Corporation PAHC operates as an animal health and mineral nutrition company in the United States, Latin America and Canada, Europe, the Middle East, Africa, and the Asia Pacific. PAHC currently carries a Zacks Rank of 2 (Buy).

The Zacks Consensus Estimate for PAHC's current fiscal-year sales and earnings implies growth of 14.8% and 47.4%, respectively, from the year-ago actuals. PAHC delivered a trailing four-quarter earnings surprise of 16.3%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

Colruyt SA Unsponsored ADR (CUYTY): Free Stock Analysis Report

ARKO Corp. (ARKO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).