KLA KLAC shares are overvalued, as suggested by the Value Score of F. In terms of the forward 12-month price/sales, KLAC is trading at 17.47X, higher than the broader Zacks Computer and Technology sector’s 6.98X. KLAC shares are trading at a premium compared with MKS MKSI and Entegris ENTG, shares of which are trading at 4.69X and 6.05X, respectively, but at a discount compared with Lam Research’s LRCX 14.25X.

KLAC Stock’s Valuation

Image Source: Zacks Investment Research

So, is the KLA stock a buy, sell or hold at this level? Let’s find out.

KLAC Jumps 91% Year to Date: What’s Driving the Stock?

KLA shares have jumped 90.5% year to date (YTD), outperforming the broader sector. The company continues to be one of the biggest beneficiaries of AI-driven semiconductor manufacturing. KLAC has repeatedly emphasized that AI infrastructure spending is increasing demand across foundry/logic, (high-bandwidth memory) HBM memory and advanced packaging, all of which require significantly higher levels of inspection and metrology. The company is expected to benefit from strong demand visibility as management expects calendar 2026 wafer equipment spending to exceed $140 billion.

AI chips continue to feature larger die sizes, more complex designs, tighter yield requirements and higher wafer values. This increases process control intensity because chipmakers inspect wafers more frequently to maximize yields. KLAC expects AI-related investments to remain a multi-year tailwind rather than a short-term spending cycle, supporting stronger equipment demand into both 2026 and 2027. Meanwhile, KLA’s expanding addressable market beyond traditional wafer fabrication into advanced packaging has been a key catalyst.

Advanced packaging has become one of KLA’s fastest-growing businesses as AI accelerators increasingly rely on chiplets, hybrid bonding and heterogeneous integration. KLA continues to widen its leadership in semiconductor process control and now expects semiconductor process control revenues from advanced packaging to increase to approximately $1 billion in calendar 2026, up from roughly $635 million in 2025. The company also noted that advanced packaging equipment demand is now growing faster than originally anticipated, with packaging spending expected to grow more than 30% industrywide.

KLAC Prospects Face Tough Challenges

KLA is suffering from higher DRAM prices that have increased the cost of image-processing computers that ship with KLA’s systems. The company expects elevated memory prices to persist through at least calendar 2026 and estimates roughly a 100-basis-point (bps) gross margin headwind over the coming quarters.

Meanwhile, KLA continues to face evolving U.S. export restrictions, tariffs and other trade limitations that could restrict equipment shipments or service opportunities for certain Chinese customers. Any slowdown in hyperscaler AI spending can limit KLAC’s share price appreciation, given stiff competition from MKS, Lam Research and Entegris, along with others.

MKS currently serves more than 85% of wafer fabrication equipment and has expanded its presence in lithography, metrology and inspection through acquisitions, making KLA one of its key customers as well as an indirect competitor in process control technologies. Lam Research remains one of KLA’s strongest competitors for semiconductor capital spending as AI accelerates demand for leading-edge manufacturing. The company also highlighted a broad pipeline of new products, increasing market share at leading-edge foundries and more than 50% growth in advanced packaging revenues for 2026.

Entegris competes with KLA in helping semiconductor manufacturers improve yield and process performance. The company expects strong growth from advanced logic, DRAM, AI-driven memory, advanced deposition materials, liquid filtration and selective etch products. Entegris management has highlighted increasing semiconductor process complexity and higher materials content per wafer at advanced nodes. The company also expects stronger wafer fabrication equipment spending and expanding fab construction activity through 2026 and beyond.

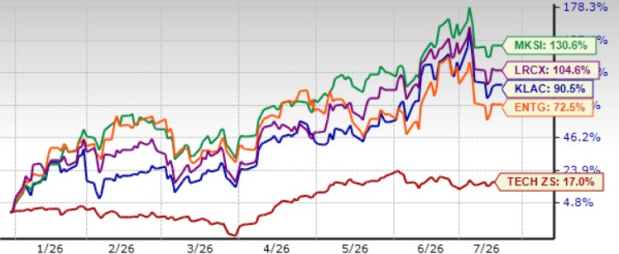

KLA shares have underperformed MKS and Lam Research but outperformed Entegris, YTD. Shares of MKS, Lam Research and Entegris have returned 130.6%, 104.6% and 72.5%, respectively.

KLAC Stock’s Price Performance

Image Source: Zacks Investment Research

KLAC’s Earnings Estimate Revision Remains Steady

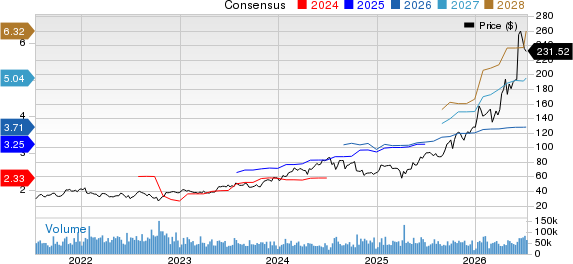

The Zacks Consensus Estimate for fourth-quarter fiscal 2026 revenues is currently pegged at $3.61 billion, suggesting 13.6% growth from the figure reported in the year-ago quarter. The consensus mark for earnings is currently pegged at $1 per share, unchanged over the past 30 days. The figure suggests 6.38% growth from the figure reported in the year-ago quarter.

KLA Corporation Price and Consensus

KLA Corporation price-consensus-chart | KLA Corporation Quote

The Zacks Consensus Estimate for fiscal 2026 revenues is currently pegged at $13.53 billion, suggesting 11.28% growth from the figure reported in fiscal 2025. The consensus mark for earnings is currently pegged at $3.71 per share, unchanged over the past 30 days. The figure suggests 11.41% growth from the figure reported in fiscal 2025.

Conclusion

KLA remains well-positioned to benefit from AI-driven semiconductor investments, expanding advanced packaging demand and rising process control intensity, supporting healthy long-term growth. However, outstretched valuation, margin pressure from higher memory costs, geopolitical risks and intense competition temper the near-term risk-reward profile. With earnings estimates remaining unchanged and much of the AI optimism already reflected in the share price, investors may be better served waiting for a more attractive entry point before adding exposure to KLAC.

KLA currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

KLA Corporation (KLAC): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

MKS Inc. (MKSI): Free Stock Analysis Report

Entegris, Inc. (ENTG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).