MaxLinear MXL is no longer being valued like a quiet turnaround story. The stock’s surge has moved the investor debate to a harder question: how much future improvement is already reflected in the price?

The answer is mixed. MaxLinear has a better earnings setup than it had a year ago, but the valuation now leaves less margin for disappointment.

MXL Rally Has Changed the Debate

MaxLinear shares have climbed 406.3% in the year-to-date period and 495% over the trailing 12 months. That performance has far outpaced the Zacks sub-industry, the broader Zacks Computer & Technology sector and the S&P 500 index over the same periods.

The growth case has become easier to defend. The Zacks Consensus Estimate indicates revenues of $655 million in 2026 and $777 million in 2027. Earnings are projected at $1.33 per share in 2026 and $1.81 in 2027.

MaxLinear’s first-quarter 2026 results also support the recovery story. The company reported earnings of 22 cents per share, beating the Zacks Consensus Estimate by 22.2%, and revenues of $137.2 million, up 43% year over year.

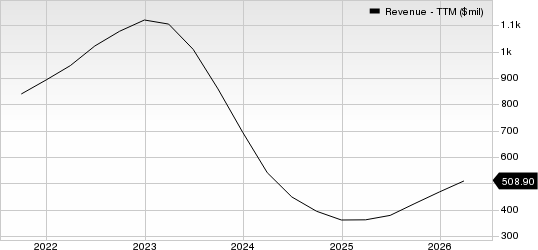

MaxLinear, Inc Revenue (TTM)

MaxLinear, Inc revenue-ttm | MaxLinear, Inc Quote

The second-quarter setup points to another step up. Management expects revenues of $160 million to $170 million and sequential growth across all four business segments, led by infrastructure strength from data center optical interconnects.

MXL Valuation Leaves Less Room for Error

The problem is that the stock already prices in a lot of that improvement. A premium sales multiple can be justified when revenues, margins and earnings are rising, but it also raises the cost of any delay in program ramps.

The price target of $96 compares with a stock price of $91.30 as of July 10, 2026. That gap suggests the stock has less obvious upside after its rally, even with the stronger operating outlook.

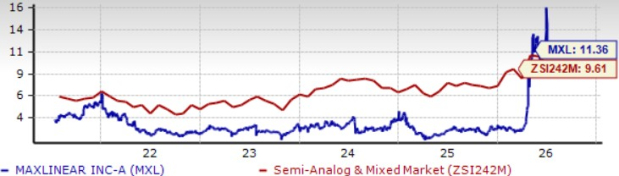

MaxLinear shares are overvalued, as suggested by a Value Score of F. MXL trades at 11.4X forward 12-month sales, above 9.6X for the Zacks sub-industry, 7X for the sector and 5.1X for the S&P 500. In comparison, shares of competitors including Broadcom AVGO, Marvell MRVL and MACOM Technology MTSI are trading at 12.55X, 14.93X and 15.83X, respectively.

MXL Stock’s Valuation

Image Source: Zacks Investment Research

Execution is the key variable. MaxLinear’s optical data center ramps, 1.6 terabit Rushmore cycle, storage accelerators, USB bridges, fiber passive optical network, Wi-Fi 7 gateways and data over cable service interface specification programs provide multiple growth paths. Still, early hyperscaler programs can be concentrated, and some ramps remain in early stages.

MaxLinear Cash Conversion Bears Watching

Revenue growth is only part of the investment case. Investors also need to watch whether higher demand turns into clean cash generation or requires more working capital first.

MaxLinear used $8.9 million in operating cash flow in the first quarter of 2026. The main use of cash was a substantial wafer prepayment tied to demand for data center low-node geometry products.

Inventory also rose by roughly $8 million sequentially, even as days of inventory improved to about 128 days. That does not weaken the revenue story by itself, but it shows that scaling demand may pressure cash conversion before it improves the financial profile.

MXL Faces Stiff Competition

Broadcom is MaxLinear's strongest competitor in high-speed networking and AI infrastructure, backed by a far broader portfolio spanning custom AI accelerators, Ethernet switching, optical interconnects, broadband chips and enterprise software. Broadcom's leadership in hyperscale networking and custom silicon gives it significantly greater scale and customer reach.

Marvell competes directly with MaxLinear in optical DSPs, networking silicon and data center connectivity. Marvell already has an established position in electro-optics through its PAM4 DSPs, optical networking processors and custom silicon business, making it one of the primary beneficiaries of AI-driven data center spending.

MACOM competes with MaxLinear across optical networking, RF, analog and high-speed semiconductor solutions serving data centers, telecom and defense markets. MACOM has built a strong franchise in optical components, including lasers, drivers, TIAs and RF technologies, giving it deep exposure to AI networking infrastructure.

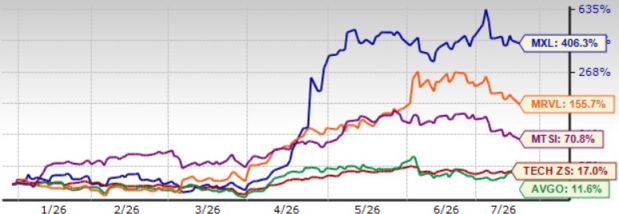

Year to date, MXL shares have returned 406.3% outperforming Broadcom’s, Marvell’s and MACOM Technology’s appreciation of 11.6%, 155.7%, and 70.8%, respectively.

MXL Stock’s Price Performance

Image Source: Zacks Investment Research

Conclusion

The bottom line is that MXL has real operating momentum, but the stock is no longer priced for a low-expectation recovery. Growth visibility has improved, while valuation support has become less obvious after the rally.

MaxLinear currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

MaxLinear, Inc (MXL): Free Stock Analysis Report

Marvell Technology, Inc. (MRVL): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

MACOM Technology Solutions Holdings, Inc. (MTSI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).