The Wendy's Company WEN continues to face margin headwinds, but management believes its comprehensive turnaround strategy, dubbed Project Fresh, could gradually improve profitability as the year unfolds. While first-quarter performance remained under pressure, executives pointed to encouraging operational improvements that could support both sales and margins over time.

During the quarter, U.S. company-operated restaurant margin fell to 11.4%, reflecting softer customer traffic, elevated beef costs, investments in food quality upgrades and labor inflation. Adjusted EBITDA also declined as the company stepped up spending on marketing, field support and international expansion. Despite these challenges, Wendy’s maintained its full-year outlook, signaling confidence that conditions will improve in the second half.

Project Fresh is central to that recovery. Wendy’s is upgrading the core menu with improved hamburger buns, enhanced condiments and a revamped spicy chicken sandwich while strengthening value offerings through its Biggie Deals platform. At the same time, WEN is focusing on cleaner restaurants, better order accuracy and enhanced employee training, areas where company-operated restaurants have already outperformed the broader system. Management believes stronger execution will increase customer satisfaction, encourage repeat visits and ultimately lift restaurant economics.

Digital initiatives are also contributing to the turnaround. U.S. digital sales increased, supported by AI-powered recommendations in the mobile app and continued investments in the digital ordering experience. Meanwhile, Wendy’s is expanding internationally, highlighted by a franchise agreement to develop up to 1,000 restaurants in China, providing an additional long-term growth avenue.

Although commodity inflation, especially beef costs and cautious consumer spending remain near-term risks, Wendy’s expects improving sales trends, better operational execution and easing cost pressures later in the year to support margin recovery. If Project Fresh continues to gain traction, the company could gradually rebuild profitability while laying the foundation for sustainable long-term growth.

Peers Are Also Balancing Costs With Operational Improvements

Wendy's turnaround efforts mirror broader trends across the quick-service restaurant industry, where operators are working to protect margins while navigating inflation and cautious consumer spending. McDonald's MCD continues to focus on affordability through value offerings while leveraging its vast digital ecosystem, loyalty program and operational efficiencies to offset higher labor and commodity costs. Its scale and strong franchise network have helped McDonald's preserve profitability despite a challenging demand environment.

Restaurant Brands International QSR, the parent of Burger King, is pursuing a similar strategy through its "Reclaim the Flame" initiative. The company is investing in restaurant modernization, improved operations and targeted marketing to strengthen guest traffic and franchisee economics. Menu innovation and digital expansion also remain as Restaurant Brands International's key priorities for driving profitable growth.

Compared with these rivals, Wendy's differentiates itself through Project Fresh, which combines menu quality upgrades, operational improvements and system optimization. While margin pressure remains in the near term, the successful execution of these initiatives could help Wendy's narrow the profitability gap with larger competitors over time.

WEN’s Price Performance, Valuation & Estimates

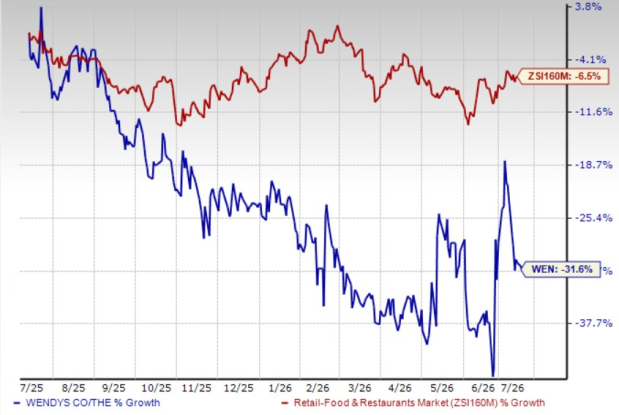

Shares of Wendy’s have dropped 31.6% in the past year compared with the industry’s 6.5% decline.

Price Performance

Image Source: Zacks Investment Research

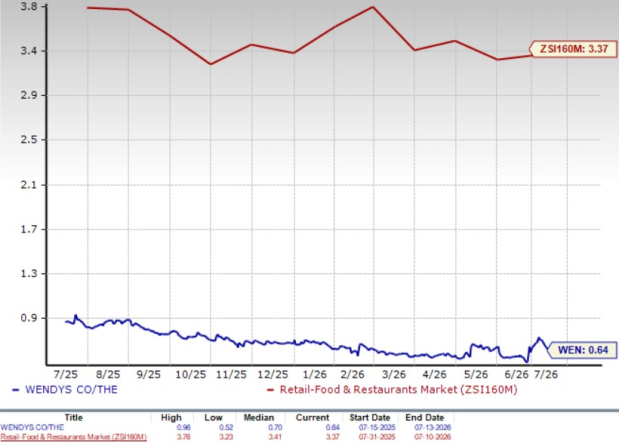

From a valuation standpoint, WEN trades at a forward price-to-sales (P/S) multiple of 0.64, below the industry’s average of 3.37.

WEN’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for WEN’s 2026 earnings per share (EPS) implies a year-over-year decline of 34.1%. The EPS estimates for 2026 have remained unchanged in the past 30 days.

EPS Trend of WEN Stock

Image Source: Zacks Investment Research

WEN’s Zacks Rank

WEN stock currently carries a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Wendy's Company (WEN): Free Stock Analysis Report

McDonald's Corporation (MCD): Free Stock Analysis Report

Restaurant Brands International Inc. (QSR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).