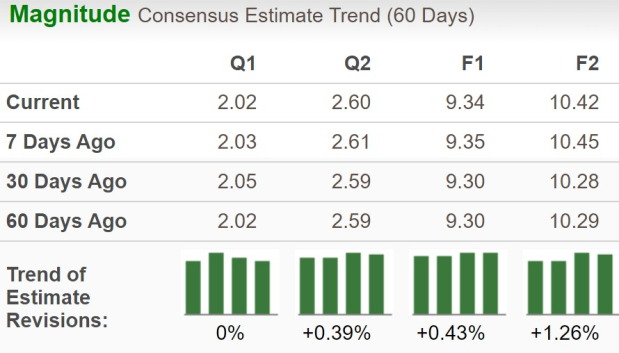

Consumer financial services company, Synchrony Financial SYF, is set to report second-quarter 2026 results on July 21, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $2.02 per shareon revenues of $4.67 billion.

The second-quarter earnings estimate has witnessed no upward revision and three downward movements over the past 30 days. The bottom-line projection indicates a year-over-year decrease of 19.2%. The Zacks Consensus Estimate for quarterly revenues implies year-over-year growth of 3.4%.

For full-year 2026, the Zacks Consensus Estimate for Synchrony’s revenues is pegged at $19.12 billion, implying an increase of 3.6% year over year. However, the consensus mark for the current year EPS is pegged at $9.34, signaling a decline of around 0.9% on a year-over-year basis.

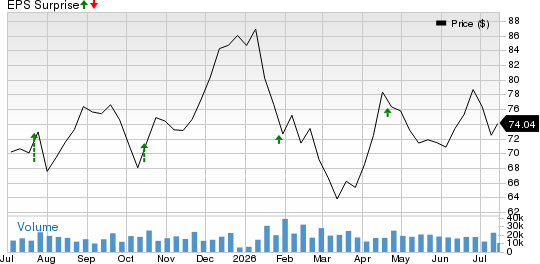

SYF’s earnings beat the consensus estimate in three of the last four quarters and met once, with the average surprise being 20.7%.

Synchrony Financial Price and EPS Surprise

Synchrony Financial price-eps-surprise | Synchrony Financial Quote

Q2 Earnings Whispers for SYF

Our proven model predicts a likely earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That is precisely the case here.

Synchronyhas an Earnings ESP of +2.07% and carries a Zacks Rank #3 at present. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

What’s Shaping SYF’s Q2 Results?

Synchrony is expected to have seen advantages in the second quarter from increased net interest margin and higher purchase volumes. Our model predicts interest and fees on loans of $5.47 billion for the quarter, up 2.6% from a year ago. Higher figures from Health & Wellness and Digital are likely to have anchored the results.

The Zacks Consensus Estimate for net interest margin is pegged at 15.31%, up from 14.78% achieved a year ago, increasing its profitability. The consensus mark for total purchase volumes indicates 5.1% year-over-year growth. The Zacks Consensus Estimate indicates that the total average active accounts are likely to increase 1.2% in the second quarter.

The consensus mark for the net charge-offs ratio is pegged at 5.61, down from 5.70 a year ago. The above-mentioned factors are likely to have benefited the company in the second quarter, positioning it for an earnings beat.

However, Synchrony is expected to have incurred increased information processing and employee costs in the second quarter, partially offsetting the positives. Also, RSA is expected to have increased nearly 10% year over year in the second quarter. SYF is expected to have witnessed a 0.2% decrease in average interest-earning assets.

Other Stocks That Warrant a Look

Here are some other companies worth considering from the broader Finance space, as our model shows that these, too, have the right combination of elements to beat on earnings this time around:

Brookfield Asset Management Ltd. BAM has an Earnings ESP of +4.55% and a Zacks Rank of 3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Brookfield Asset Management’s bottom line for the to-be-reported quarter is pegged at 44 cents per share, which indicates 15.8% year-over-year growth. The consensus estimate for BAM’s revenues is pegged at $1.49 billion, a 15.6% increase from a year ago.

American Express Company AXP has an Earnings ESP of +0.73% and a Zacks Rank #3 at present.

The Zacks Consensus Estimate for AmEx’s bottom line for the to-be-reported quarter is pegged at $4.41 per share, which increased by 2 cents over the past week and indicates 8.1% year-over-year growth. The consensus estimate for AmEx’s revenues is pegged at $19.62 billion, a 9.9% increase from a year ago.

Virtu Financial, Inc. VIRT has an Earnings ESP of +14.23% and a Zacks Rank of 3 at present.

The Zacks Consensus Estimate for Virtu Financial’s bottom line for the to-be-reported quarter is pegged at $1.59 per share, a growth of 3.9% from a year ago. The consensus estimate for VIRT’s revenues is pegged at $602.74 million, a 6.2% year-over-year jump.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Synchrony Financial (SYF): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

Brookfield Asset Management Ltd. (BAM): Free Stock Analysis Report

Virtu Financial, Inc. (VIRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).