Johnson & Johnson JNJ delivered better-than-expected second-quarter 2026 results, supported by continued strength across its Innovative Medicine portfolio and steady MedTech execution. The healthcare giant reported adjusted earnings and revenues ahead of consensus estimates while lifting its full-year sales and earnings outlook, reflecting confidence in its commercial momentum and expanding pipeline.

Management emphasized that the company remains on track to surpass $100 billion in annual revenues for the first time in its 140-year history. Strong performances from oncology, immunology and neuroscience products, coupled with a growing roster of new launches, more than offset continued pressure from STELARA biosimilar competition and softer trends in portions of the MedTech business.

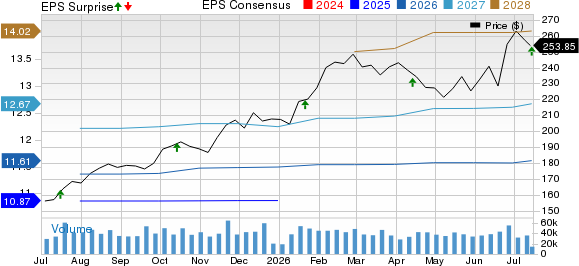

Earnings Beat Expectations

Johnson & Johnson reported second-quarter adjusted earnings of $2.90 per share, topping the Zacks Consensus Estimate of $2.84. Revenues increased 6.6% year over year to $25.31 billion, outpacing the Zacks Consensus Estimate of $25.18 billion.

Johnson & Johnson Price, Consensus and EPS Surprise

Johnson & Johnson price-consensus-eps-surprise-chart | Johnson & Johnson Quote

Reported EPS was $2.27 compared with $2.29 in the year-ago period, while adjusted net earnings rose 5.7% to $7.08 billion. Worldwide operational sales increased 5.6%, or 5.7% on an adjusted operational basis.

Innovative Medicine Continues to Drive Growth

Innovative Medicine remained the primary growth engine, with worldwide sales climbing 7.8% (6.8% operational) to $16.38 billion. Growth was led by blockbuster oncology therapies DARZALEX, CARVYKTI, TECVAYLI and RYBREVANT/LAZCLUZE, alongside continued momentum from TREMFYA, SPRAVATO and CAPLYTA.

Management noted that excluding STELARA, whose sales continue to be pressured by biosimilar competition, the company delivered double-digit operational growth during the quarter. CEO Joaquin Duato said Johnson & Johnson now has 28 platforms generating more than $1 billion in annual sales and expects new launches such as ICOTYDE, INLEXZO and RYBREVANT to support accelerating growth into 2027.

TREMFYA remained a standout performer as inflammatory bowel disease indications continued driving strong uptake. Meanwhile, CAPLYTA benefited from its recently expanded schizophrenia label, while SPRAVATO maintained robust demand.

MedTech Performance Mixed but Long-Term Outlook Intact

MedTech revenues increased 4.5% (3.6% operational) to $8.93 billion.

Growth was driven by cardiovascular products, wound closure and biosurgery offerings, contact lenses and orthopedic trauma products. Shockwave continued generating double-digit growth, while the Vision business benefited from strong ACUVUE demand and premium intraocular lens adoption.

However, management acknowledged weaker-than-expected performance in Heart Recovery, where increased physician caution following external clinical data temporarily pressured Abiomed procedure volumes. CFO Joseph Wolk said expectations for Abiomed have been moderated for the remainder of 2026, though the company continues to expect improvement over the longer term.

Pipeline Momentum Supports Long-Term Growth

Executives highlighted another active quarter across the pipeline, including FDA approvals for TREMFYA's psoriatic arthritis label expansion, CAPLYTA for relapse prevention in schizophrenia and the Dual Energy THERMOCOOL SMARTTOUCH SF platform.

The company also reported encouraging clinical data for RYBREVANT FASPRO in head and neck cancer, TALVEY plus DARZALEX FASPRO in multiple myeloma and the OTTAVA robotic surgery platform.

Management reiterated confidence that recent launches are tracking ahead of expectations. ICOTYDE has already reached more than 10,000 patient starts, with executives describing physician uptake and payer access as stronger than initially anticipated.

Johnson & Johnson Raises 2026 Guidance

Following the stronger-than-expected first half, Johnson & Johnson increased its 2026 outlook.

The company now expects reported sales of $100.8-$101.4 billion, representing approximately 7.3% growth at the midpoint. Adjusted EPS guidance was raised to $11.60-$11.75, with a midpoint of $11.68, up $0.13 from the prior guidance.

Management also raised adjusted operational EPS guidance to a midpoint of $11.58 while expecting approximately 75 basis points of adjusted pretax operating margin expansion during the year.

Analyst Questions Focus on Growth Sustainability

During the Q&A session, analysts concentrated on the drivers behind the guidance increase, launch trajectories for ICOTYDE, MedTech recovery prospects and pipeline execution.

Management indicated that Innovative Medicine will contribute the majority of the higher revenue outlook, supported by continued momentum from TREMFYA, ICOTYDE, INLEXZO and oncology products. While MedTech growth is expected to improve during the second half, executives acknowledged that Abiomed's recovery will likely extend into 2027.

Executives also emphasized upcoming catalysts, including additional data readouts across oncology and immunology, potential FDA approval for IMAAVY in warm autoimmune hemolytic anemia and anticipated regulatory milestones for the OTTAVA robotic surgical system.

Looking Ahead

Johnson & Johnson exited the quarter with broad-based commercial momentum, multiple successful product launches and improving financial guidance. Although biosimilar pressure on STELARA and temporary MedTech headwinds remain challenges, management believes the breadth of its portfolio and pipeline positions the company for sustained long-term growth while maintaining its goal of reaching double-digit growth by the end of the decade.

Zacks Rank and Style Scores Signals

Johnson & Johnson currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock has a Value Score of C, a Growth Score of F and a Momentum Score of A, resulting in a VGM Score of D. Investors following the Zacks Style Scores may find the company's strong momentum profile encouraging, though the lower Growth and VGM scores suggest a more balanced risk-reward profile following the recent earnings report.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Johnson & Johnson (JNJ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).