Demand for high-precision lasers is rising. As artificial intelligence (AI) workloads expand and cloud companies upgrade their optical infrastructure, the need for faster, more reliable technologies grows. Lumentum Holdings (LITE), long a low-profile player, is now gaining attention. Known for its expertise in indium phosphide and advanced laser technologies, the company has moved beyond telecom roots to become a key supplier in AI-driven data center infrastructure. But that low-profile phase now looks like a thing of the past.

No surprise, then, that the stock has rocketed 1,600% over the past year, driven by powerful hyperscale demand. What began as a steady rise in 2025 has turned into a full breakout in 2026, fueled by strong AI-led catalysts. It may be a coincidence that Lumentum rhymes with “momentum,” but the stock’s performance clearly reflects that trend.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

A big part of that rally ties back to rising expectations around AI infrastructure. Its high-profile partnership with NVIDIA (NVDA) and growing relevance in next-gen optical technologies have strengthened investor confidence. Add to that its inclusion in the S&P 500 ($SPX), and the story has clearly shifted. More importantly, Lumentum says demand from hyperscalers is so strong that its order book could stay filled through 2028, as AI data centers race to scale and require faster, high-capacity optical connections.

After such a massive run, does LITE stock still have more room to run higher?

About Lumentum Stock

Valued at $64.1 billion and founded in 2015, Lumentum is a San Jose-based optical technology leader powering the modern AI era. The company builds laser chips, photonic components, and high-speed transceivers used across AI data centers, cloud networks, and global fiber systems. Operating worldwide, Lumentum runs two segments: Cloud & Networking, supplying advanced optics to hyperscalers and network equipment makers, and Industrial Tech, providing precision lasers for semiconductors, solar, displays, and EV manufacturing.

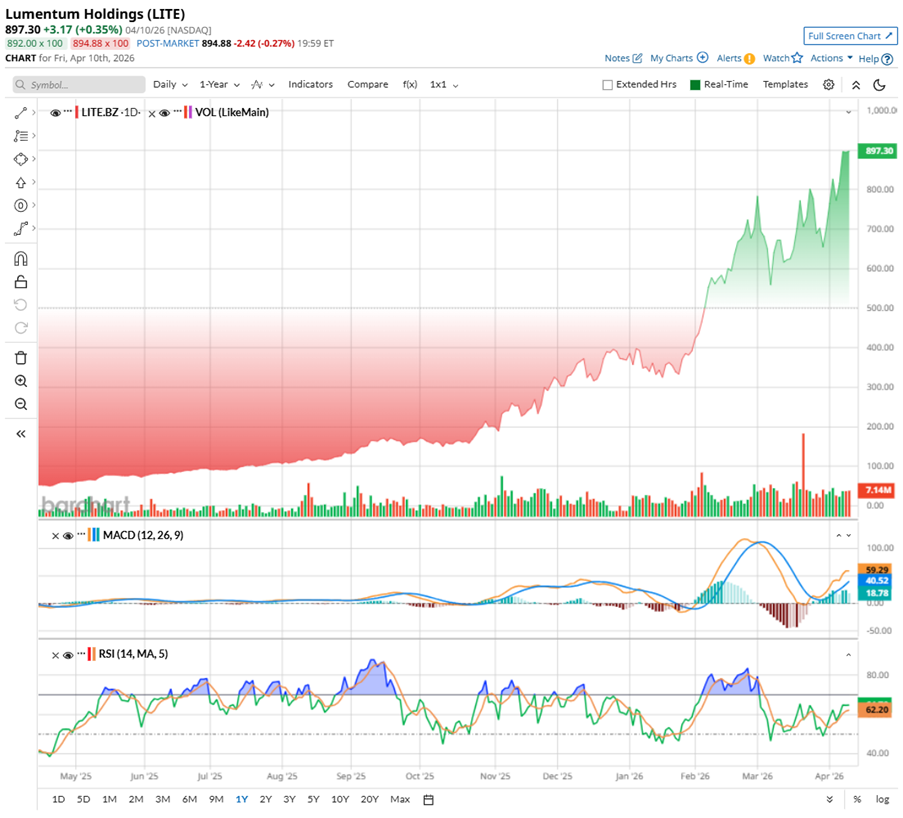

Lumentum Holdings has gone from a quiet player to a market standout, riding the powerful wave of the AI infrastructure boom. The stock surged close to a high of $960 just last week, pausing only briefly after a relentless rally fueled by strong earnings and rising confidence around its role in next-gen data centers.

Even now, the momentum is hard to ignore. LITE has climbed 136.35% so far in 2026, with gains of over 39.95% in the past month and nearly 12.81% in just the last five days. Each move higher seems to build on the last.

Zooming out, over the past 52 weeks, LITE stock has skyrocketed 1,599.2%, including a staggering 442.59% jump in just six months, marking a clear turning point in its growth journey.

Technically, the setup for LITE still looks firmly in the bulls’ favor. The 14-day RSI, which had risen to overbought territory in February, has now cooled to 61.76, suggesting the stock has reset without losing its underlying strength.

At the same time, the MACD oscillator is flashing a positive signal. The yellow line has crossed back above the blue signal line – a classic bullish crossover – while the histogram has turned positive. Together, these indicators suggest momentum is rebuilding, and the broader uptrend remains intact.

www.barchart.com

www.barchart.com Lumentum Holdings’ stock carries a premium price tag now. Priced at 115.25 times forward adjusted price-to-earnings and 21.91 times price-to-sales, it sits well above peers and its own historical average.

But that premium reflects its growing role in AI infrastructure. Investors are betting that demand for high-speed optical networking in AI data centers will stay strong, and for now, they seem comfortable paying up for that future growth story.

Lumentum Beats on Q2 Numbers

Lumentum released its Q2 fiscal 2026 results on Feb. 3, and the results were a significant turning point for the company. It impressed investors, with the stock rising for the next four trading sessions. The company didn’t just beat expectations, it blew past them on both revenue and earnings, showing that its AI story is translating into real numbers.

In fiscal Q2, revenue jumped to $665.5 million, marking a sharp 65.5% year-over-year (YOY) rise. This was not a one-off spike either. Growth came from across the business, with its core components segment rising 68.3% and systems revenue climbing 60.1% annually. It’s the kind of broad-based strength that suggests demand is building across the entire AI ecosystem.

What stood out even more was the turnaround in profitability. A year ago, Lumentum was in the red. Its Q2 net income amounted to $78.2 million, with adjusted earnings surging to $1.67 per share. Margins also told a strong story, with gross margins expanding significantly and operating margins pushing to 25.2%.

CEO Michael Hurlston called it a “standout quarter,” but the more telling part was his outlook. He emphasized that most of the growth opportunity still lies ahead, signaling that the AI wave for Lumentum may just be getting started.

Behind the scenes, the company is moving quickly to keep up. It is expanding its manufacturing footprint in the U.S., including a new large-scale facility focused on advanced optical technologies used in AI data centers. At the same time, collaborations with players like Marvell Technology (MRVL) are pushing innovation further, especially in speeding up the pace at which data moves across massive AI systems.

Looking ahead, the momentum seems to be building, not slowing. Management’s guidance for the next quarter points to another strong jump in revenue and earnings. Revenue is expected to land between $780 million and $830 million, a sharp step up from the already strong Q2 performance. Adjusted EPS is projected to be between $2.15 to $2.35, comfortably ahead of earlier expectations and reflecting continued margin strength.

Meanwhile, analysts monitoring Lumentum expect the company’s Q3 EPS growth of 706.7% YOY to be $1.82, with revenue around $809.5 million. Fiscal 2026 EPS is expected to be $5.90, up 1,304% annually, and rise by another 133.2% to $13.76 in fiscal 2027.

What Do Analysts Expect for Lumentum Stock?

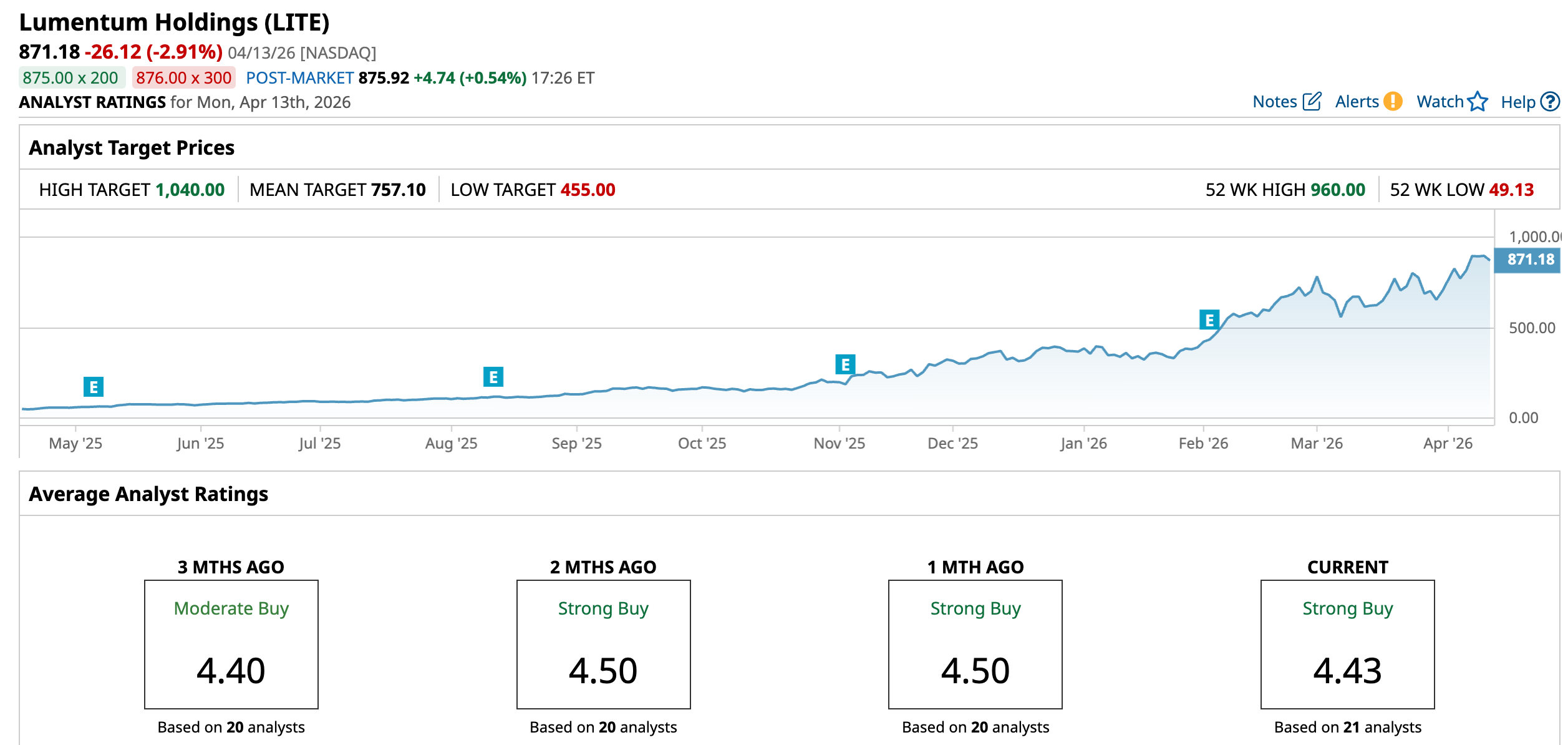

JPMorgan Chase is growing more confident in LITE stock, maintaining its “Overweight” rating while sharply lifting its price target to $950 from $565. The shift follows Lumentum’s recent investor briefing, where management painted a clearer picture of future growth.

Analysts came away impressed by stronger-than-expected visibility across key demand drivers, especially in AI-related markets. New customer agreements and ongoing capacity expansions added further conviction, suggesting that the company’s growth story is not only intact but accelerating, giving JPMorgan greater confidence in its long-term outlook.

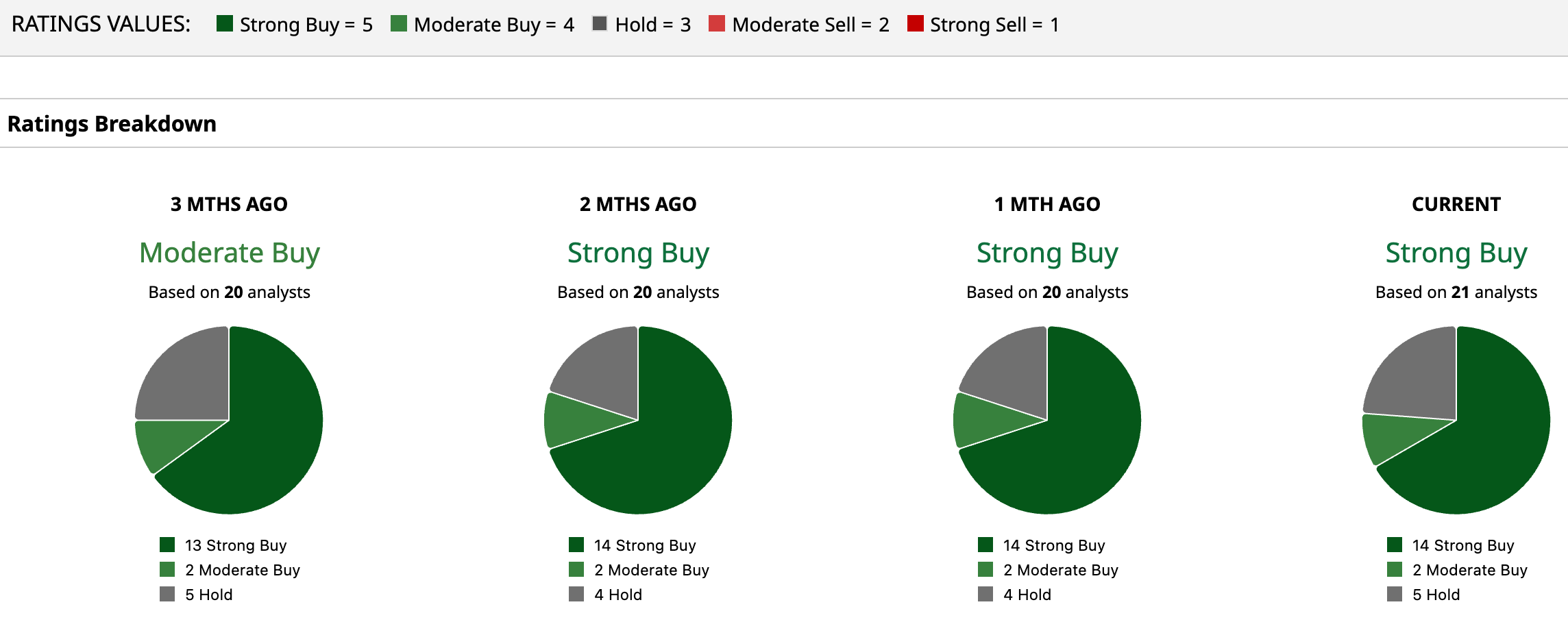

Lumentum has a consensus “Strong Buy” rating overall – an upgrade from the “Moderate Buy” rating three months back. Out of the 21 analysts offering recommendations for the stock, 14 suggest a “Strong Buy,” two advise a “Moderate Buy,” and the remaining five give a “Hold” rating.

After its impressive run, LITE now trades above its average Street target. Yet the Street-high $1,040 call still flags roughly 19.38% upside potential from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Should You Buy the Dip in Fastenal Stock Today? Glencore Stock Is Up 120% in the Past Year. Can It Survive the Iran War? Aggressive Traders Looking for a Rebound Should Consider Carnival Cruise (CCL) Stock Fastenal Stock Sold Off on Q1 Earnings. Don’t Buy the Dip.